This Issue Includes:

- Think Piece (Special Holiday Edition): Housing leaders reflect on 2025’s biggest shifts and what’s ahead in 2026.

- Three Questions: Joseph Gormley on Ginnie Mae’s priorities, capital markets, and modernization efforts.

- Inside Voices: HUD reopening, FHA delinquencies, GSE developments, AI policy debates, and CFPB updates.

- Gate House Index: Key 2026 forecasts for growth, inflation, rates, housing activity, and originations.

THINK PIECE

Special Holiday Edition

December is the unique time when we can look back on the year that’s passing while simultaneously looking forward to the one approaching. That’s why we thought we’d ask the experts these two questions:

1. What is a big change you saw happening for the housing and housing finance world in 2025?

2. What is a big change you anticipate happening by the end of 2026?

Stan Middleman, President & CEO, Freedom Mortgage

A big change in 2025: The biggest surprise of 2025 was the dramatic climate change in the regulatory environment. It was not so much easing of enforcement (which there seemed to be) as the massive degree to which the system was diminished in capacity.

An anticipated change in 2026: 2026 may hold surprises, I think there could be some increase in unemployment resulting in a slight surprise to the upside in loan origination. I think we may find ourselves surprisingly stable. Without seeing a major shift. We may be surprised at the speed of technological advancement in our sector.

Brian Montgomery, Chairman, Gate House Strategies

A big change in 2025: It is refreshing to see housing supply increase especially new construction, but looking back over the last 11 months, I would offer the biggest change in the housing industry is the one that hasn't happened--the housing market is still flat across a laundry list of metrics: lack of affordability in many markets, stubbornly high interest rates, sluggish existing sales, and no real movement on the future of the GSEs.

An anticipated change in 2026: I think we will see slight improvement in the overall housing market aided by continued acceptance of new technology in particular AI. The regulatory environment will be a mixed bag with enforcement at the federal level somewhat diminished, but expanding within several large blue states.

David Dworkin, President & CEO, National Housing Conference

A big change in 2025: The crippling of the Consumer Financial Protection Bureau is the biggest change. It presents even greater risk for lenders than consumers. While no one in the industry was happy with the previous Administration’s approach, gutting the agency increases legal risk by eliminating regulatory guidance essential to compliance. Given the 5-year statute of limitations, and increased likelihood of state actions and private action lawsuits, lenders may end up paying a lot more in compliance costs and fines that could have been avoided.

An anticipated change in 2026: All eyes are on the future of Fannie Mae and Freddie Mac. Will there be a secondary offering? How big will it be and who will buy it? Will an offering make any changes to the Enterprises that could increase MBS spreads or reduce the value of future offerings. What does the future of conservatorship look like? What will Congress do? Everything is on the table and anything could happen. Earlier this year, NHC released a paper on considerations and priorities for administrative recapitalization and release of the Enterprises, and at the top of that list is do no harm.

Cecily King, Managing Principal, Kipling Development/Associate Professor, Columbia University, MS in Real Estate Development

A big change in 2025: One of the most discussed changes in affordable housing finance in 2025 was the permanent reduction of the bond test from 50% to 25% for 4% LIHTC projects. Since the modification is anticipated to ease 4% LIHTC transaction feasibility and facilitate more deal volume, I will be keeping an eye on closings as we go into 2026 and reflecting on how capital stacks shift in response to this policy change.

An anticipated change in 2026: I honestly hope that big changes happen with insurance premium costs in 2026. The cost increases on premiums are impacting multifamily valuations and are even starting to limit their ability to trade.

Dror Oppenheimer, Partner, Gate House Strategies

A big change in 2025: The undeniable change in the federal regulatory environment, with significant cuts at the CFPB, FHFA, and to a lesser extent HUD. Many of the changes are certainly welcomed. But I’m concerned for lenders and servicers who now must deal with a much more complex environment created by more states filling that void.

An anticipated change in 2026: A rise in foreclosures, particularly in the FHA portfolio. It will result from policymakers moving away from the pandemic loss mitigation policies that extended well beyond the crisis.

Gerald Flood, Senior Consultant, Gate House Strategies

A big change in 2025: At the risk of stating the obvious, it has been the change in administrations, which naturally has dramatically altered the strategic priorities of HUD and the GSEs.

An anticipated change in 2026: We should see some progress on affordability for three combined reasons. Mortgage spreads are expected to tighten, as the Fed ends Quantitative Tightening (QT) by reinvesting runoff from its MBS and Treasury holdings. A revised proposal for Basel III Endgame is expected to clarify capital requirements in a way that encourages more bank holding of mortgage assets in portfolio. And passage of the ROAD Act should reduce regulatory burdens and boost the supply of affordable housing.

Earl Randall, Senior Consultant, Gate House Strategies

A big change in 2025: A big change happening in housing and housing finance for 2025 is Affordability. Here in Louisiana and across the Gulf South, Affordability due to the increased cost in insurance is taking its toll on homeowners. The increased cost of both hazard and flood insurance have increased mortgage payments substantially over the past decade with no relief in sight.

An anticipated change in 2026: I see more people feeling the economic pinch and I really believe the Affordability dialogue is about to change.

Hunter Kurtz, Partner, Gate House Strategies

A big change in 2025: The significant increase in insurance costs and the detrimental effect it has had on the development of new, multifamily affordable housing.

An anticipated change in 2026: I’m hopeful for the passage of the ROAD to Housing Act passing in some form which hopefully will allow for an increase in the number of Low Income Housing Tax Credit deals.

Michael Marshall, Partner, Gate House Strategies

A big change in 2025: One interesting change has been a late-2025 development following the passage of the GENIUS Act: the legitimizing of stablecoins and establishing them as regulated investment vehicles (banning unregulated stablecoins) and some crypto becoming accepted as an asset class — with institutional investors looking to it as a source of portfolio diversification.

