This Issue Includes:

- Think Piece: Michael Waldron on litigation mitigation strategies as federal enforcement declines and state/private actions rise.

- Three Questions: Keith Becker on Buy Now, Pay Later — data gaps, underwriting risks, and potential regulatory action.

- Inside Voices: Shutdown impacts, ROAD to Housing developments, reverse mortgage reform signals, FICO changes, housing supply pressure, and rising AI-related fraud.

- Gate House Index: Enforcement trends, BNPL growth and delinquency data, state activity, and historical FHA context.

THINK PIECE

Managing Risk and Maximizing Opportunity Through Litigation Mitigation

by Michael Waldron

Ideological differences between presidential administrations have been known to produce swings in the federal posture toward business for many years. The change in point of view of federal oversight agencies under Trump 2.0 in 2025 has been particularly acute and has already shifted the litigation landscape. Wolters Kluwer reports that federal agency enforcement actions in the first half of 2025 in the areas of consumer protection, competition, and financial practices were down 37% compared to the second half of 2024 and the associated penalty amounts were down 33%. [1]

While federal government enforcement actions have declined, prior experience suggests that state attorneys general and the plaintiffs’ bar will become increasingly active. During the first Trump term (that also saw a reduction in federal actions) there was a near immediate pick up in state enforcement actions, including multi-state actions. There has also been an increase in private enforcement actions in 2025, many based on state laws. In other words, even with a decline in federal enforcement actions, there is no rest for the weary within lender and servicer compliance operations.

“It's no coincidence that in the lull of regulatory pursuits by the federal government, litigation brought by state attorneys general and private parties is on the rise,” says Daniella Casseres, partner and head of the mortgage regulatory practice group at Washington, DC-based law firm Mitchell Sandler. “Plaintiffs are out there who have a real interest in bringing claims which maybe the feds aren’t picking up now.”

“The challenge is the unpredictability and often unfounded nature of these emerging threats,” says Casseres. The reality is litigation for many mortgage lenders and servicers is not a matter of if, but when and we’re seeing anecdotally an increase in our clients who require very specialized support in litigation matters initiated by state AGs and qui tam whistleblowers.

That is to say, it is a critical time to assess the risks from state and private party actions, and moreover to build a culture of compliance that serves customers properly, protects against mistakes or inadvertent errors, and reduces expected litigation costs.

The costs involved in defending, even successfully, against these actions that seem to come out of nowhere can be high. While firms can estimate the cost of defending such accusations from financially motivated relators, for example, it’s difficult to quantify the reputational costs that often coincide with even spurious accusations.

When regulatory or legal issues shift, industry best practice is to review and refine compliance platforms to ensure that the right internal framework is in place and lenders are prepared to navigate the evolving challenge most efficiently and effectively.

“It comes down to asking what can be done proactively to better position the business for the possible litigation,” John H. Lawrence, partner at law firm K&L Gates and lead counsel in securing dismissals of numerous False Claims Act suits.

A “litigation mitigation” strategy goes beyond normal, well-functioning compliance management. Traditional litigation management tends to be reactive in nature and typically breaks down into three categories once a suit has been filed: expert witness testimony, investigative support, and third-party oversight and monitorship. All are important and invaluable when things go south. Litigation mitigation significantly reduces the possibility and potential expense – legal costs, penalties, management distraction, reputational damage, etc. – that can come with litigation.

Implementing a comprehensive strategy ahead of time can optimize the outcome when a firm faces unexpected regulatory or legal challenges. The ability to demonstrate a comprehensive and intentional compliance program to regulators and enforcement agencies yields real results. “Settlements from qui tam cases in which the Justice Department intervenes typically carry a much higher price tag compared to those when the Justice Department declines. For example, in Fiscal Year 2024, the Justice Department recovered $2.2 billion from intervened qui tams, compared with $218 million in declined qui tams,” Lawrence said.

