Welcome to FHA+, Gate House’s monthly intel brief from our team of housing and mortgage industry experts. Each month we provide timely insight, information, and analysis regarding the Federal Housing Administration as well as the entire housing and housing finance ecosystem. Each edition begins with our “Think Piece,” followed by our “Three Questions,” then “Inside Voices,” and the “Gate House Index.” In this month’s Think Piece, Brian Montgomery argues that the time is right to grant Ginnie Mae and FHA greater independence as a standalone government agency. Keith Becker also offers his reaction to FHA’s 2025 Annual Report to Congress. In Three Questions, Gate House Advisor Cecily King shares her insights into the challenges facing developers in 2026. And in Inside Voices, we share what we are hearing around the industry and policy circles. Once again, please enjoy this complimentary copy of FHA+ and Happy New Year. — Brian Montgomery, Gate House Strategies Chairman and former HUD Deputy Secretary and FHA commissioner.

THINK PIECE

One Additional Big Change for Mortgage Finance Needed

by Brian D. Montgomery

It is anticipated that 2026 will be a significant, even monumental, year in housing finance with the Administration signaling aggressive efforts to lower costs and its strong intention to remove Fannie Mae and Freddie Mac from conservatorship after 17+ years.

It would be a long-awaited exit for the housing giants that have combined portfolios of nearly $8 trillion. If done correctly, their release would help reduce political influence over a large sector of the U.S. economy and ultimately deliver better value to homebuyers and taxpayers.

The other significant portion of government-backed housing finance, however, is also worth our serious attention at this time of enormous financial innovation and technological advance in the U.S. mortgage market.

Ginnie Mae and FHA, in particular, comprise another massive segment of the housing finance ecosystem -- $2.8 trillion in MBS backed by Ginnie’s full-faith-and-credit guarantee, $1.5 trillion of which is FHA endorsed-loans made to 8 million households. These entities should be released in a different way by moving them to a stand-alone government agency that befits their large role and influence.

Though they serve vital missions while currently sitting within HUD -- playing an important countercyclical role in our economy as evidenced during the 2008 global financial crisis when FHA-backed mortgages surged from 3% of purchase mortgages to nearly 30% and enhancing daily mortgage market liquidity -- we would do better to provide the duo with additional independence.

Consider that FHA was created as an independent agency in 1934 amidst the Great Depression, and operated as an independent agency for 3 decades before being transferred into HUD with the HUD Act of 1965. Ginnie’s function was performed by the independent government agency FNMA from 1938 until being spun off and placed within HUD in 1968. For decades they have provided vital access to housing for first-time homebuyers, minorities, seniors, and underserved communities.

Unlike most of HUD, Ginnie Mae and FHA do not function as traditional grant-making or social-policy programs. They operate as distinct financial institutions in the secondary mortgage market: managing credit risk, overseeing counterparties, and supporting capital markets through mortgage insurance and guarantees. Their missions and risks more closely resemble those of financial regulators than those of a cabinet agency built to administer housing assistance and community development programs.

The work of Ginnie Mae and FHA is consequential and complex—credit modeling and management, securitization oversight, issuer surveillance, and loss mitigation at scale. Yet their employee compensation frameworks lag far behind financial regulators like the Federal Reserve, FHFA, or FDIC. Independence would allow market-competitive pay, improving the recruitment and retention of specialized talent. Talent gaps, I should add, are not abstract—they translate directly into operational risk, fiscal exposure, and missed opportunities for innovation.

Anyone who has observed Ginnie Mae or FHA compete for HUD-wide IT dollars like I have, knows the challenge that process presents to their operations. Independent budget authority would enable transition from outdated legacy systems to sustained investment in modern risk analytics, counterparty monitoring, and servicing platforms. Better technology in an advancing marketplace means fewer defaults, stronger taxpayer protections, and operational resilience when markets are under stress.

While FHA has received some long overdue IT funding in recent years, they should not be allocated at the whim of an obstinate or inattentive Congress.

While implementation would require legislation and careful coordination, these are solvable problems: inter-agency councils, shared policy frameworks, and statutory mission alignment can preserve support for underserved borrowers. This is not partisan, and it is not about crowding out the private sector. On the contrary, it is about reliable market liquidity at scale and scope.

Making Ginnie Mae and FHA into an independent agency that provides competitive compensation, budget autonomy, and modern governance and IT infrastructure would make them stronger, safer, and more effective.

For more information, contact: FHAplus@gatehousedc.com.