An anticipated change in 2026: Both the bearing of fruits from heavy 2025 AI investment and the integration of blockchain into mortgage much faster than the industry may have anticipated, both in relation to stablecoin usage and to mortgage documentation.

Michael Waldron, Partner, Gate House Compliance

A big change in 2025: Strategy and resource decisions driven by evolving shifts in federal oversight and enforcement. While increased litigation and state-related oversight and enforcement have started to receive attention, the impact of the perceived "lull" is to come.

An anticipated change in 2026: Further consolidation of disparate vendor solutions and technologies with emerging end to end, programmatic mortgage solutions becoming the buzz by the end of 2026.

Keith Becker, Partner, Gate House Strategies

A big change in 2025: The persistence of the “Lock-in Effect”. Existing homeowners with very low interest rates have remained reluctant to sell and buy another home with much higher interest rates. This reluctance contributes to the tight inventory of homes available for sale and keeps upward pressure on home prices.

An anticipated change in 2026: The industry will continue to focus on cost management and increase its focus on leveraging AI to help in this effort. Aside from that, I do not see a sea change in any one area for 2026. The challenges in today’s housing market will take a few years to work itself out. Interest rates will stay in the low to mid-six range, inventory will stay tight, house price growth will moderate near 1%, and households will have to confront the high cost of housing in more creative ways such as increasing multi-family households and delaying life decisions such as starting families.

For more information, contact: FHAplus@gatehousedc.com.

THREE QUESTIONS

Joseph M. Gormley on Ginnie Mae.

Joe Gormley currently serves as the Executive Vice President and Chief Operating Officer of Ginnie Mae, responsible for the day-to-day operations of the organization. He is the president’s nominee to be President of Ginnie Mae.

Question: You returned to HUD in April of this year, after having worked in the private sector, joining Ginnie Mae at a really critical juncture. Going into next year, what do you see as the biggest priorities for Ginnie Mae in 2026? What do you hope will occupy your time?

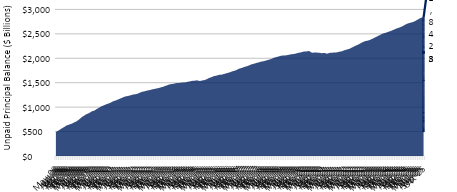

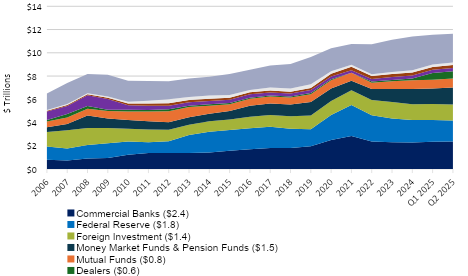

Gormley: Since the Great Financial Crisis, Ginnie Mae has seen substantial growth in the size of its portfolio. Today, Ginnie Mae has an over $2.8 trillion portfolio and has seen issuance on par or exceeding either of the GSEs for the last two years, and continues to function as a negative subsidy program, contributing more than $1.5 billion to the United States Treasury this past fiscal year.

With that growth comes greater responsibility. Our number one priority is optimizing the Ginnie Mae platform to ensure smooth and reliable operations for Issuers and investors. The Ginnie Mae guaranty carries the full faith and credit of the United States, which must always be our north star. Since issuing our first mortgage-backed security in 1970, we have never missed a pass-through payment to investors. This stability is critical to ensuring that Americans can continue to access affordable homeownership and rental opportunities through the federally insured or guaranteed mortgage programs.

Growth of Ginnie Mae MBS Guarantee Portfolio

In the immediate term, we’ll be looking for efficiencies and ways to increase transparency. The capital markets team at Ginnie Mae has been working to create new disclosures on our securities that provide more information regarding characteristics of the loans underlying the securities. These new disclosures should help investors with modeling prepayment activity and assess the relative performance of the Ginnie Mae security. Ginnie Mae also hopes to align our requirements for liquidation reporting with other large participants. The liquidation file data exchanges are used by market participants to monitor inventory, manage risk and ensure accurate settlement and accounting reporting. More frequent liquidation reporting will also provide Ginnie Mae important information to help keep the program resilient to various types of operational interruptions.

We are also increasing the velocity of our initiative to evolve Ginnie Mae from pool-level operation to loan-level operation. At its core, we want to enable individual loan servicing transfers which is a long time industry ask and should improve liquidity in the Ginnie Mae MSR market. This transformation will involve a wide range of processes, systems, and controls to ensure loan quality, compliance and accurate cash flows. These operations will impact underwriting, servicing, securitization and investor reporting. The net effect of this transition will be to provide more precision cash flow tracking for managers and investors; more effective prepayment, delinquency, and loss mitigation modeling; error reduction and – we believe - lower costs in originations, servicing and securitization. This is a fundamental shift in program operations and requires a steady and methodical approach to ensure no disruptions to current state. I hope to be able to share more information soon on the policy framework we’re developing as well as a timeline for action.

Question: You spoke about the global capital which enables affordable homeownership and rental opportunities through Ginnie Mae. In what ways are global investors changing or their interest evolving? What are the key factors that will enhance the liquidity for this government insured market?

Gormley: Ginnie Mae’s mission is to be a stable source of liquidity for the government-insured mortgage market and doing so ensures that there is a reliable secondary outlet for loans made to low- and moderate-income, veteran, rural, and Tribal borrowers. The explicit government guaranty attracts global capital to our domestic housing market and in doing so creates a deeply liquid product which participates in the largest fixed-income market after US Treasuries. The YTD average daily trading volume for agency MBS was $353 billion as of month-end October 2025, an increase from the daily average of $305 billion for calendar year 2024. This represents the highest average daily trading volume in the past 20 years.