From the perspective of our team, it starts with a clear-eyed reevaluation of a lender’s or servicer’s current compliance management system. There are specific, tangible steps that can be taken now to assess internal standards and policies:

- Assure appropriate levels of oversight by the board

- Evaluate issue escalation processes for timeliness to appropriate level of management

- Analyze customer calls and QC results for patterns and positive or negative trends

- Rate the quality of document retention, file stacking and maintenance

- Review vendor contracts for potential exposures

- Look at how artificial intelligence is employed and its potential impact amid potential legal actions

- Consider how best to enhance compliance automation

- Research recent and ongoing enforcement actions; identify strategies and factors that were critical to the greatest successes and failures (And remember, as Mark Twain may have once said, “history doesn’t repeat itself, but it often rhymes”)

In short, develop operational compliance structures and install them in advance to make a positive difference in future negative scenarios.

The extra effort is worth it. Casseres and Lawrence say they’ve seen the investment in litigation mitigation payoff repeatedly. Beyond the significant savings in time and resources, having a litigation mitigation strategy in place actually strengthens a lender’s market position. It will improve the quality of the lender’s work, attract solid partners and create advantages by projecting confidence in the products and services it delivers to the marketplace.

And those are things you never want to be complacent about.

For more information, contact: FHAplus@gatehousedc.com.

[1] “Regulatory Violations Intelligence Index July 2025”,

[2] “Protecting Consumer Protection: Filling the Federal Enforcement Gap”, https://digitalcommons.law.buffalo.edu/cgi/viewcontent.cgi?article=4923&context=buffalolawreview

[3] “What goes down comes back up: Federal agency enforcement actions drop and private enforcement class actions rise”,

THREE QUESTIONS

Keith Becker on Buy Now Pay Later.

Buy Now, Pay Later (BNPL) is short-term consumer financing that has become a common payment method for both online and in-store purchases. Popularized by services like Klarna and Affirm, BNPL allows consumers to make purchases, then pay off the debt in a series of installments. Proponents laud consumer access to interest free credit, while critics point out that many BNPL obligations are not captured in traditional credit reports, which can create “invisible” debt that undermines accurate debt-to-income assessment. The mortgage industry has begun to consider the increased usage of BNPL options, with FHA recently issuing an RFI on BNPL on June 25, 2025. In this month’s “3 Questions,” Gate House partner Keith Becker shares his thoughts on the widespread and growing use of BNPL.

Question: Many housing and housing finance groups have been voicing their strong cautionary views on Buy Now, Pay Later. What’s fueling their concerns?

Becker: People are expressing caution around BNPL simply because there’s not yet enough known about its impact. The right amount of the necessary data hasn’t been collected. The industry doesn’t have the information it needs to draw conclusions on the use of BNPL and how it impacts borrower performance.

That’s not a good place for us to be, as the use of BNPL is growing rapidly, with the number of consumers using the BNPL feature close to ninety-two million this year. And it’s projected to continue to grow. More than a third of them are frequent users. BNPL users also tend to be younger, have lower income, and are renters rather than homeowners. In fact, according to a recent Lending Tree survey, nearly one in four users report having three or more active BNPL loans at one time. Not only are folks using it for their online purchases, but also for things like deliveries from DoorDash and Grub Hub. BNPL purchases of groceries and other essentials are rising as well, which could be an indication of increasing household stress.

In June, FICO announced it has plans to soon begin incorporating BNPL data into credit scores. That kind of thing is a good first step toward reducing the invisibility problem. But all other credit scoring vendors must also universally adopt it. BNPL providers should also be required to report standardized data to the three main credit repositories.

Until then, BNPL continues to operate generally outside bureau reporting. That means underwriters may miss stacked or overlapping BNPL obligations that increase borrower leverage. This really does threaten accurate assessment of DTI ratios and payment history.

Question: So then, what needs to be done?

