This Issue Includes:

- Think Piece: Michael Marshall on how innovation in modular, manufactured, 3D-printed, and AI-driven construction could lower costs and reshape housing supply.

- Three Questions: Steve Irwin on the reverse mortgage market — demographic demand, investor appetite, underwriting, and technology standardization.

- Inside Voices: Government shutdown risks, potential housing emergency actions, FHA waterfall updates, and CWCOT program developments.

- Gate House Index: Home price and square-foot trends, affordability shifts, mortgage debt growth, and rising home equity — especially among seniors.

THINK PIECE

Innovation in American Home Construction Will Soon Meaningfully Alter Housing in America

by Michael Marshall

The American economy continues to be at the top of the world when it comes to innovation, leading nearly every era of large productivity gains over the past century – the Second Industrial Revolution, the post-WWII boom, the Digital/Dot-Com transformation, the biotechnology/genomics breakthroughs, and, currently, the age of artificial intelligence.

In the housing industry, an arguably staid, old-fashioned market anchored in long-running preferences, conventions, and government regulations, methods of production and building materials nevertheless continue to evolve, improving the quality of new homes and delivering value to homebuyers even though the nominal cost has risen over time.

As discussed in FHA+ back in July, our market is short on supply over the next decade even net of older Gen X and Baby Boomer effects. Builders are responding of late to the supply constraints and affordable demand, producing homes that are slightly smaller and/or with fewer amenities. [1] We argued there are solutions that can help right-size supply and demand in the affordable sector, not least of which is regulatory relief, but concurrent with that is innovation in home construction.

The U.S. Department of Housing and Urban Development (HUD) and the Federal Housing Administration (FHA) hosted its fifth annual Innovative Housing Showcase on the National Mall last month in an effort to promote innovative home construction techniques.

The showcase featured full-scale models of manufactured, modular, and 3D-printed homes, offering tangible examples of how modern construction methods can deliver quality, affordable housing. [2]

By insuring mortgages for non-traditional housing types—such as manufactured homes—FHA helps reduce risk for lenders and support the scaling of new construction techniques. FHA is also exploring updates to its underwriting standards to better accommodate homes built with emerging technologies, and bipartisan legislation has been introduced in the Senate that would ease existing manufactured housing regulations and support modular home construction.

Innovation over the next 5-10 years provides an opportunity to deliver substantial efficiencies, bring down the cost of new construction, and allow homebuilders to increase production of new units at affordable price points that can make a large contribution to solving today’s shortage in affordable housing supply.

The math on new home construction makes it difficult for builders to earn a profit on affordable housing in many markets given the substantial fixed costs, including regulatory costs. Still, despite the refrain “they don’t make ‘em like they used to” the American home of today is more resilient than it was in the recent past. On average, low- and moderate-income Americans are living in higher quality homes. [3]

But based on the widespread interest in solving the affordable housing supply problem, a wave has the potential to break on innovative construction. Indeed, our firm has been working with several of these trailblazers in recent years.

Estimates vary, but U.S. investment in housing construction technology has been in the tens of billions of dollars over the past 5 years. Efforts include AI for design & project management, robotics and automation (e.g., on-site microfactories), 3-D printing, modular/foldable housing systems, and more.

Given that level of investment, the price per square foot of a median priced home could decline substantially over the next 10 years with the help of alternative construction methods.

Depending on the region, the price of site-built homes ranges from $125-300 per square foot, modular homes between $80-$160 per square foot, and manufactured homes between $70-90 per square foot excluding land. 3-D printed homes are ranging between $80-$150 per square foot, but that’s without finishings. Though the costs of alternative homebuilding technologies provide an advantage to site-built housing, other barriers must be overcome, and market share remains low.

A McKinsey study estimates that modular and pre-fab homes can drive costs lower by up to 20%, [4] and the Harvard Joint Center for Housing Studies (JCHS) estimates that housing construction time can be cut in half, [5] referring to Terner Center research that also estimates housing costs can be reduced by 10-20%. [6] Although 3-D print home manufacturers who reach scale are claiming much lower costs, as low as $36 without finishings, the reality may be closer to the McKinsey/Harvard estimates.

Regardless, the market is responding to the current and growing need. The investments underway in construction design will ultimately bear fruit, notwithstanding frictions that make any change more difficult than just about every other sector. Nevertheless, the ingenuity and innovative character of the American economy is at hand.

For more information, contact: FHAplus@gatehousedc.com.

[1] The median size of a new home has fallen for the past decade after peaking at nearly 2,500 square feet in 2015. The average new home size grew steadily from 1,400-1,500 square feet in the 1970’s to 2,350 square feet in the 2010s before falling to 2,250 in first half of the current decade.

[2] The NAHB also hosts an annual International Builders’ Show (IBS), bringing together builders, remodelers, developers, suppliers, and manufacturers to showcase the latest home building products and technologies.

[3] 100 years ago: homes often lacked indoor electricity, plumbing, a/c, and central heating.

50 years ago: many homes had lead paint, asbestos, poor insulation; existing MH was not built to last.

20 years ago: affordable housing stock often included aging postwar multifamily units.

Steve Irwin on the state of the reverse mortgage industry.

THREE QUESTIONS

Steve Irwin is President of the National Reverse Mortgage Lenders Association (NRMLA). The organization advocates on the federal and state levels for its more than 250 company members and their employees, and the senior homeowners they serve. In this month’s “3 Questions,” Steve talks about the opportunities and challenges presented to lenders who originate and service reverse mortgages.

Question: What would you say to a lender who might be interested in getting into the reverse mortgage business?