Ginnie Mae new issuance steadily grew with $416 billion in total YTD gross issuance, leading either Fannie Mae or Freddie Mac. The attractiveness of the Ginnie Mae security remains strong in comparison to sovereign fixed income securities of similar or longer duration.

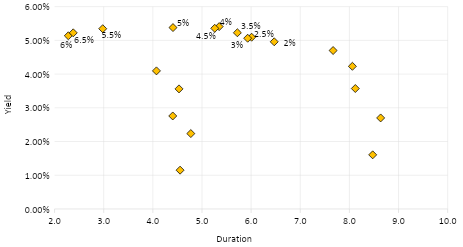

Global Product Yield Per Duration: Yield versus Duration

Despite modest year-to-date declines, Ginnie Mae II MBS hedged yields remained near 2.0 percent in JPY (Yen) and 3.4 percent in EUR (Euro), continuing to offer favorable relative value for overseas investors.

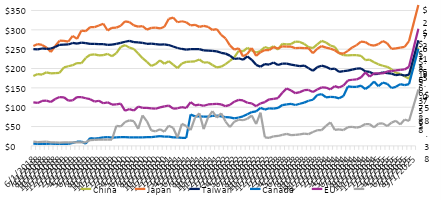

Agency Debt Investor Breakdown

Top Foreign Holders of Agency Debt

Another trend we’re seeing is the rise in demand for Custom pools, largely fueled by collateralized-mortgage obligation (CMO) issuance. Broker dealer CMO desks are building Custom pools with superior convexity characteristics and removing loans with positive prepay stories from TBA-eligible pools, resulting in higher concentrations of FHA loans in Custom pools and higher concentrations of VA loans in TBA-eligible pools. VA loans have grown as a proportion of total Ginnie Mae gross issuance. VA loans accounted for only 14.6 percent of total gross issuance in 2008 but now account for approximately 40.7 percent of gross issuance in 2025 YTD. Federal Housing Administration (FHA) remains the largest loan program, comprising 57.5 percent of Ginnie Mae collateral in 2025 YTD.

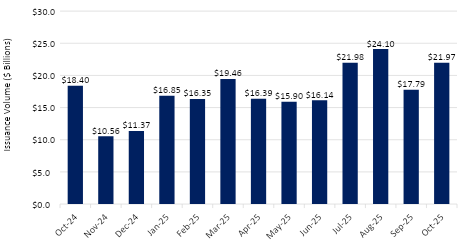

Lastly, it’s worth mentioning that in addition to robust MBS pass-through activity, real estate mortgage investment conduit (REMIC) production played an important role in Ginnie Mae’s capital market operations this year. These transactions allow investors to structure cash flows and manage prepayment risks in ways that aligned with diverse investor needs, broadening the program’s appeal and strengthening overall market efficiency. Demand for REMICs remained strong, reflecting not only healthy trading activity but also the resilience of the housing finance system.

Ginnie Mae REMIC Issuance Volume Oct 2024 - Oct 2025

Question: Can you comment on Ginnie Mae and technological innovation, and how AI and other major developments are affecting all of the above?

Gormley: Cybersecurity is a priority of the Trump administration and Ginnie Mae is no different. Protecting our systems and critical assets is always top of mind, and our cybersecurity program continues to evolve as threats grow more sophisticated. We are strengthening and modernizing defenses to stay agile in a fast-moving threat environment. This effort includes close collaboration across every office at Ginnie Mae to ensure platform resilience. In addition to hardening internal systems, Ginnie Mae continues to deepen engagement with counterparties as part of a holistic cybersecurity strategy. Our processes and controls are designed to identify, prevent, detect, respond to, and mitigate risks more effectively.

To improve early visibility and response, Ginnie Mae implemented a 48-hour cybersecurity incident notification requirement for Issuers and Document Custodians. This policy has enhanced our ability to monitor risks in real time and coordinate timely mitigation efforts. Strengthening our cybersecurity framework remains a central focus as we continue maturing our enterprise capabilities. These actions ensure that Ginnie Mae remains proactive in managing emerging threats. Our goal is to maintain a resilient, trusted platform for Issuers, investors, and stakeholders.

Some of the most valuable technology modernization work happens behind the scenes, yet it is vital to the continuity of the Ginnie Mae platform. This transition included retiring end-of-life technologies and moving to cloud-based Infrastructure, Platform, Software, and Data-as-a-Service solutions. The result is improved system availability, stronger cybersecurity, enhanced resiliency, and the elimination of single points of failure. These upgrades underscore our commitment to modern, dependable IT services.

As part of this modernization, Ginnie Mae streamlined several legacy technologies and integrated public-facing tools into a single access point through the MyGinnieMae enterprise portal. This unified experience simplifies interactions for Issuers and reduces operational complexity across the platform. By modernizing both visible and behind-the-scenes components, Ginnie Mae delivers greater stability, transparency, and efficiency to its partners. These enhancements strengthen the digital foundation that supports the mortgage-backed securities ecosystem. Together, these improvements ensure that Issuers have the tools and reliability they need to succeed.

INSIDE VOICES

What we’re hearing around Washington and the industry

Government Reopening: Secretary Turner wasted no time signaling HUD’s aggressive comeback the moment the government reopened—rolling out a major $3.9 billion competitive funding offering as an innovative attempt to address and eradicate root causes of homelessness. FHA is also hitting the ground running, and it shows: FHA immediately issued a waiver of Form HUD-92900 (Important Notice To Homebuyers) reducing redundancies, streamlining workflows, and smoothing the borrower experience.