Becker: The most urgent need is good data. We’ve got to get to the point quickly where we are collecting and tracking reliable information, so that we better understand whether BNPL has a positive, neutral, or deleterious effect on borrower and mortgage performance. Without it, we’re only speculating.

For now, large mortgage investors and insurers may want to consider reinforcing, through industry communications, what is already required on the uniform mortgage loan application. That is, borrowers already are required by law to list all debts, including all their monthly revolving and installment debts, which BNPL falls into, no matter how short-term it is. Doing so would enhance data collection for analysis and modeling, as well as lead to better informed credit decisions.

In the meantime, as the industry and regulators gather and analyze more data, lenders can serve as an important stopgap. You know, lots of people in the pipeline may be saying, “Oh, BNPL is an installment debt with less than 10 months remaining, so we can ignore it in underwriting.” Well yes, potentially -- but the exclusion of short-term debt is not absolute. To be excluded, FHA requires total short-term debt payments to be <5% of borrower income and the GSEs require that these payments not materially affect the borrower’s ability to meet credit obligations. If the lender believes that those payments that are less than 10 months in duration are consequential, and usage appears to look more like revolving debt, they are required to include the payments in the DTI calculation or require it to be paid off.

Mortgage investors and insurers rely on lenders to adequately assess the impact of this new financing option on a borrower’s ability to repay the debt. And underwriters should remain diligent in reinforcing the existing standards around installment debt. You’ve got to have the steel to say tough things sometimes like, “You’re consistently borrowing money on a short-term basis, you have little remaining savings, you’re at the max DTI. How are these BNPL loans getting paid?” There will be times when a loan should be denied for excessive obligations.

Question: What’s the outlook for action in Washington?

Becker: It’s clear that HUD, FHFA and the GSEs intend to become better informed on the issue. It’s too big to ignore the potential long-term impact. And as you mentioned, a broad spectrum of the housing and consumer groups have weighed in already, including the Mortgage Bankers Association, the National Association of REALTORS, The Consumer Federation of America, and the National Association of State Housing Agencies. All have flagged a combination of concerns, from underwriting and FHA risk to consumer harm and overextension. We may very well see regulatory requirements for standardized disclosures to consumers on BNPL loans. A TILA-like disclosure could be the best practice.

And remember also that the institutional investors and venture capitalists who are behind the BNPL firms are well represented in Washington. BNPL providers are arguing for a measured approach to new requirements, emphasizing low BNPL loss rates. However, without good, standardized data, accurate payment histories, and loan performance over time are not known. At least one recent study suggested more than 10 percent of BNPL borrowers were assessed late fees in 2021.

Ultimately, I believe the BNPL product should be more transparent, that is, subject to standard regulations and oversight, and integrated into the traditional credit reporting ecosystem.

INSIDE VOICES

What we’re hearing around Washington and the industry

Shutdown Squeeze: The federal shutdown continues to ripple across housing agencies. The real pinch comes from limited staff and stalled policy work, leading to some delays in program reviews, lender approvals, and guidance updates. Most loan operations remain on track, but uncertainty around FHA processing, Ginnie Mae oversight, and policy timelines persists. Still, there’s cautious optimism that Washington will strike a deal soon.

Surprise Housing Play: A big surprise was tucked into the National Defense Authorization Act (NDAA) for Fiscal Year 2026: the Renewing Opportunity in the American Dream (ROAD) to Housing Act of 2025. What started as a defense bill suddenly turned into a housing-policy moment, and an important one. This is a good reminder that housing issues are finding their way into unexpected places on the Hill, and this could have real implications for how federal housing programs evolve next year.

The ROAD to Housing: This bill’s key provisions include reforms to housing-especially HUD related programs and opportunities such as counseling and financial-literacy programs, lifting caps on rental-assistance, streamlining zoning and environmental reviews, boosting production and preservation of affordable homes (especially in Opportunity Zones), and expanding access to homeownership and manufactured/modular housing.