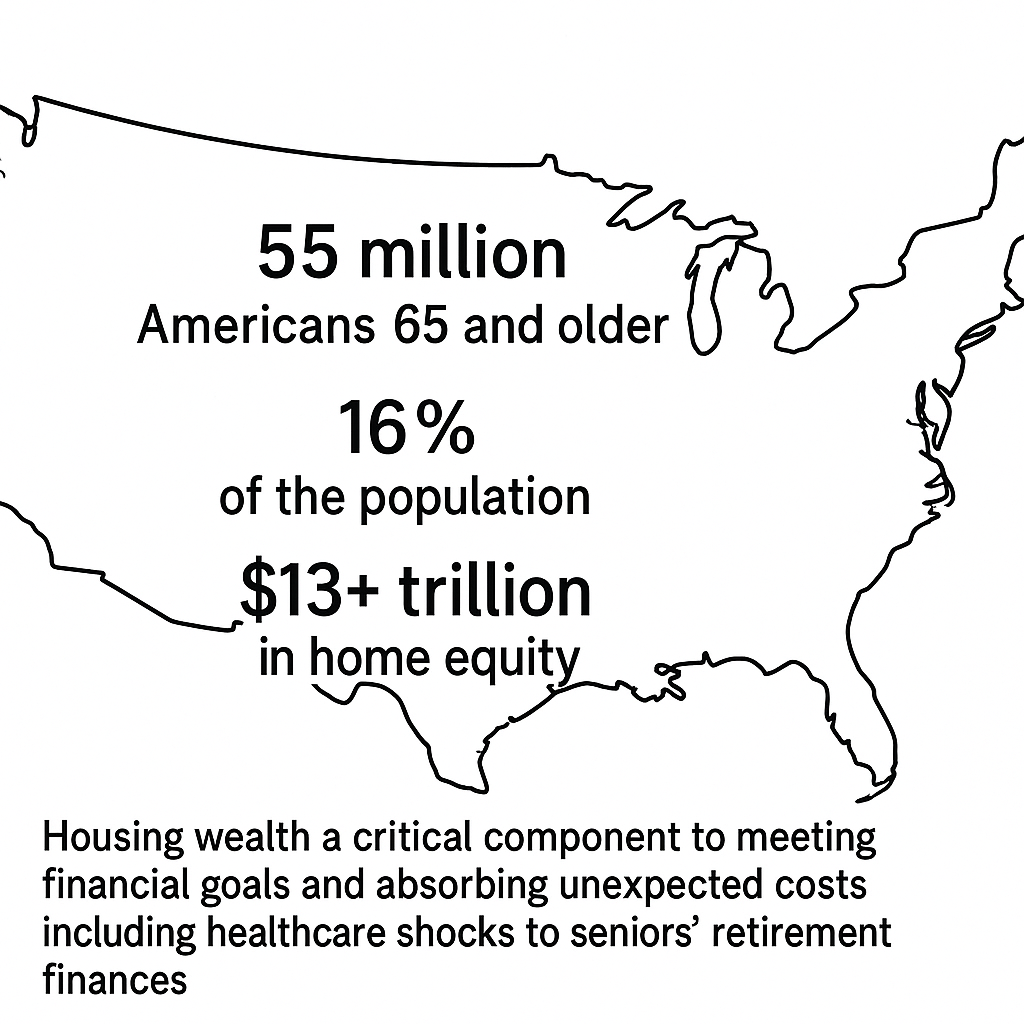

Irwin: I’d first tell them reverse mortgages are an increasingly important product to have in your lending arsenal and portfolio retention strategy. As the country continues to age, it simply makes sense for a lender to help meet the needs of its older customers. There are some 55 million people in the U.S. who are 65 years or older, representing over 16 percent of the population. These older homeowners have more than $13 trillion in home equity. The need to monetize that equity as part of a retirement plan is becoming ever more evident. Access to housing wealth is a critical component of addressing retirees’ top financial concerns: the risks of living longer, of maintaining their current lifestyle and the ability to absorb unexpected healthcare shocks to their retirement finances. The monetization of that equity mitigates a lot of the retirement financial risks.

On the back end of the reverse mortgage business, the market is quite robust. The investor base is ever-increasing and expanding, both for the FHA-insured product and private-label products. And there are an increasing number of inquiries from warehouse lenders who are looking to get into the space.

Question: In respect to industry standards, there are some things still to iron out, correct?

Irwin: Yes, there are still some challenges with the point-of-sale tech stacks as larger forward mortgage lenders look to enter the space and integrate products. But we are seeing huge strides being made in this area. NRMLA has been very engaged with the Reverse Mortgage Development Work Group of MISMO (Mortgage Industry Standards Maintenance Organization). We’ve just finished phase one of incorporating reverse mortgage elements into the MISMO reference model. That covered the origination phase of the MISMO standards. Now we're moving on to the secondary markets phase, after which we’ll deal with the servicing phase. All this effort reflects the fact that definitionally there are certain differences between reverse mortgage lending and forward mortgage lending. That can create some bumps in the road, which we’re smoothing out. For instance, there have been challenges with portability, moving data and portfolios from lender to lender. As all that data gets standardized, that and other issues will go away.

Question: On the consumer side, what kind of underwriting does this business demand?

Irwin: Well, it’s a distinct set of origination calculations. Reverse mortgages are non-recourse, collateral-based loans. The only thing repaying the lender is that property. There’s no other recourse. The borrower will not owe more than the property’s value at the end of the loan. So therefore, you've got to get it right up front.

And not only do you want to ensure a fair and accurate valuation at time of origination you need solid underwriting that carefully reviews a borrower’s expenses, cash flow and liquid assets. You want to make sure your clients have enough residual income to pay for utilities, food, medical expenses, taxes and property insurance after the close of the loan.

All these details make it a more high-touch business on the consumer side. Our members find that it's been consistently well worth it. And as both macroeconomic forces turn more favorable and the demographic trends continue on pace, we believe the demand for reverse mortgages will grow even further.

INSIDE VOICES

What we’re hearing around Washington and the industry

Shutdown: The federal government shutdown, which is centered on a disagreement over keeping pandemic-level Obamacare tax credits, continues with little indication as to how it will be resolved. The Senate is expected to vote on the House version of a Continuing Resolution this evening, which would fund the government through November 21st. How long this closure lasts remains unclear, but the need to scope for risks and ramifications is immediate. Lenders should prepare for the real possibility of disruption across housing and mortgage operations: delays at FHA, potential impacts at Ginnie Mae and VA, and complications with flood insurance. The GSEs should be less affected by the shutdown.

Housing Emergency: With the potential for a national housing emergency announcement, the U.S. housing market could see dramatic shifts. Federal land use policies, GSE and FHA program tweaks, changes to closing costs, and reimagined zoning requirements at the local level are all on the table. This broad spectrum of possibilities could provide a much-needed spark for revitalizing supply, especially as interest rates dip, giving a boost to affordability. The intersection of these efforts could lead to quicker, more efficient housing delivery, but how far the reforms will go and how they’ll be implemented remains to be seen.