Gate House Partner and former FHA Chief Risk Officer Keith Becker on FHA’s fiscal year 2025 'Annual Report to Congress Regarding the Financial Status of the FHA Mutual Mortgage Insurance Fund, released December 31, 2025:

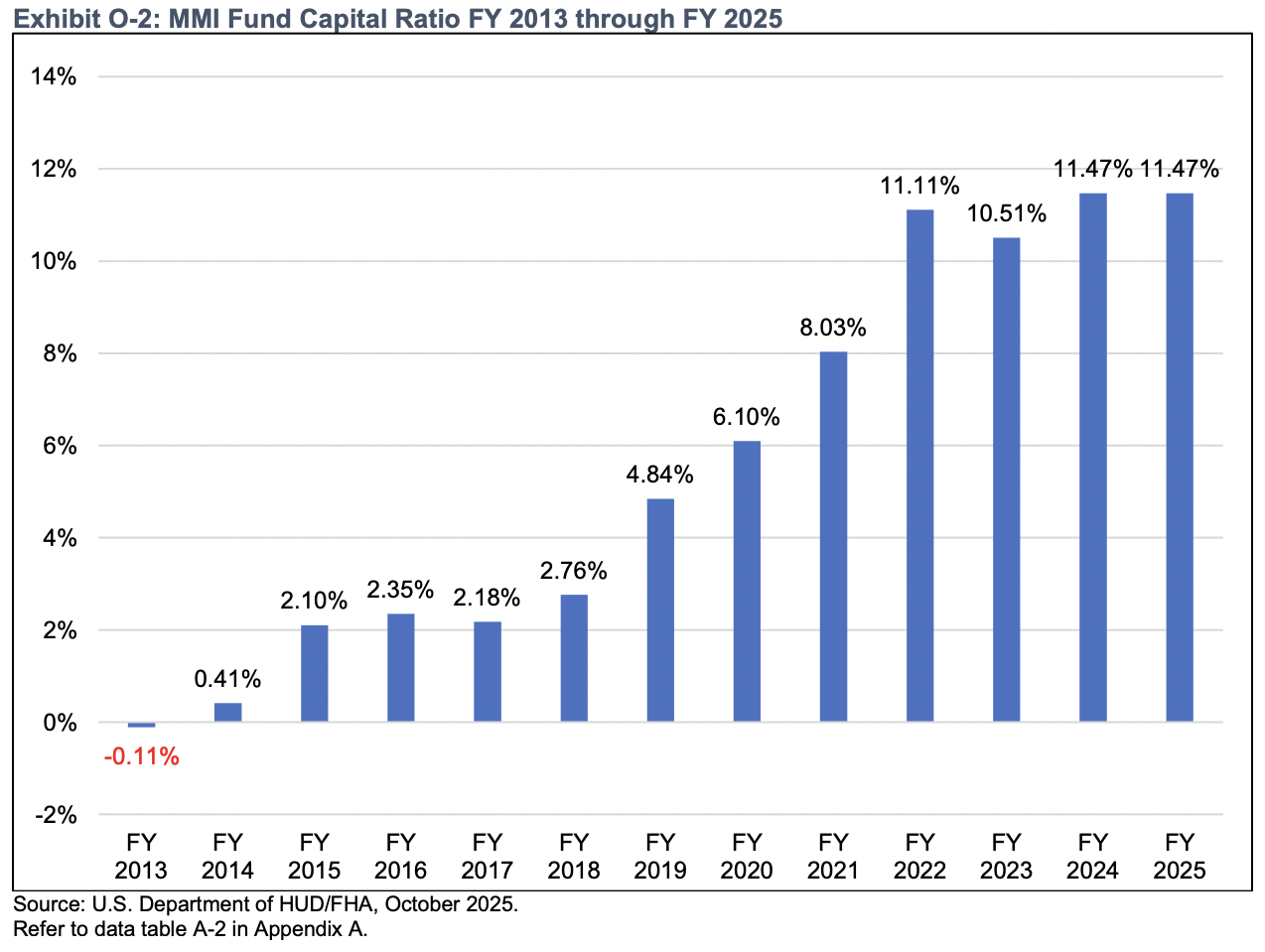

FHA has continued its strong support of its core mission to provide mortgage liquidity for first time homebuyers along with low- and moderate-income borrowers as well as minorities, seniors, and other underserved communities. The report reveals that the MMI Fund maintains a strong capital position with an 11.47% capital ratio—well above the statutory 2% minimum—and demonstrates resilience even under severe economic stress scenarios. Both the Forward and Reverse businesses showed strong results again in 2025 and comprehensive stress testing, including replays of over 100 historical economic scenarios since 1954, indicates the Fund would maintain a 4.42% capital ratio even in the most aggressive downturn in the market (mirroring 2007 conditions), indicating sufficient capitalization to withstand significant economic turbulence.