FHA Delinquencies: The MBA reported that as of Q3 2025, the delinquency rate for FHA loans rose to 10.78% (seasonally adjusted). Stressors cited include a softer labor market, rising personal debt obligations, and sharp increases in taxes and insurance that are squeezing already-thin affordability. To make matters worse, home-price declines in certain markets may also limit a borrower’s ability to sell or refinance, further elevating default pressure.

GSE IPOs: Pershing Square CEO Bill Ackman has stepped back from earlier GSE merger ideas and is now stressing a simpler path and suggests a relisting of Fannie and Freddie on the NYSE to reopen institutional investment. He argues that a clear roadmap out of conservatorship and clarity on FHFA’s future authority are essential to restoring the companies as attractive investments. There is a lot on the table, the two firms reported over $6 billion in net income in 3Q.

Speaking of FHFA: Director Pulte recently noted that the GSEs are looking at ways to take equity stakes in technology companies. And new product ideas such as a 50-year mortgage and a portable mortgage are being bantered about, reflecting a willingness to consider new solutions. That said, many good questions have been raised, clearly there’s a lot to think about. May the best ideas win…

AI, what next? Enterprise-level AI integration is now affecting competitiveness, accessibility, and the borrower experience across the mortgage ecosystem. A lack of coherent regulation is increasingly possible as states try to write AI rules. The Administration recently called for one unified federal AI standard, warning that a patchwork of state rules threatens innovation and economic growth. However, the states aren’t on board, at least so far…

CFPB News: President Trump nominated Stuart Levenbach to lead the CFPB—an appointment expected to align with the Administration’s ongoing effort to recalibrate the Bureau’s scope and enforcement posture.

THE GATE HOUSE INDEX

The Gate House Index and analysis is designed to provide insight into the status of FHA’s business at a moment in time and over a period of time, as well as other pertinent data points we’re following.

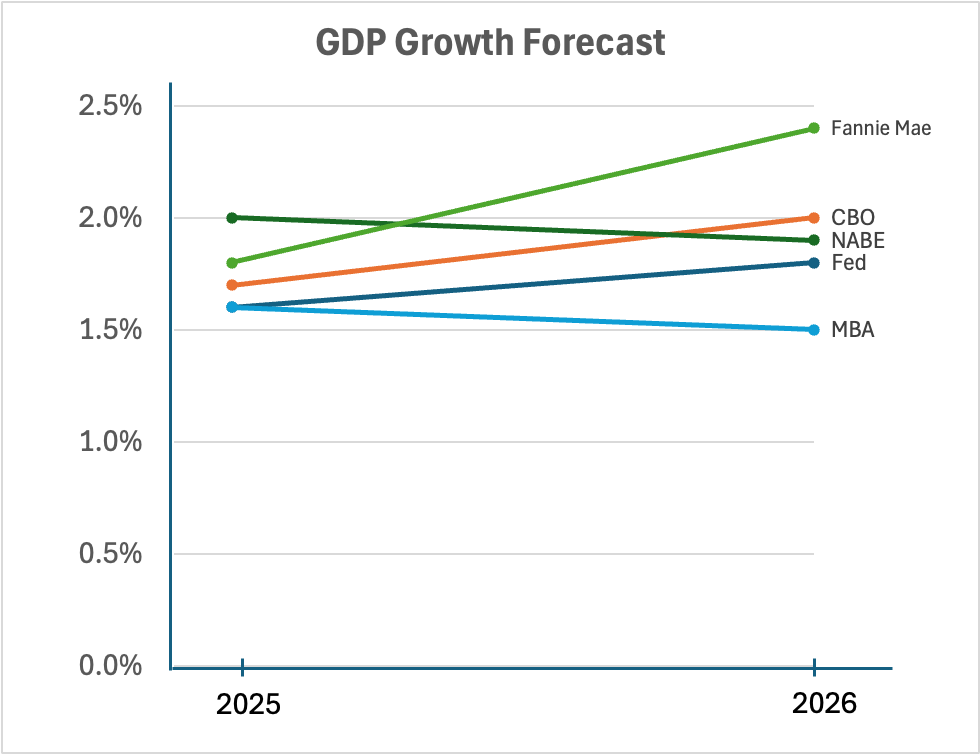

This month, we look at forecasts of important economic and housing market indicators beginning with the GDP forecast from several sources which average 1.92% for 2026.