FHA Waterfall Rollout: Mortgagee Letter 2025-21 clarifies FHA’s waterfall and includes a handful of revisions to reflect industry feedback and align with President Trump’s executive order on use of public funds.

FHA CWCOT: FHA is working on recent feedback from the industry related to its CWCOT program. There is an ongoing dialogue with stakeholders. Clear communication will be vital to navigate any forthcoming changes.

THE GATE HOUSE INDEX

The Gate House Index and analysis is designed to provide insight into the status of FHA’s business at a moment in time and over a period of time, as well as other pertinent data points we’re following.

This month, we look at important figures related to home pricing that is inviting innovation and home equity figures that present opportunity to the reverse mortgage market.

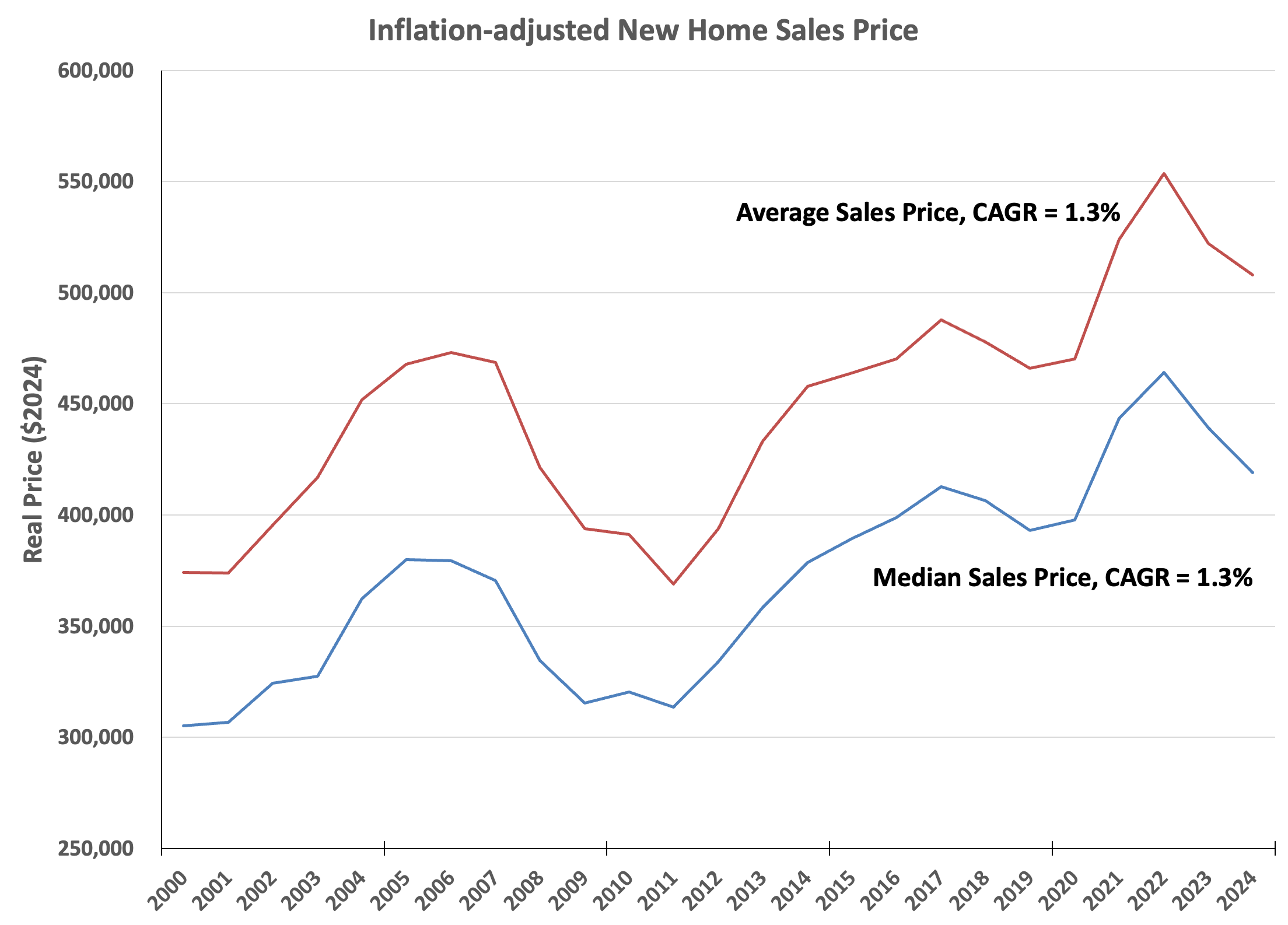

Even after inflation, we can see that home prices continue to trend up, though moderating after the mortgage rate increases in 2022.