It is also noteworthy that under the Trump Administration, FHA implemented key policy reforms in FY 2025 aimed at increasing affordable homeownership and other priorities. These reforms included rescinding burdensome regulations, such as outdated appraisal protocols, unnecessary origination requirements, and restrictive construction standards; updating loss mitigation requirements to improve the sustainability of loss mitigation outcomes; and revising borrower residency requirements to prioritize U.S. citizens and lawful permanent residents. Additionally, FHA continued technology modernization efforts through enhancements to the FHA Catalyst platform and prepared for the adoption of the modernized Uniform Appraisal Dataset in Spring 2026, all designed to reduce costs, streamline operations, and expand access to homeownership for American families.”

The strong results reported by FHA will undoubtedly lead many to call on the FHA to reduce mortgage insurance premiums (MIPs). There are reasons to be cautious about that approach, not least of which are the significant changes in the loss mitigation space, including the limitation on permanent loss mitigation home retention options to one every 24 months. The impact of this policy change is not yet known but the one- year re-default rate after loss mitigation exceeded 50% in 2024. If historical results hold, I anticipate an increase in delinquencies and defaults as some borrowers with more than temporary difficulties will not be eligible for loss mitigation. Combined with a recent increase in serious delinquencies and overall loss rates, the totality of circumstances argues strongly for a delay in any consideration of reducing the MIP for the time being. It's also important to remember the unintended consequence of a premium reduction — while it may decrease the cost of homeownership on its face, it will also increase demand for housing that in a tight inventory environment will ultimately drive up home prices and can result in higher, not lower, costs of homeownership. Finally, for a typical FHA borrower with a mid-600 credit score and LTVs greater than 80%, the FHA mortgage is already cheaper than a GSE execution when we consider the cost of a conforming interest rate combined with the GSE guarantee fee and loan level price adjustments along with private mortgage insurance (PMI) premiums for loans with those credit characteristics.

THREE QUESTIONS

Cecily King on Affordable Housing Development Today

Cecily King is founder of Detroit-based Kipling Development, a real estate development and consulting firm. She previously served as development director of the City of Detroit’s Housing and Revitalization Department. A Gate House Strategies advisor, King holds an MS in Real Estate Development from Columbia University, an MEng in Structural Engineering from Lehigh University and a BSE in Civil and Environment Engineering from Princeton University. She is an Associate Professor of Professional Practice at Columbia Graduate School of Architecture, Planning and Preservation, where she teaches courses on real estate development, community and economic development, and urban revitalization strategy.

Question: You started out as a structural engineer. What unique value does that background bring to your work now as a developer?

King: The important thing about that background is that it's grounded in execution. Engineering is all about end-problem solving. Working with the developer, the architect comes up with a vision. They then hand the drawings to you and say, “Okay, make it stand up.” And frankly, the notion of problem solving from within a decision has an element of fun to it. What's cool about being on the development side now is applying that problem solving ability, whether it’s about the capital stack, or construction, or entitlements or policy. Execution happens at the intersection of complex pieces.

Question: You also served in the City of Detroit’s housing department. Now as a private developer, you know what it’s like to be on the public sector side. What would you want other developers to understand better about the public sector mindset? And what would you want public sector folks to understand better about the developers at the table?

King: Many of my fellow private sector developers don't have public sector experience. What I encourage them to do is to genuinely care about public policy. You simply need to be involved in the process. Most of those on the public side who are making policy are doing so with good intentions. But they often are going about it without any private sector experience. As a developer, you must be willing to sit at a table with them and have real conversations about policy. Even though you’d much prefer being out in the field hammering out the project. But your participation in the policy making process will have positive implications on your ability to actually deliver that project.

The challenge public sector folks face is understanding the realities of the execution of their proposed policies. There's intent and then there's outcome. That’s what I tell friends in the public sector. The secret is to be able to follow the thread that goes from very initial goal setting to reality on the ground. You need to ask what the goal is, and what it will look like when your private sector partner is faced with executing that goal.

Question: What are the barriers you face in the marketplace right now?

King: I’d say there are two: inflated costs and market instability. As for the latter, there is simply too much uncertainty out there right now, whether it’s from new or proposed public policy or potential shifts in budget priorities for investors and for all levels of government. It’s hard to plan and that’s making investors especially skittish. Financial partners are not quite sure what's happening. They're like, “Oh, we're just going to hold off until 2026.” In affordable housing development, the sources of subsidy that traditionally have existed for gap financing are now a little slower on the commitment. They don’t know how much subsidy they’ll have to allocate. And let me tell you, it’s hard to run a business in a wait-and-see environment.

Then there are the high costs. Not only in construction and taxes, but now we’re looking at all insurance premiums escalating across the board. For new construction, for preservation, and on renewals. And a housing developer cannot operate without multiple types of insurance.