Reverse Mortgages: FHA recently dropped an RFI on the future of the HECM and HMBS programs. They’re asking whether the program still serves its purpose of helping seniors tap home equity, how to fix liquidity and market issues, and what reforms could reduce risk to the insurance fund. Changes could be coming to how reverse mortgages are structured, funded, and serviced. This is a good time and opportunity for the industry to weigh in.

Credit Score Headlines: FICO launched its Mortgage Direct License Program, which permits a bypass of the traditional credit bureaus. This move could lower costs for lenders and brokers, reduce the role of resellers, and reshape the tri-merge credit market. However, the devil is in the details and there are a lot of moving parts and implications to sort out.

Building Housing Supply: FHFA is calling on builders to ramp up efforts to tackle the nation’s housing shortage. This could be a tough challenge for an industry juggling labor, land, and lending constraints. That said, any move that adds affordable supply and/or eases builder constraints deserves kudos.

Not a Deepfake: Mortgage and AI-driven fraud are rising fast, according to the 2025 Cotality Fraud Report. Cotality’s Mortgage Application Fraud Risk Index climbed 6.1% nationwide over the past year, highlighting growing threats from identity, income, and transaction schemes. The sharpest increases are showing up in “transaction risk” cases such as hidden concessions, non-arm’s-length deals, and property flips which are up 4.6% year over year.

THE GATE HOUSE INDEX

The Gate House Index and analysis is designed to provide insight into the status of FHA’s business at a moment in time and over a period of time, as well as other pertinent data points we’re following.

This month, we look at important figures related to litigation trends and Buy Now Pay Later.