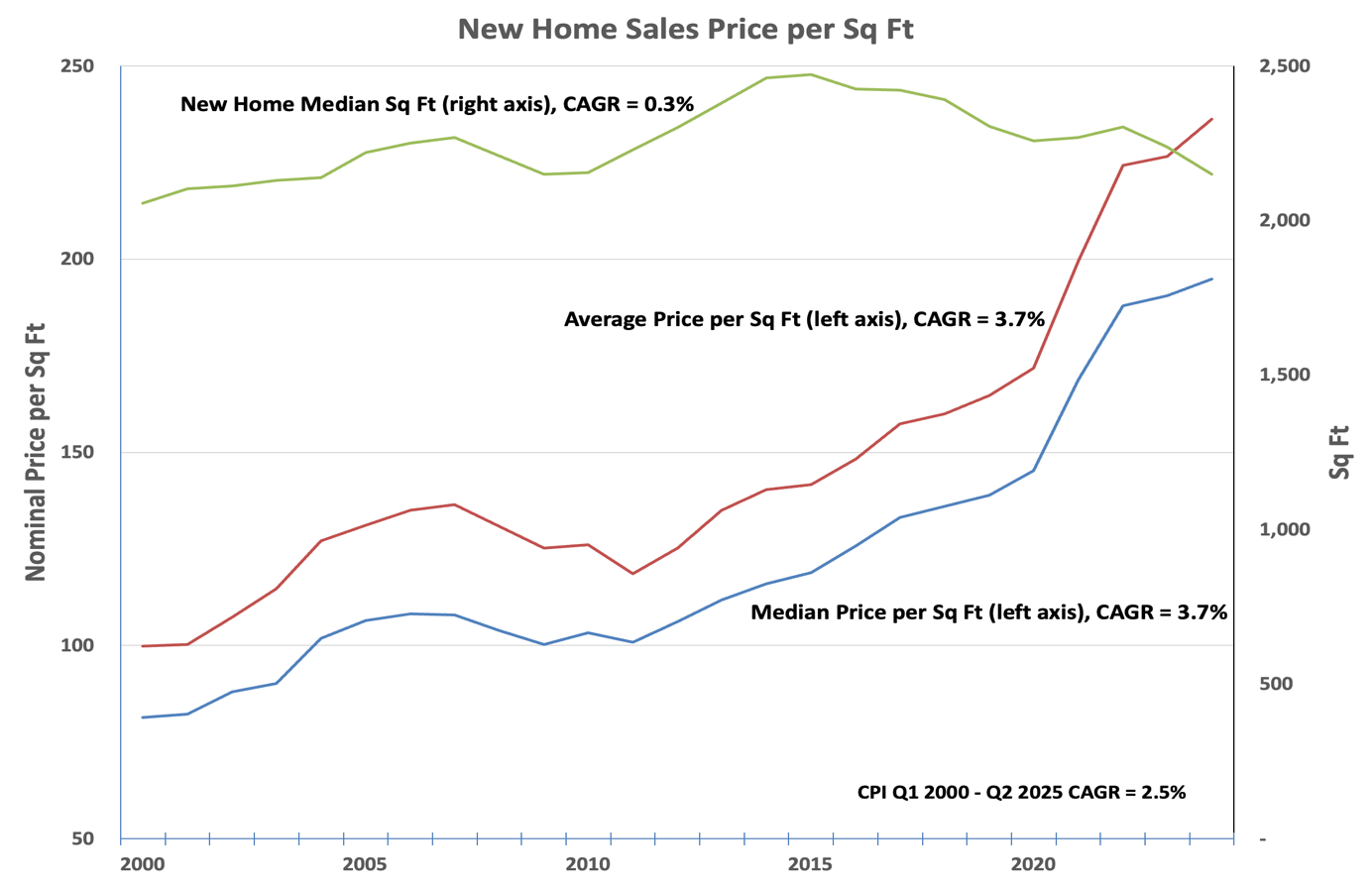

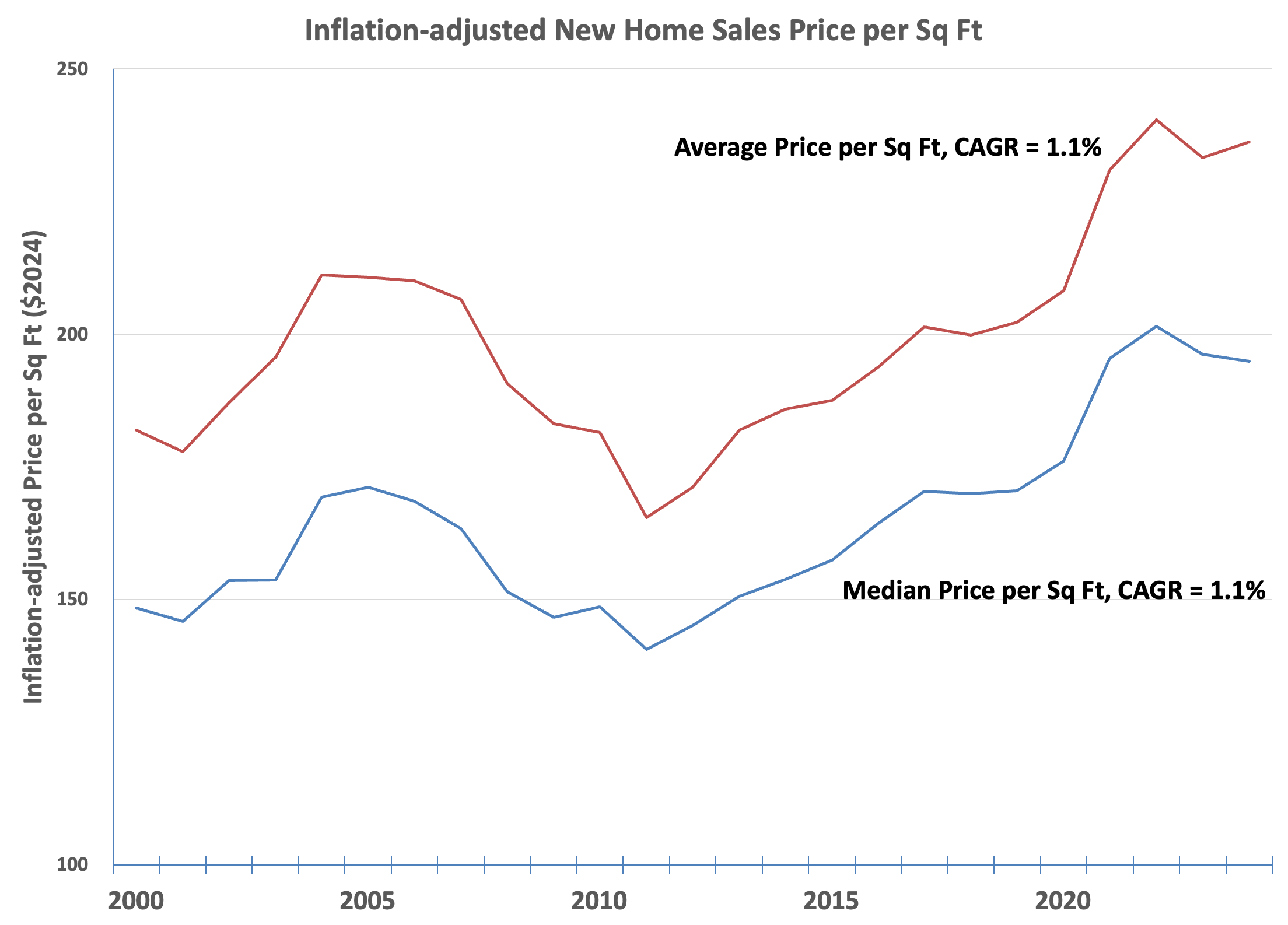

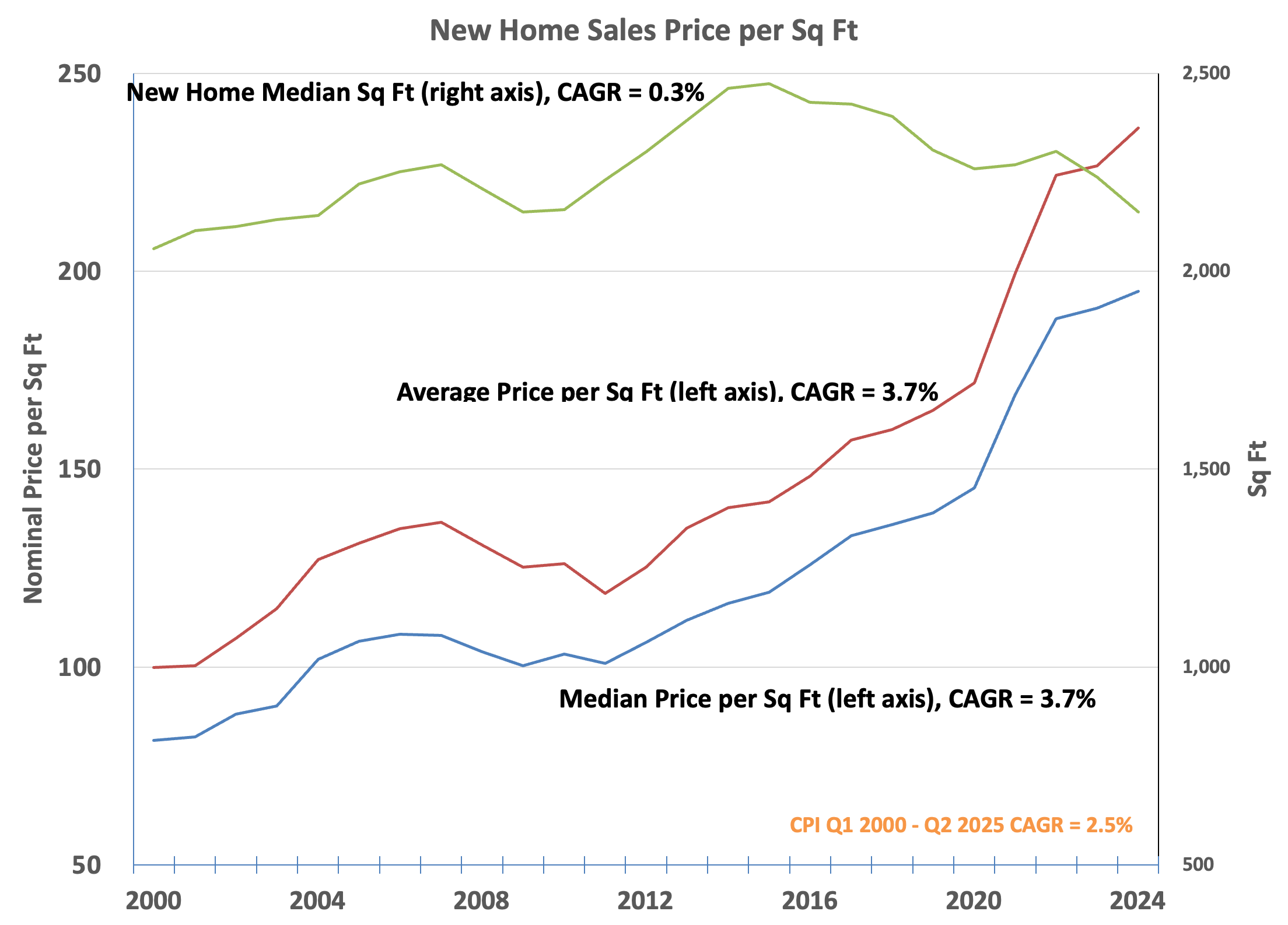

The inflation adjusted price per square foot has continued to trend up as builders have reduced the size of new homes in recent years:

Recently, median new home sales prices and price per square foot have come down slightly (3%, 2022-2024).

Although home prices declined 3% between 2022 and 2024, median square