For more from this Gate House advisor, check out The Real Value of Real Estate with Cecily King

INSIDE VOICES

What we’re hearing around Washington and the industry

FHA Congrats! The confirmation of Joe Gormley as President of Ginnie Mae and Frank Cassidy as HUD Assistant Secretary and Federal Housing Commissioner brings seasoned, steady leadership to federal housing roles at a moment when experience truly matters. Both are widely respected insiders with deep institutional knowledge and long track records of navigating complex policy, operational, and stakeholder challenges.

Housing Legislation: The House Financial Services Committee’s recent bipartisan passage of the Housing for the 21st Century Act aligns closely with the Senate’s ROAD to Housing bill, signaling rare bipartisan momentum on initiatives to address housing affordability and supply. Both bills focus on cutting regulatory barriers, modernizing federal housing programs, and incentivizing local reforms to boost production. To become law, the chambers must reconcile the bills, secure leadership backing, and clear floor votes—steps that could yield the most meaningful housing legislation in years.

Financial Stability Oversight Council (FSOC) Pivots: At the recent FSOC meeting, the Council emphasized advancing new workstreams on AI, market resilience, and crisis preparedness, signaling a more targeted and growth-aware approach to systemic risk. As Chair Scott Bessent noted, “Too often in the past, efforts to safeguard the financial system have resulted in burdensome and often duplicative regulations,” underscoring a renewed focus on balance and efficiency.

Freddie Mac AI Guidance: Freddie Mac’s new AI requirements make clear that AI is now a core compliance and risk issue, not just a tech function. Seller/servicers must have formal, senior-management–approved AI governance, clear documentation on how AI/ML is used (including vendor tools), ongoing monitoring and annual reviews, and the ability to disclose AI use to Freddie Mac on request—with lenders retaining full accountability for outcomes. Compliance teams should revisit governance, controls, and oversight before implementation deadlines arrive.

Credit scores, what next? The MBA and industry groups have growing concern that current credit reporting policies are adding cost and friction without clear risk benefits. Many are concerned that mandated use of multiple credit reports could drive lender compliance costs and borrower fees higher with little payoff for access or safety. More recently, the MBA called for one single credit report for credit scores over 700. FHFA continues to evaluate the issues and concerns.

THE GATE HOUSE INDEX

The Gate House Index and analysis is designed to provide insight into the status of FHA’s business at a moment in time and over a period of time, as well as other pertinent data points we’re following.