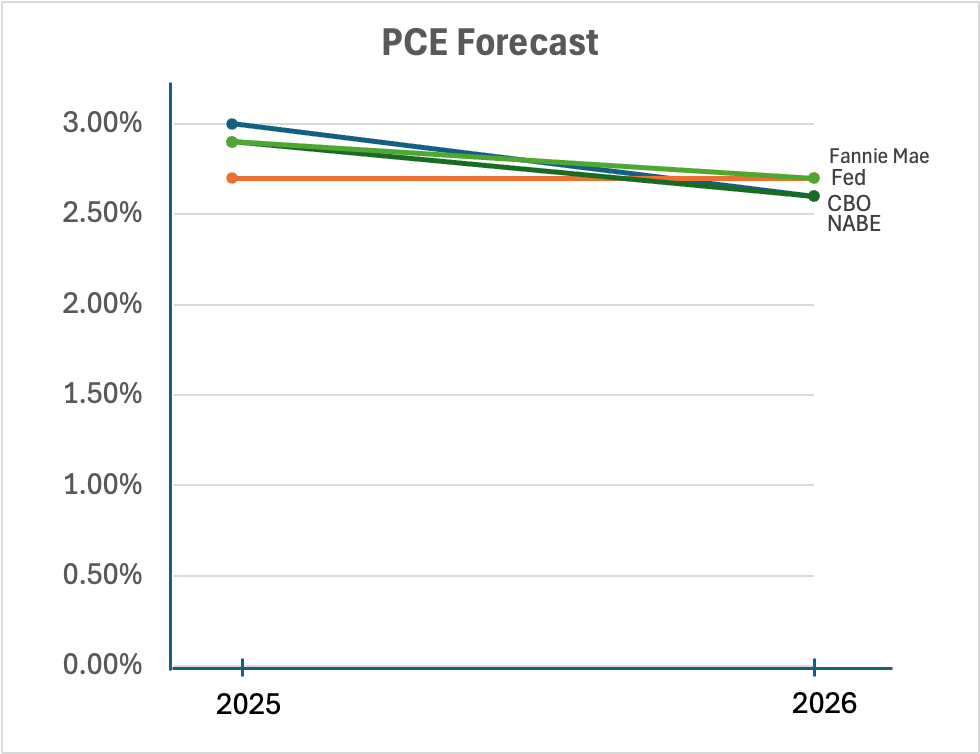

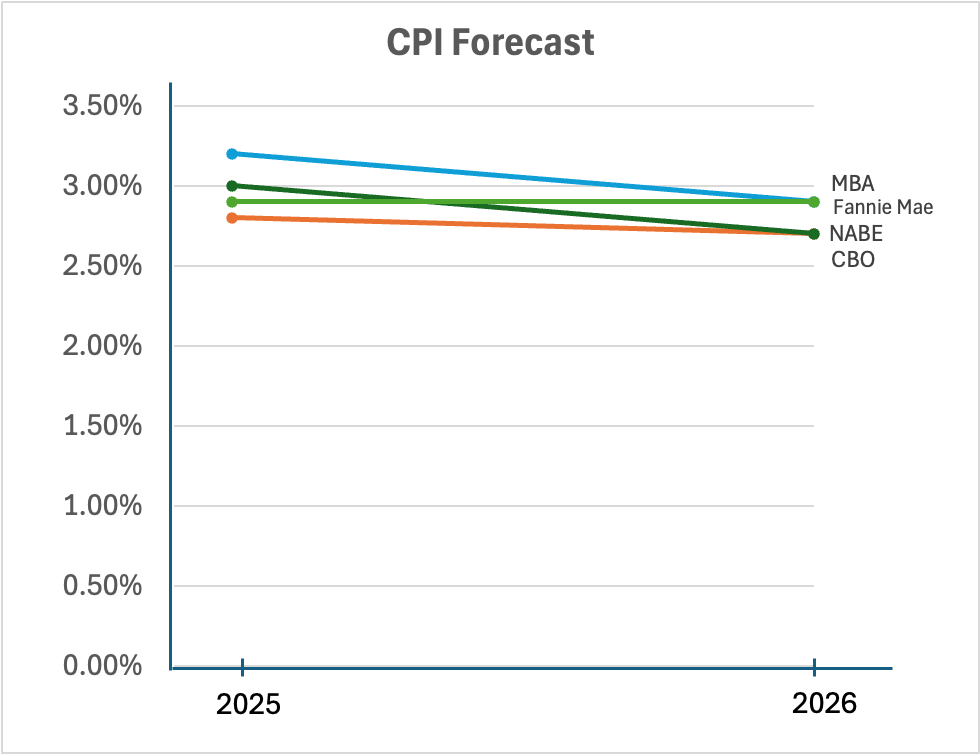

The Personal Consumption Expenditures Deflator (PCE Deflator ), the Federal Reserve's primary inflation gauge, and the Consumer Price Index (CPI) are predicted to decline to averages of 2.65% and 2.8%, respectively, but remain above the Fed’s target inflation level.

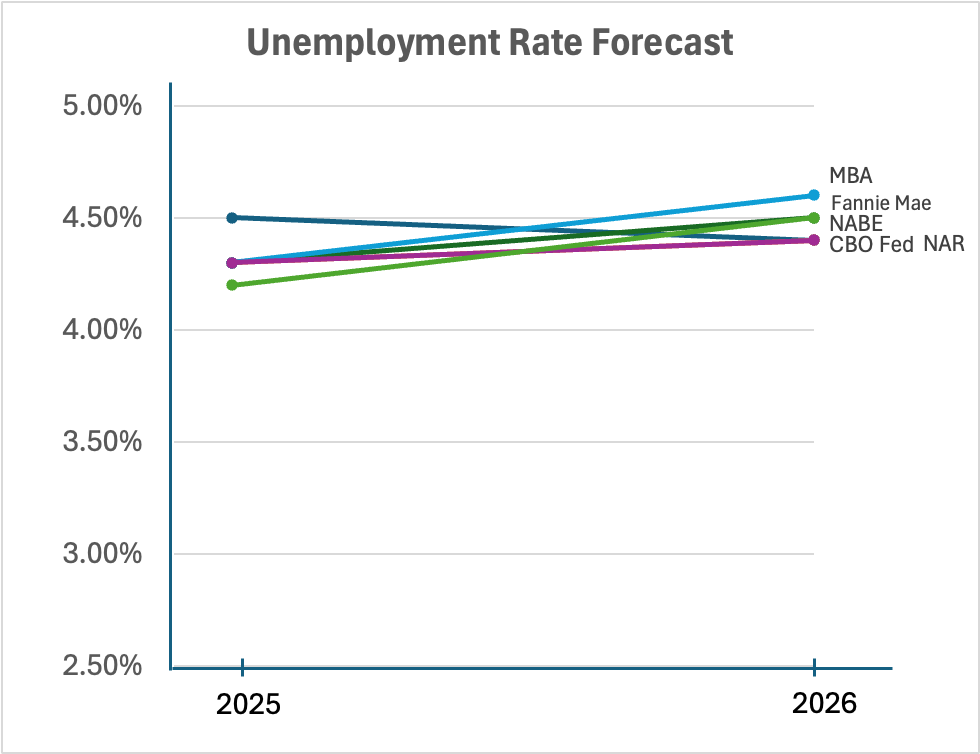

Unemployment is forecasted to rise slightly, with average expectation about 4.5%.