footage declined further – 7% between 2022 and 2024 – and nominal price per square foot has continued an uninterrupted rise. New home price per square foot has risen every year between 2011 and 2024 while square footage in newly built homes peaked in 2015.

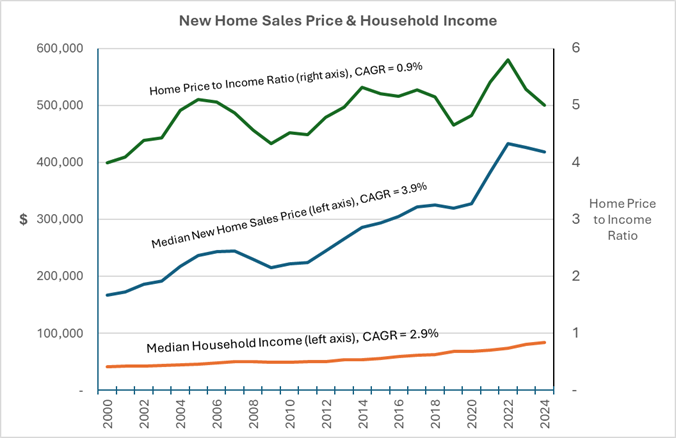

And the overall cost of housing has trended up relative to income, but declined between 2022 and 2024 as incomes rose while home prices fell:

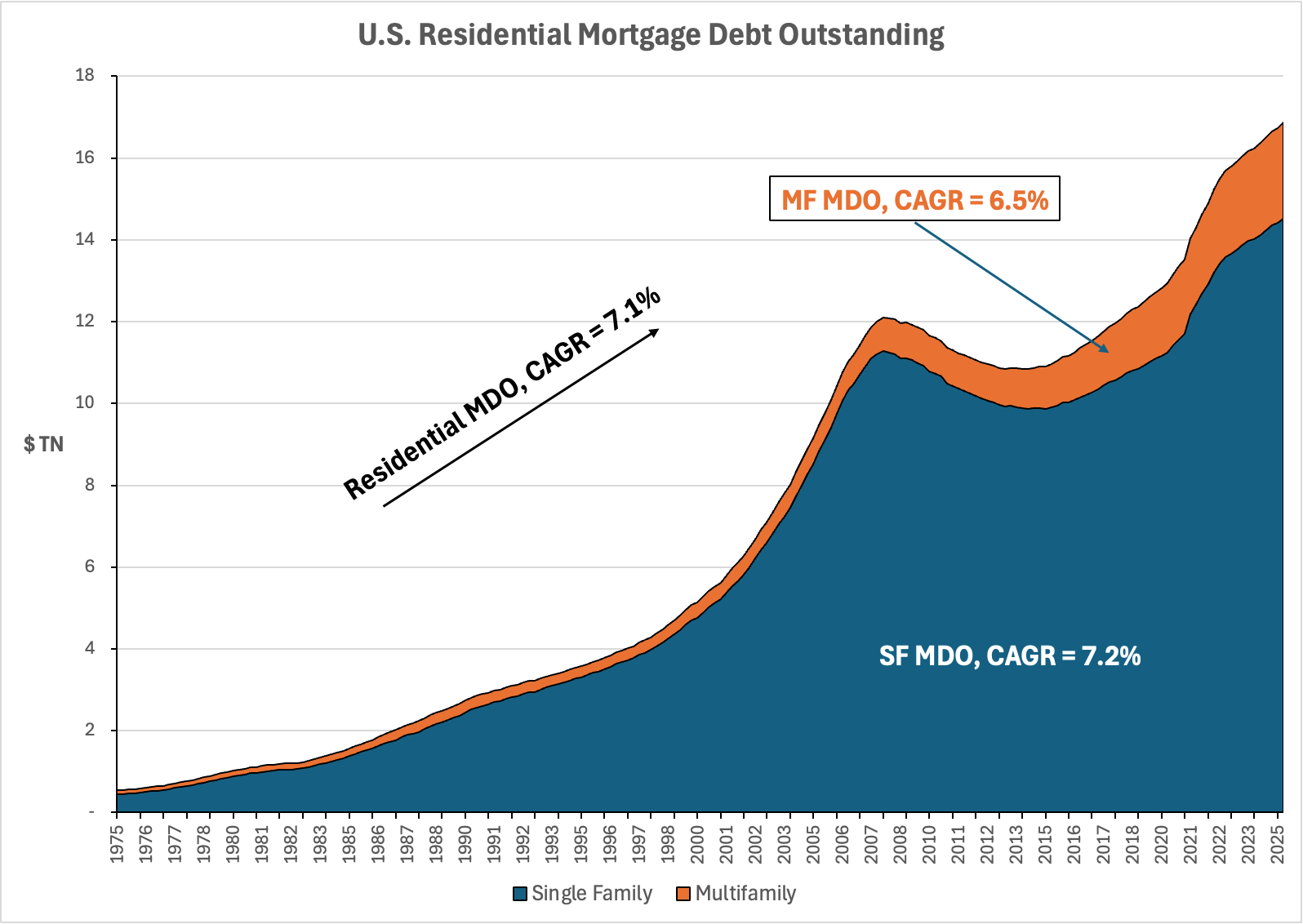

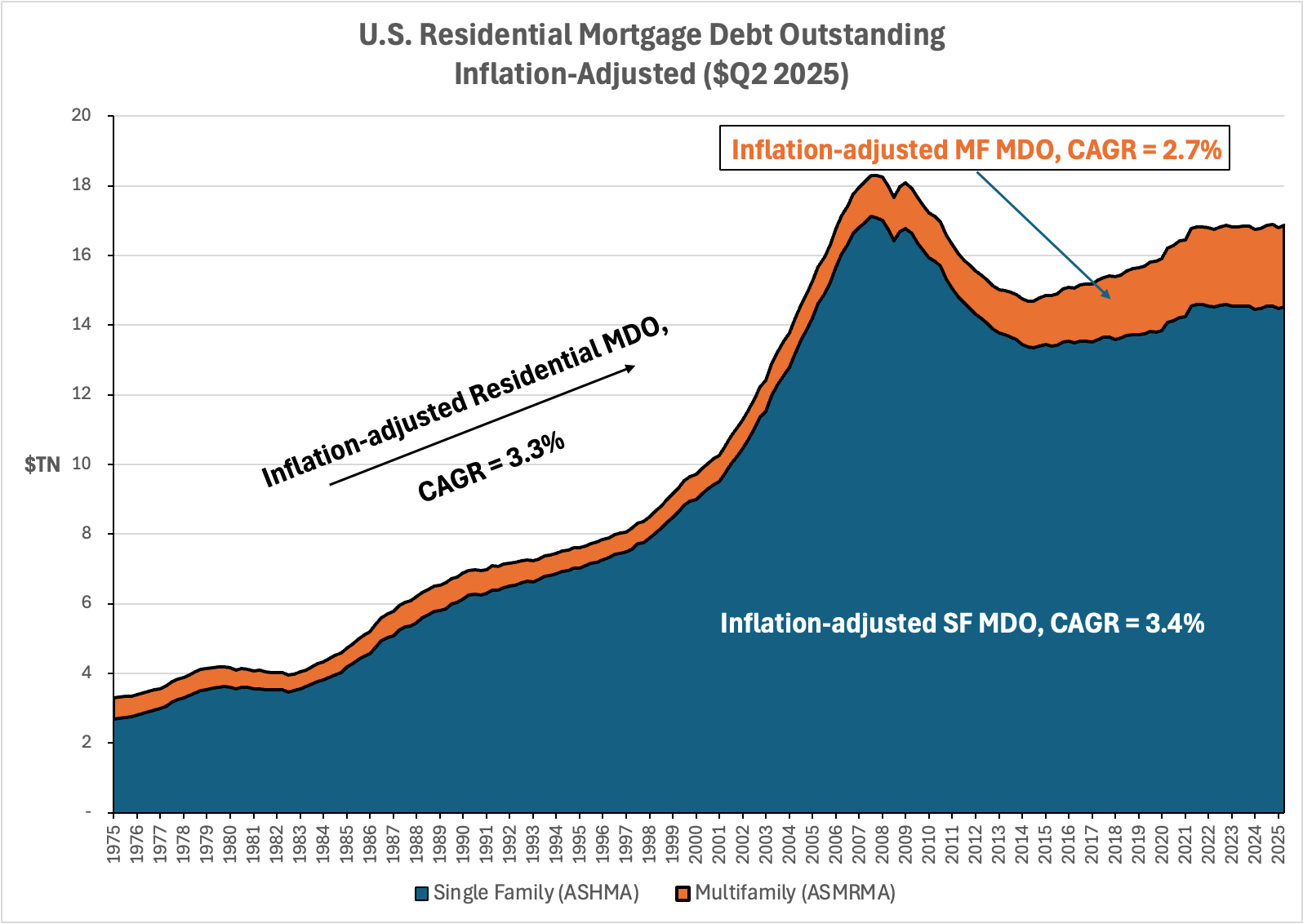

Meanwhile, mortgage debt outstanding (MDO) has been growing at 2x inflation as home prices have risen:

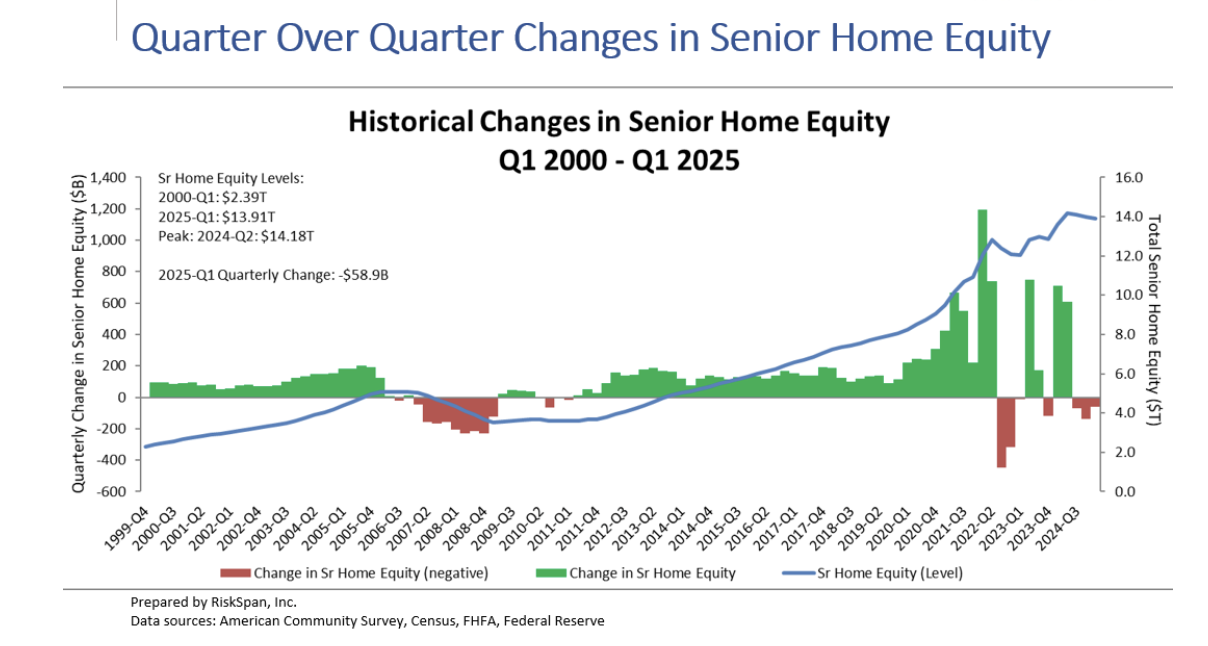

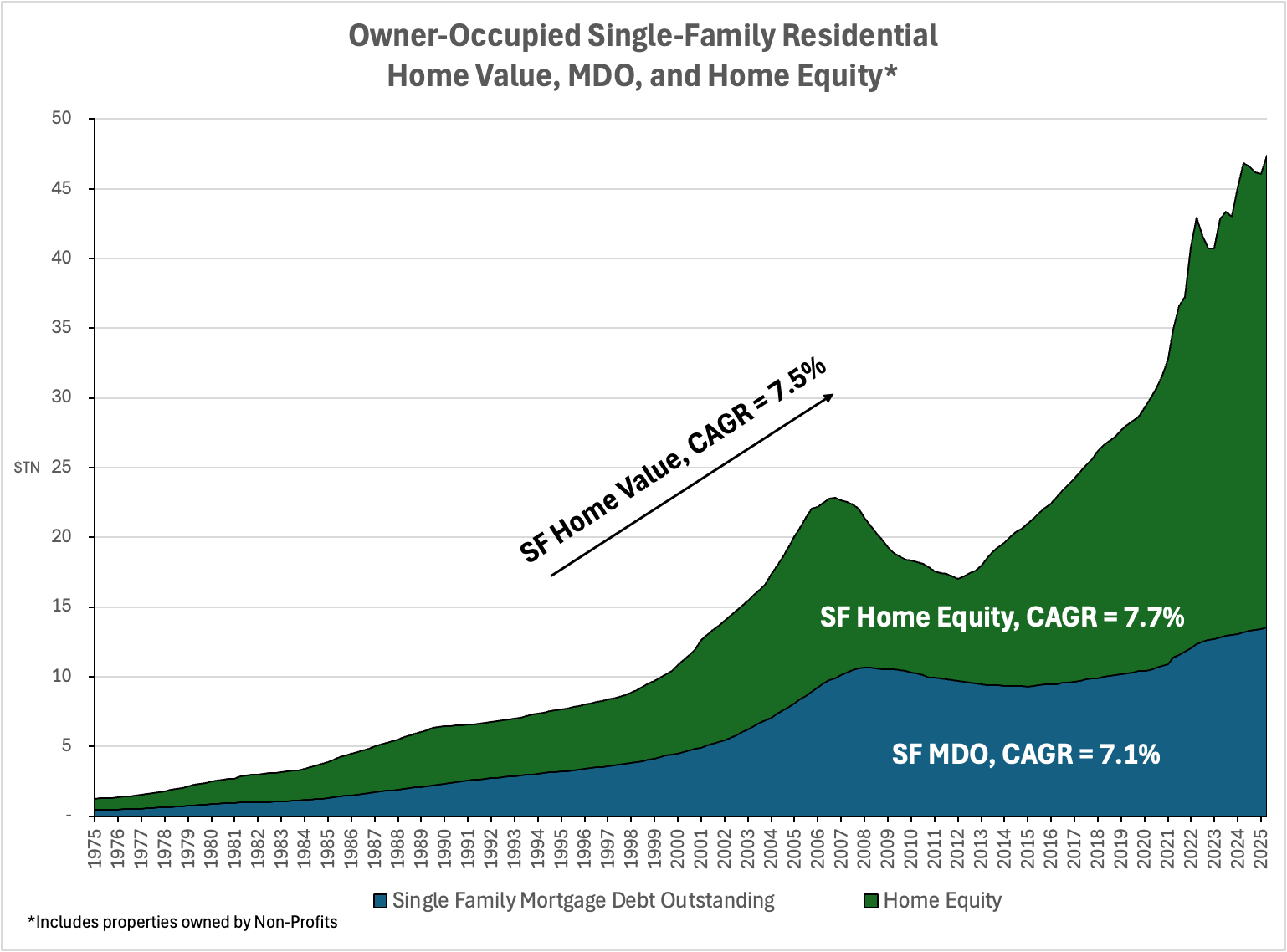

And home equity has soared:

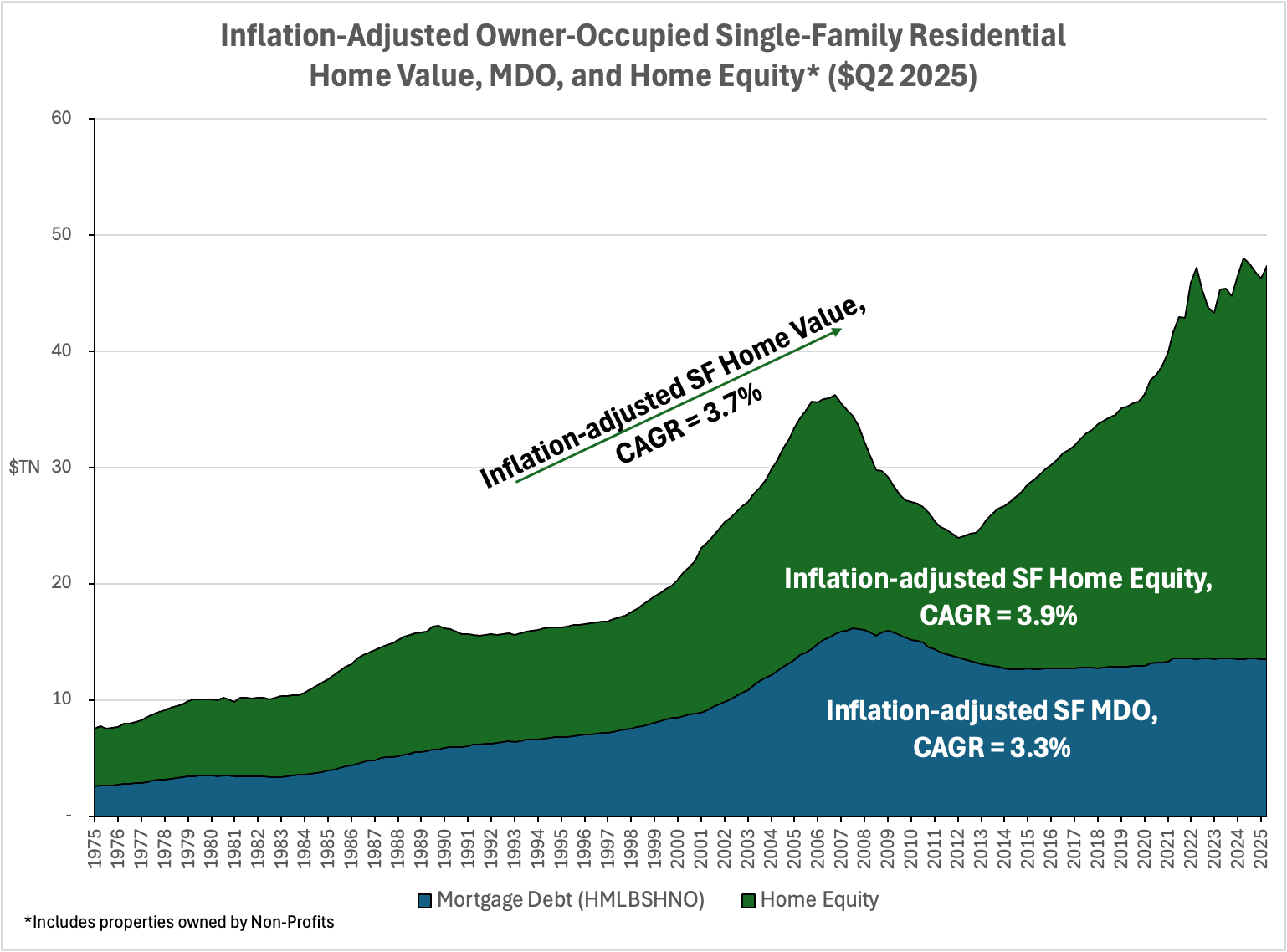

With seniors holding equity of nearly $14 trillion:

This Month In History

In October 1660, the English Restoration Parliament—convened after Charles II’s return to the throne—passed the Tenures Abolition Act (12 Charles II c.24), and the King assented, ending England’s feudal land tenures and dues. Two years later, Parliament enacted the Hearth Tax (14 Charles II c.10), a levy on fireplaces that used housing features as a proxy for household wealth. This shift marked the transition from medieval, relationship-based dues to a more modern, standardized system of property taxation.

FHA+ is published monthly by Gate House Strategies, a Washington, DC area-based advisory firm focused within the financial services, mortgage lending and servicing, community development, and public housing sectors. Contact us at FHAplus@gatehousedc.com