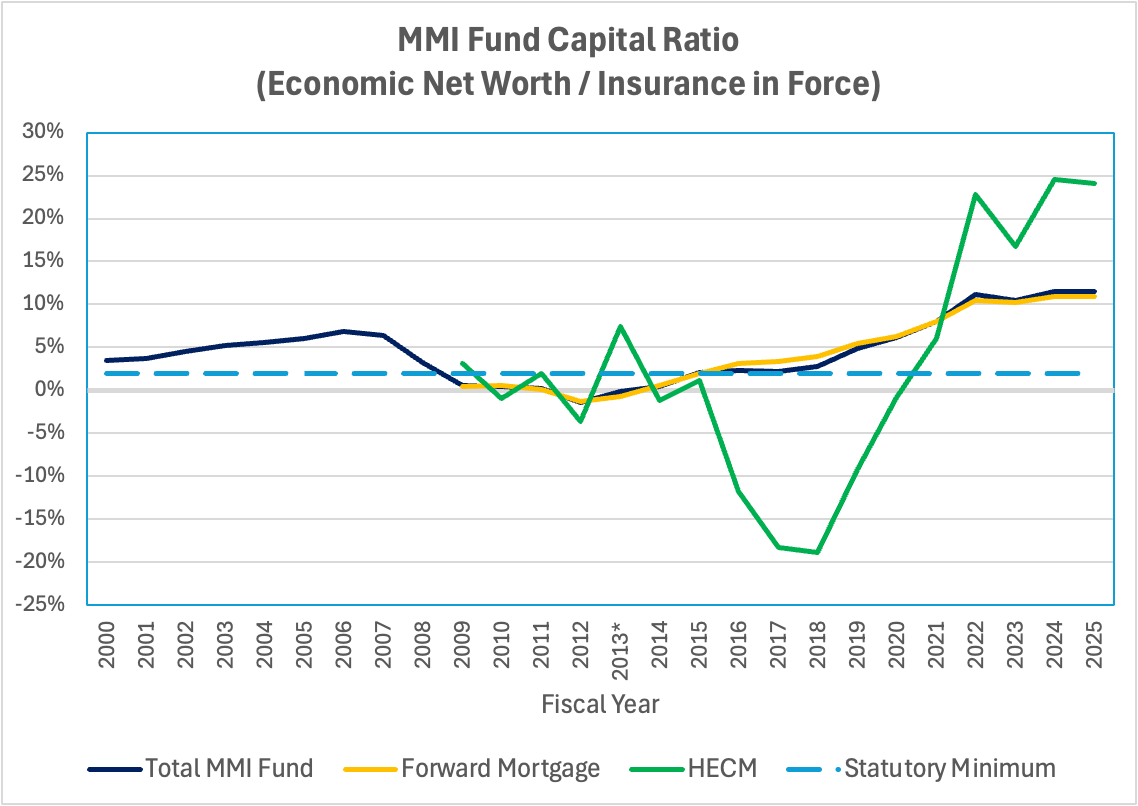

This month, we look at the results of the 2025 Annual Report to Congress Regarding the Financial Status of the Federal Housing Administration Mutual Mortgage Insurance Fund, the subject of Keith Becker’s comments above. The MMI Fund’s Capital totals $189 billion, comprised of the Fund’s Capital Resource -- the collected upfront and monthly insurance premiums, investments, recoveries on disposed assets, and any notes and properties awaiting disposition -- plus the net present value of future expected cash flows. Expressed as a ratio to the Insurance in Force of $1.6 trillion yields a Capital Ratio of 11.47%, unchanged from a year ago. The Capital Ratio for FHA forward mortgages has been relatively flat over the past 4 years while the Capital Ratio of the HECM book has been highly sensitive since the HECM portfolio was added to the MMI Fund in 2009, as seen here:

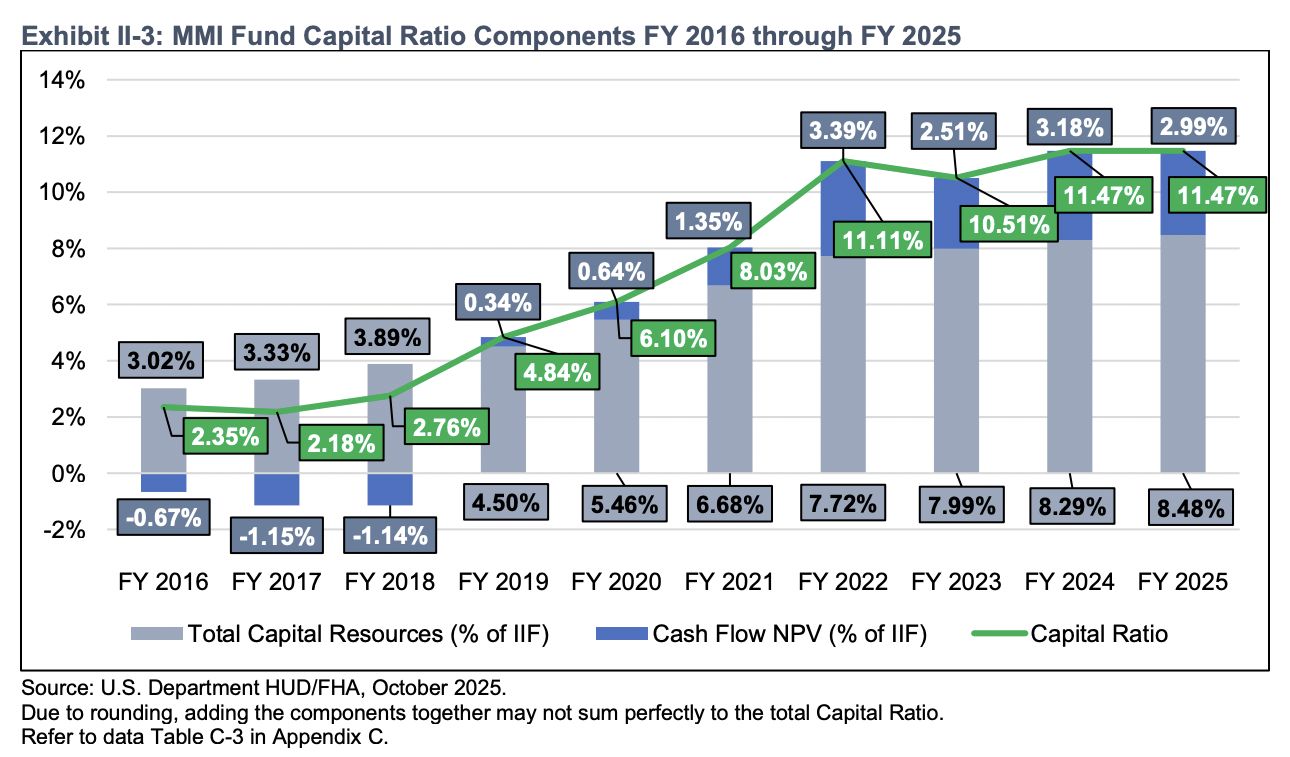

The following chart from the 2025 Report shows the breakdown of the components of the Capital Ratio -- Total Capital Resources (8.48%)+ Cash Flow NPV (2.99%) = 11.47% in 2025:

Again, the denominator in the ratio is the FHA Insurance in Force, $1.6 trillion (made up of nearly 8 million loans backed by FHA):

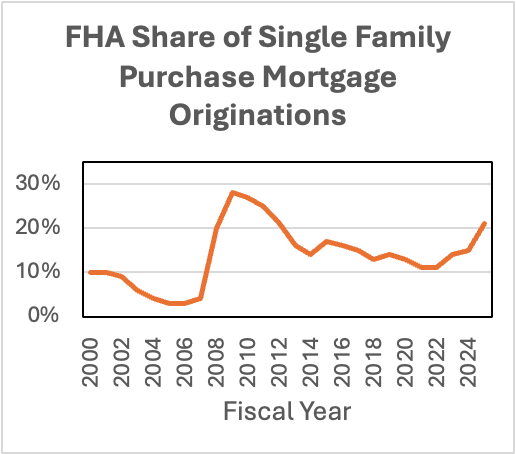

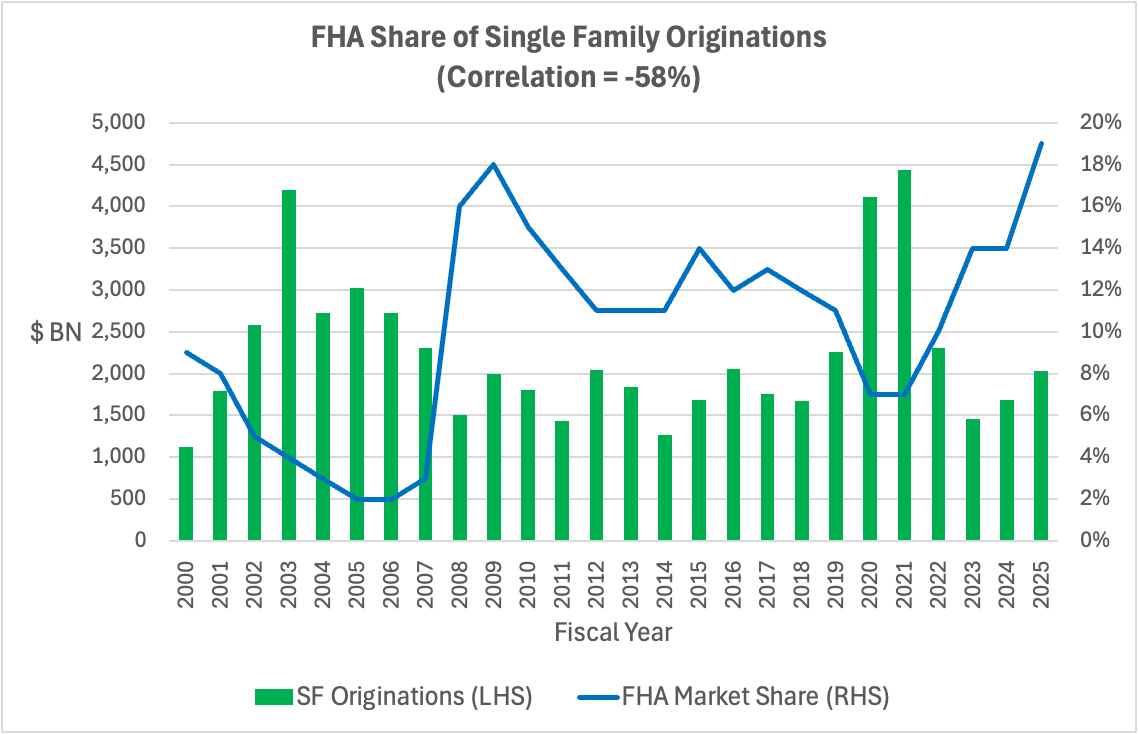

As mortgage originations have fallen since 2021, FHA share of single family originations has risen, reflecting its countercyclical importance and the challenges of housing affordability:

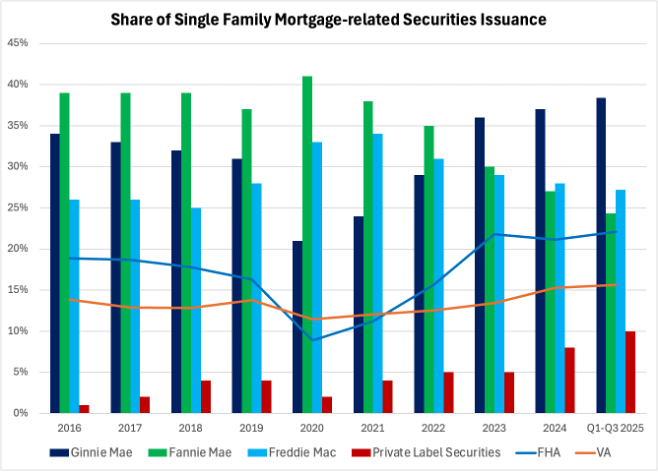

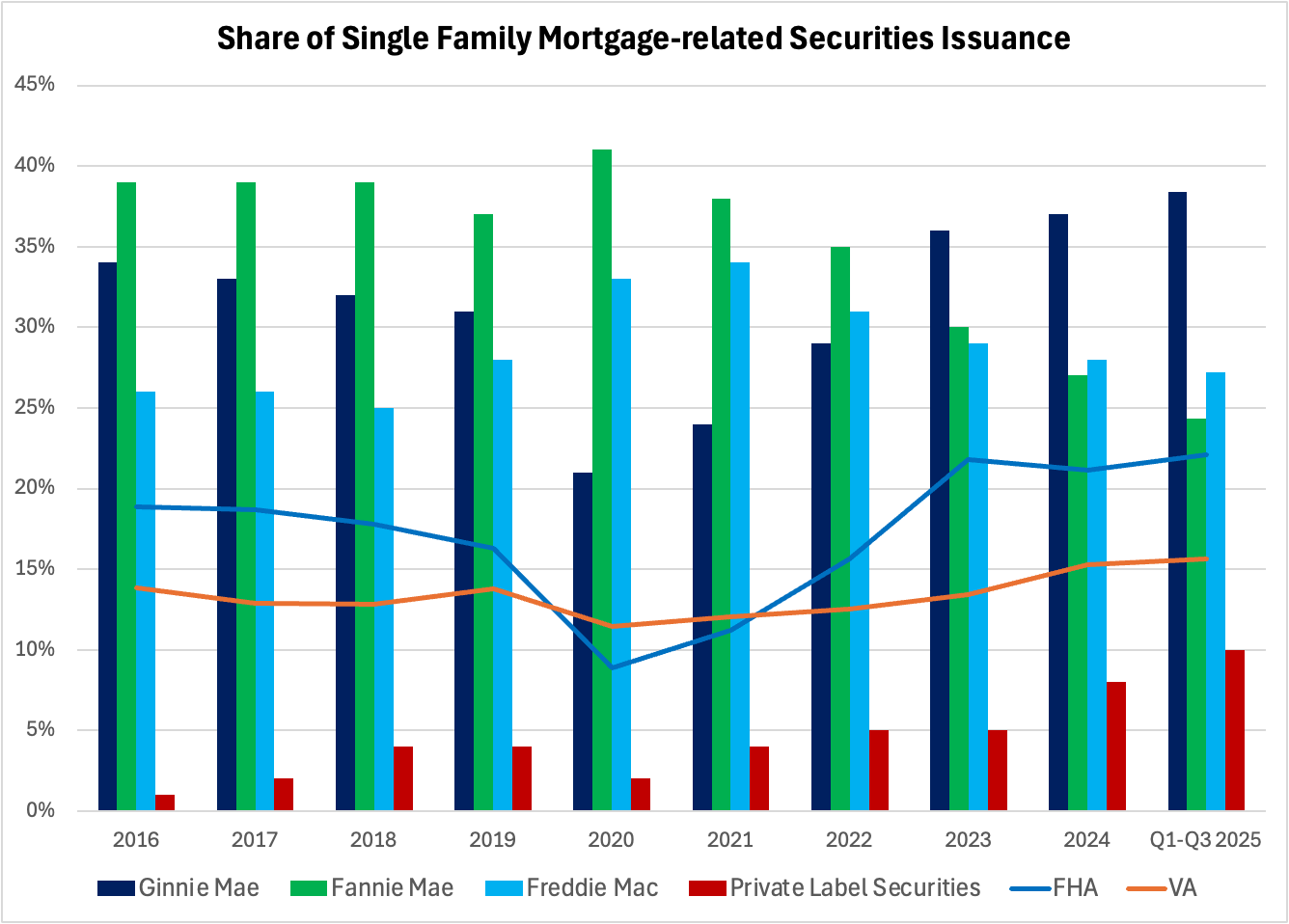

Ginnie Mae share of mortgage-related securities issuance continues to rise and has exceeded Fannie Mae and Freddie Mac individually over the past three years:

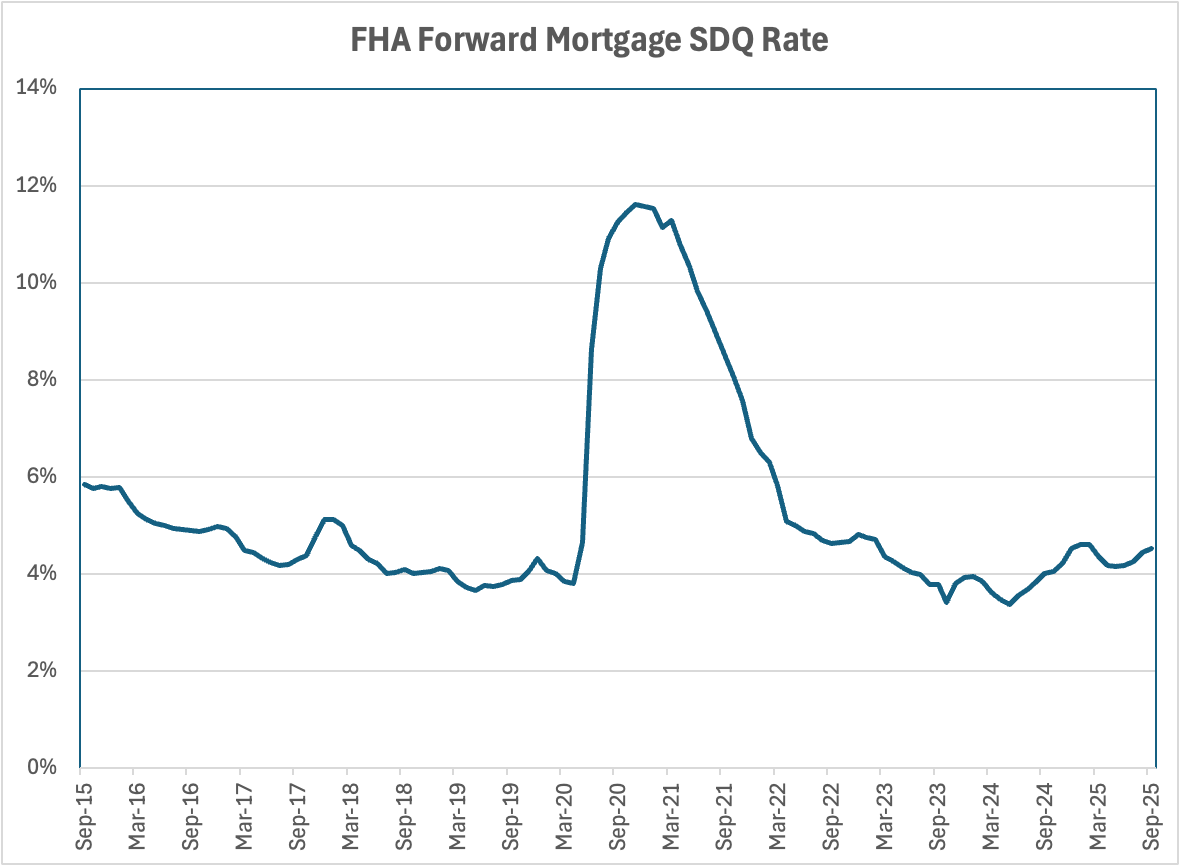

Meanwhile, the serious delinquency rate for FHA while relatively stable the past three years beginning to trend up:

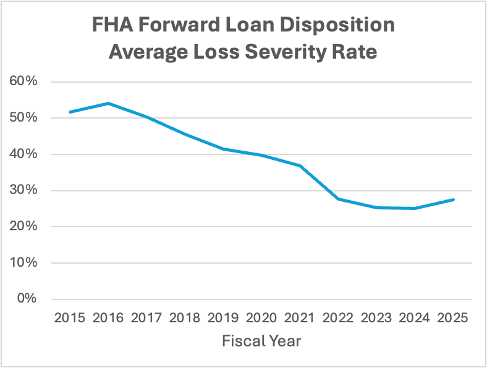

And though the FHA loss severity rate has been down significantly, supported by rapid home price-appreciation in the early ‘20’s, it ticked up in 2025:

This Month In History

In January 1938, Fannie Mae began purchasing FHA-insured mortgages from loan originators using federal funds, effectively creating the U.S. secondary mortgage market.

Although Fannie Mae was not formally chartered until later that year with enactment of the National Housing Act Amendments of 1938, these early purchases were carried out under broad executive and emergency lending authority within the framework of the National Housing Act of 1934.

FHA+ is published monthly by Gate House Strategies, a Washington, DC area-based advisory firm focused within the financial services, mortgage lending and servicing, community development, and public housing sectors. Contact us at FHAplus@gatehousedc.com