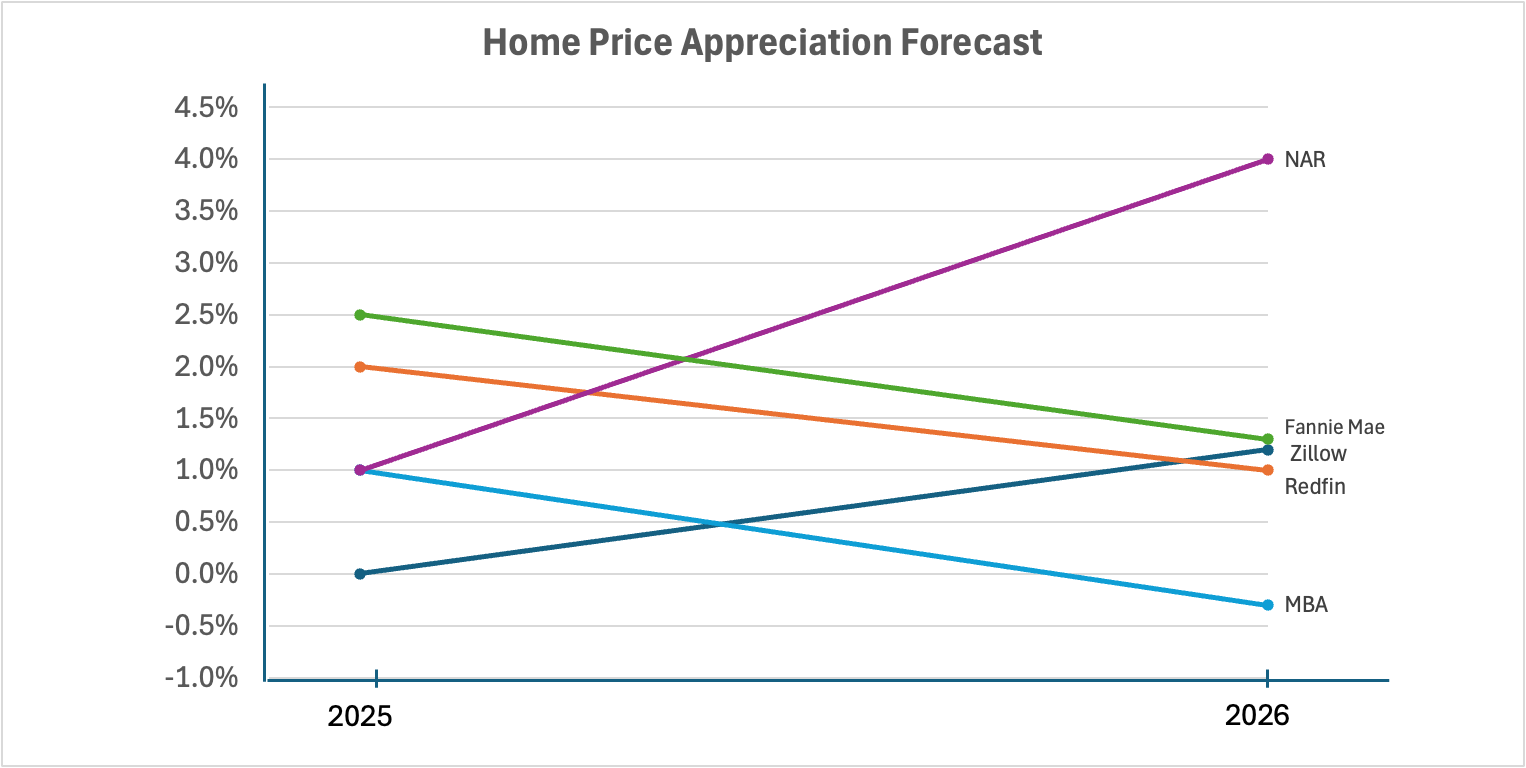

Home price appreciation is forecasted to run slightly below expected inflation, with the average forecast 1.9%.