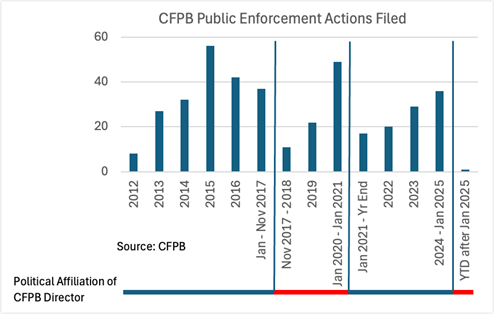

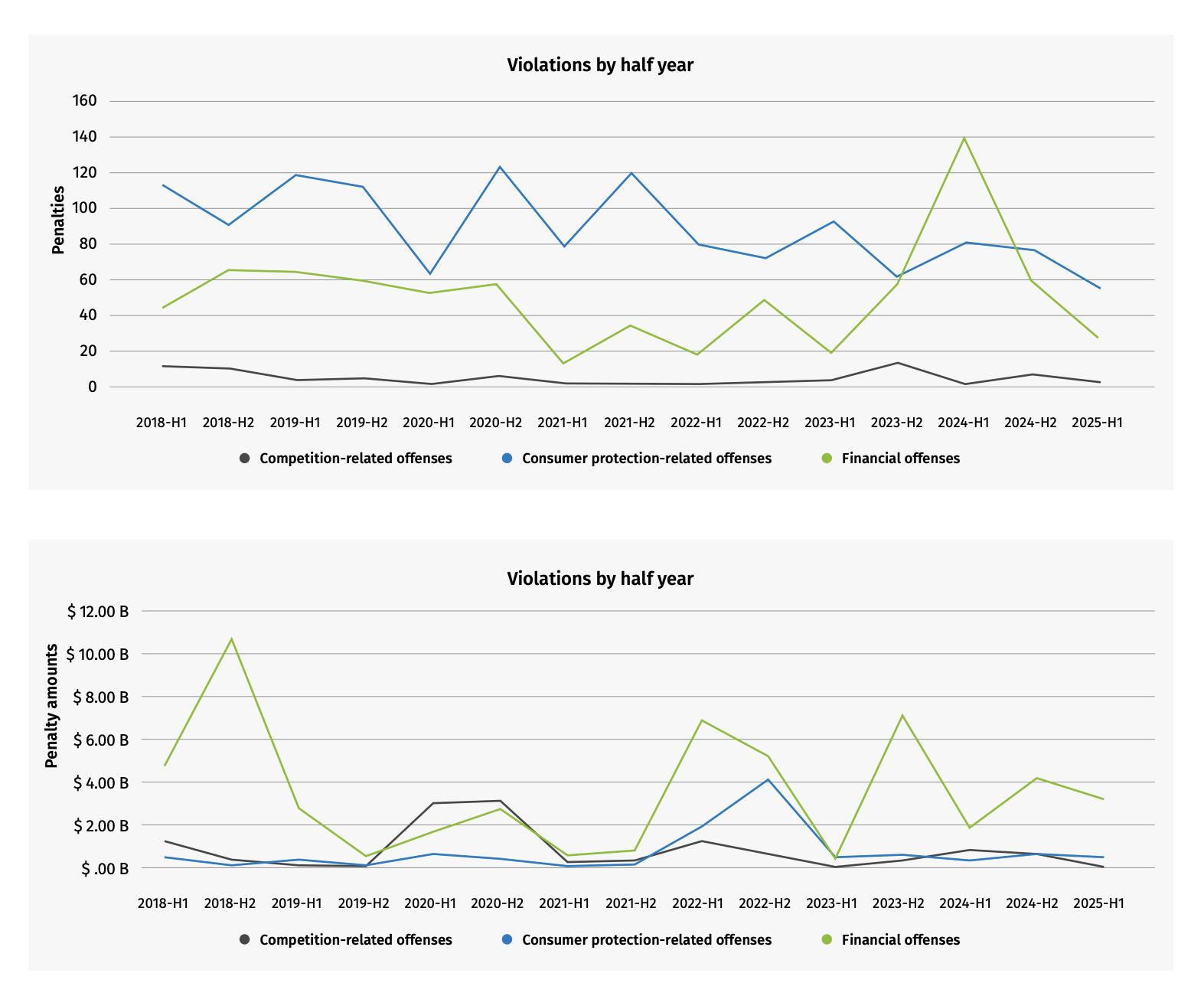

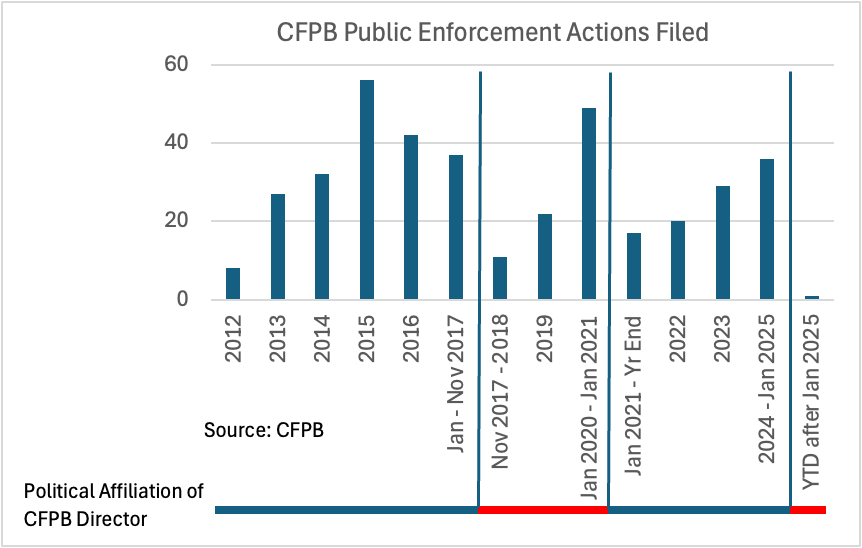

In the following charts, we can see combined federal enforcement actions for Competition, Consumer Protection, and Financial practices declined 37% in 1H25, led by a >50% decline in the number of Financial practice violations. Of note — "The largest [Financial practice] violation in H1 2025 was a ... $1.37 billion [penalty in April] for unsafe banking practices including failing to establish and maintain a compliance management system."