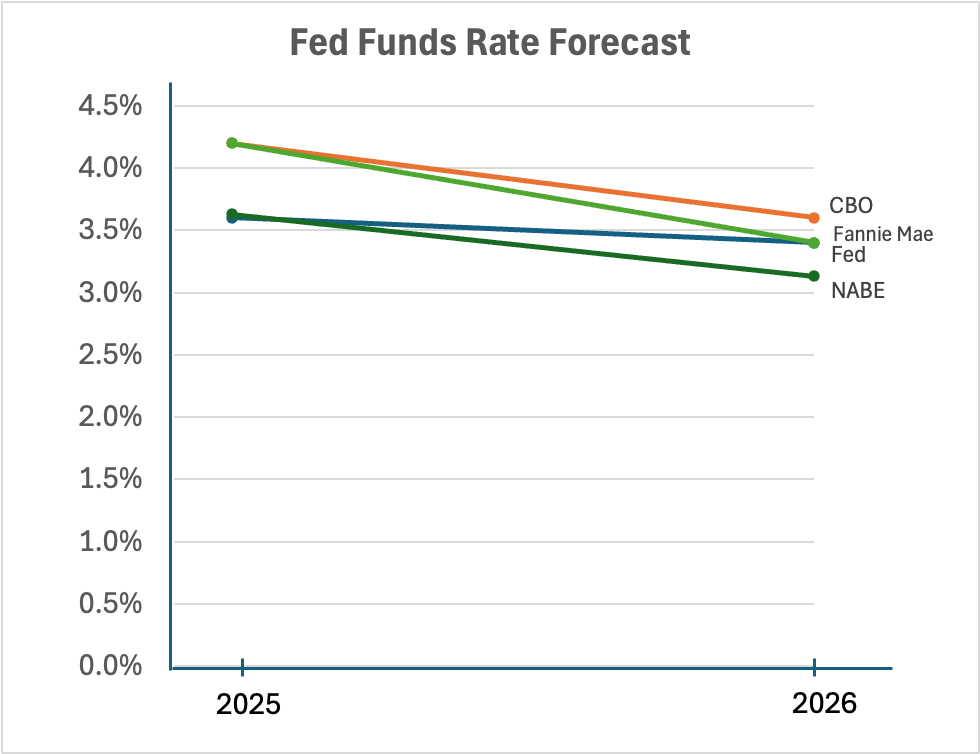

The Fed Funds Rate is forecasted to fall to 3.4%, on average.

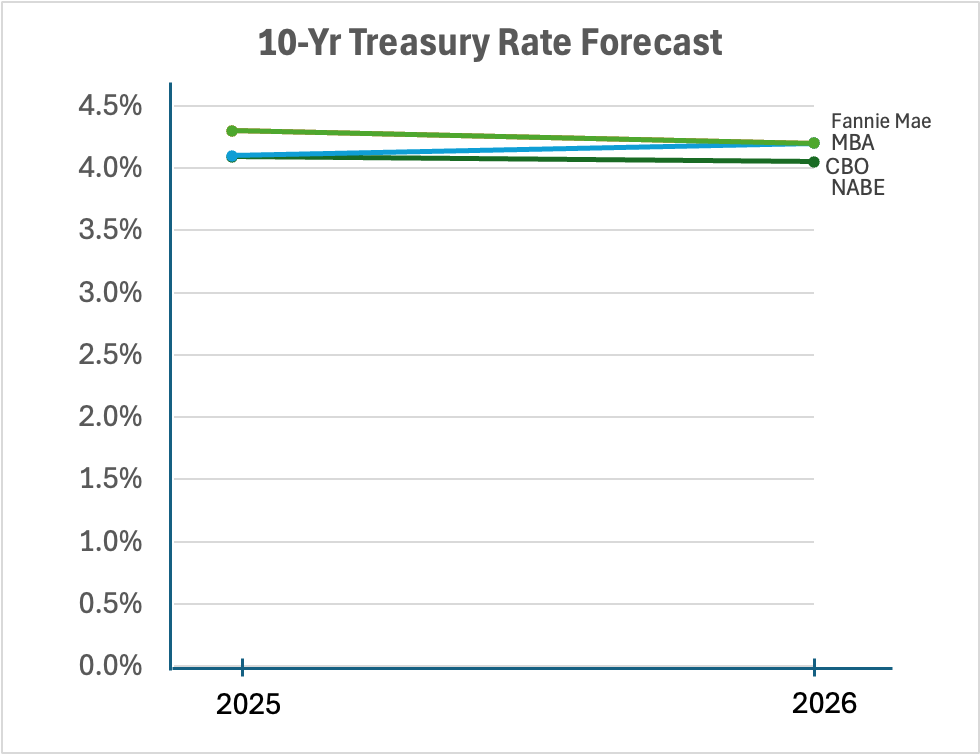

The 10-year Treasury is forecasted to be relatively stable, with forecasts averaging about 4.2%.

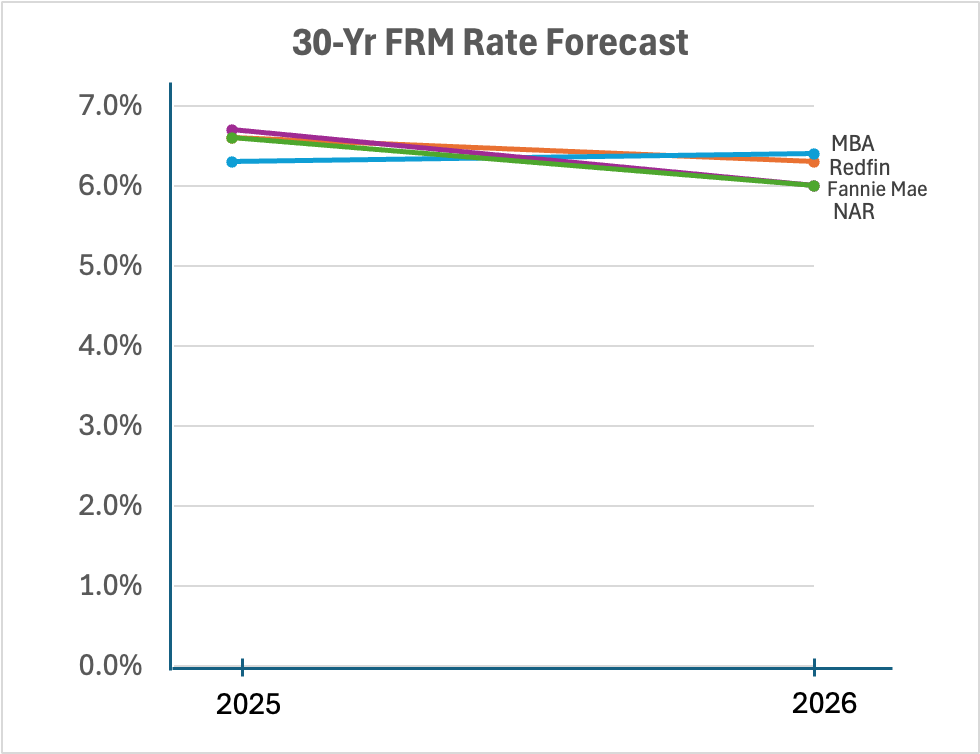

And the 30-year is forecasted to run, on average, 6.18%.

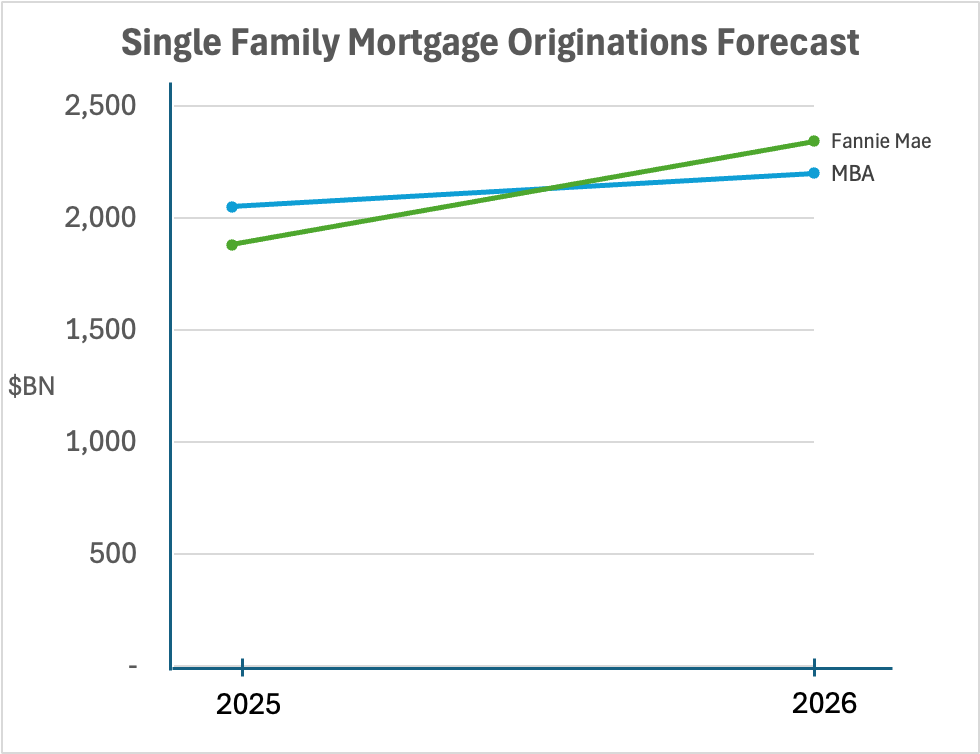

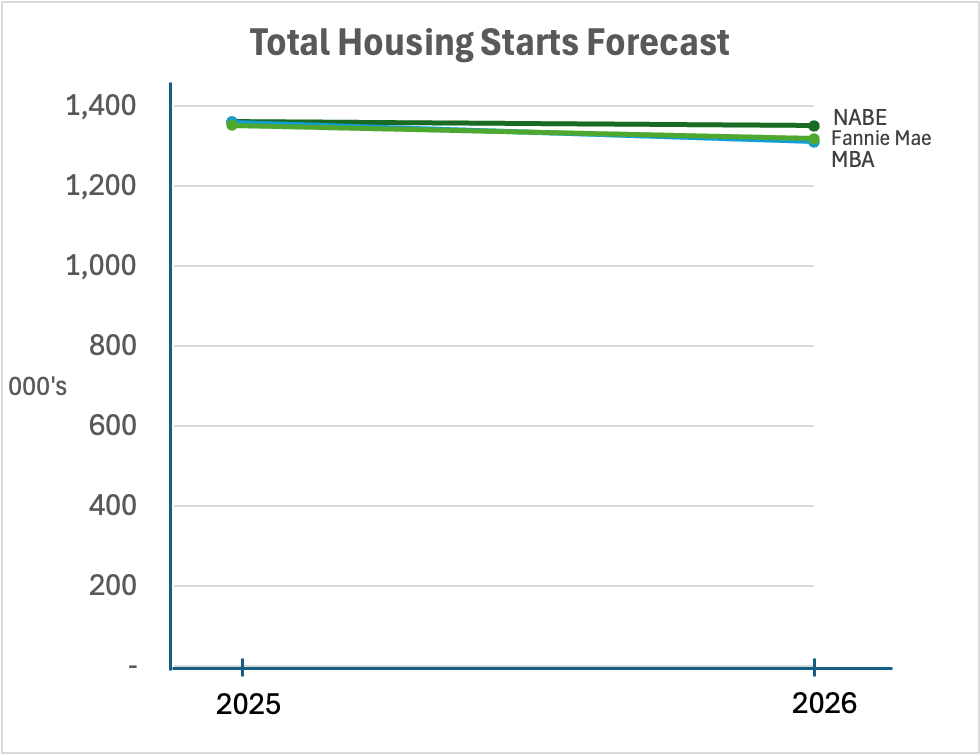

Single family originations are forecasted to rise to $2.27 trillion, housing starts on average 1.3 million units and home sales just over 5 million.

This Month In History

FHA insured its first Title II mortgage loan in December 1934. The $4,800 20-year fixed-rate loan to Mr. and Mrs. Warren H. Newkirk for their property at 30 Hopper Avenue in Pompton Plains, NJ was originated by Prospect Park National Bank of Paterson NJ.

...And a picture of it today…

... and of Arthur L. Walsh, FHA regional director, signing the commitment on December 21, 1934.

FHA+ is published monthly by Gate House Strategies, a Washington, DC area-based advisory firm focused within the financial services, mortgage lending and servicing, community development, and public housing sectors. Contact us at FHAplus@gatehousedc.com