We do not expect CFPB enforcement actions in the near term (3+ years)

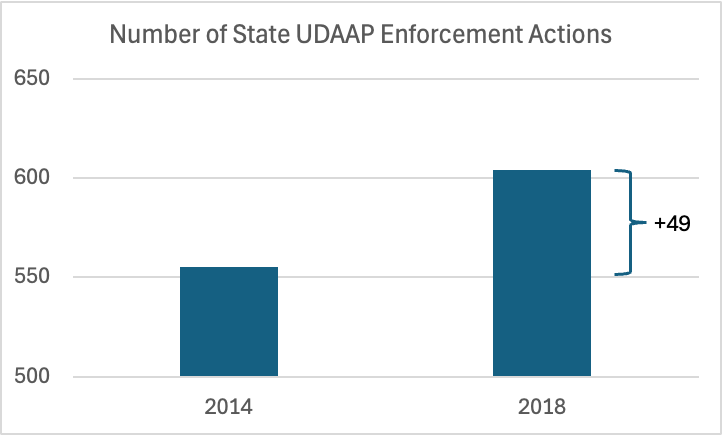

The increase in state enforcement actions for Unfair, Deceptive, or Abusive Acts or Practices (UDAAP) between 2014 and 2018 offset a decline in federal actions:

Based on 38 states for which public records or open records requests provided required documents for both years.

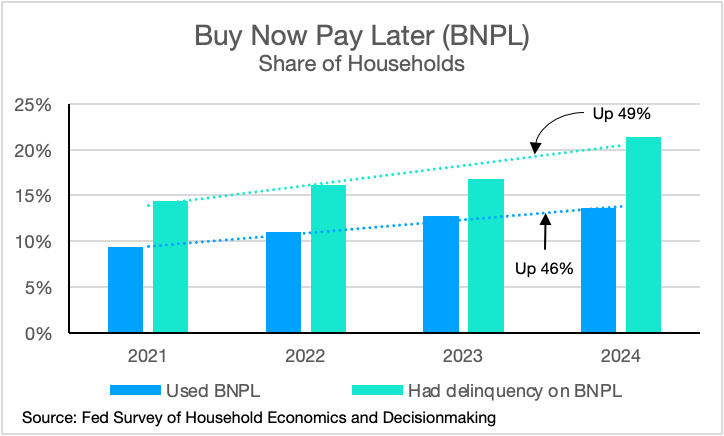

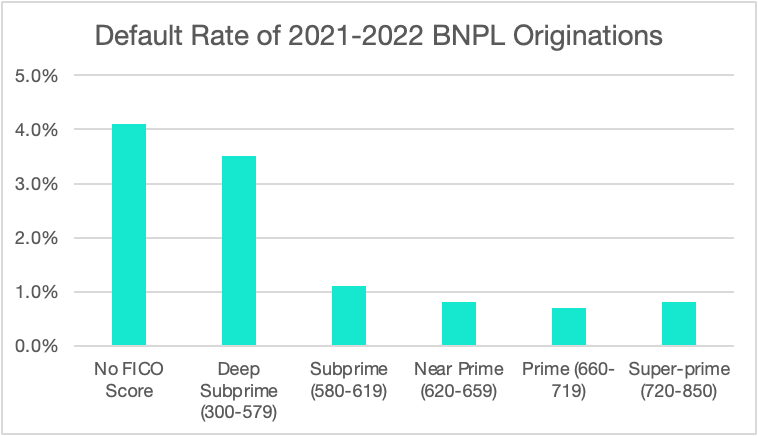

BNPL usage and delinquencies increased nearly 50% between 2021 and 2024

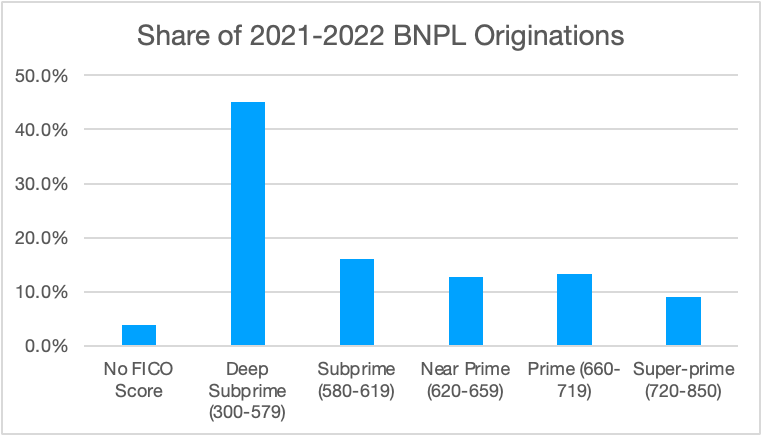

More than 60% of 2021 and 2022 BNPL originations were subprime (FICO < 620)

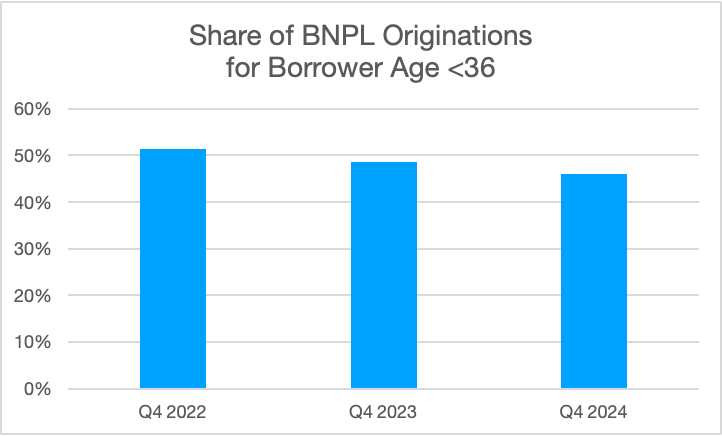

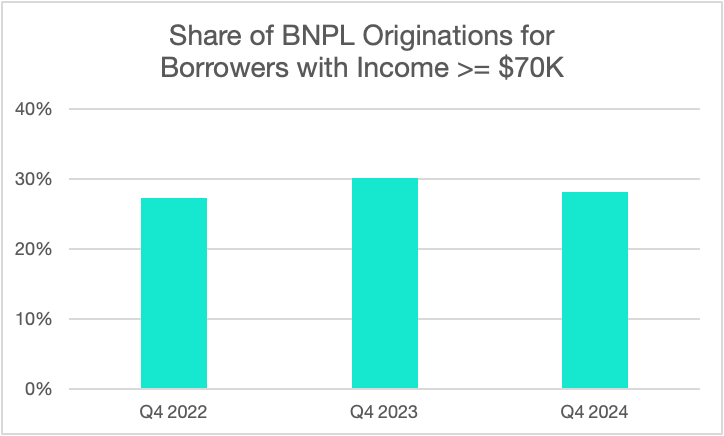

BNPL borrower demographics appear to overlap with prospective 1st-time homebuyer demographics

This Month In History

In November of 1934, FHA published and implemented its Mutual Mortgage Insurance Rules and Regulations, which enabled government insurance of first-lien home mortgages under Title II of the National Housing Act of 1934.

FHA’s underwriting manual was used to implement the Title II requirement that insured mortgage loans be fully amortizing with "periodic payments by the mortgagor not in excess of his reasonable ability to pay."

FHA and the Mutual Mortgage Insurance Fund had been created by the National Housing Act only 5 months earlier.

FHA+ is published monthly by Gate House Strategies, a Washington, DC area-based advisory firm focused within the financial services, mortgage lending and servicing, community development, and public housing sectors. Contact us at FHAplus@gatehousedc.com