This Issue Includes:

- Think Piece: Earl Randall and Hunter Kurtz on HUD’s long-term role in disaster recovery, the evolution of CDBG-DR, and efforts to make the program permanent.

- Three Questions: Stockton Williams on the bipartisan momentum behind the ROAD to Housing Act and the critical partnership between state HFAs, lenders, and HUD.

- Inside Voices: ROAD Act progress, condo market bottlenecks, rising insurance costs, HUD language policy changes, and renewed GSE IPO speculation.

- Gate House Index: Disaster recovery appropriations trends, rising insurance premiums, and the growing role of state housing finance agencies in homeownership and rental production.

THINK PIECE

HUD’s Role in Natural Disaster Recovery

by Earl Randall and Hunter Kurtz

September sits at the center of peak Atlantic hurricane season, according to NOAA’s National Hurricane Center. And this year, the tropics are following the same pattern of unpredictability that forecasters label as an unusually active one. During this time, we often become familiar again with the stark media images of the federal government responding when a catastrophe hits. While the Federal Emergency Management Agency (FEMA) is widely recognized for its role in natural disaster response during hurricane season, the U.S. Department of Housing and Urban Development (HUD) performs crucial though perhaps less publicized work to support the rebuilding of affected communities. While FEMA’s efforts to address emergency needs may dominate news coverage of hurricanes and other natural disasters, HUD focuses on the less visible processes around longer-term housing needs, infrastructure and economic development.

A textbook example is 2005’s Hurricane Katrina. The positive impact of the work by HUD and its partners in New Orleans and on the Gulf Coast has required two decades of sustained effort. But imagine that area in the immediate aftermath of the storm.

Once New Orleans neighborhoods were drained of devastating flood, lifeless streets were covered in dried toxic sludge. Thousands of people were displaced. Businesses were destroyed, infrastructure was obliterated. Federal, state and local governments tried to manage people’s expectations of what recovery would look like. Amid the grim reality, with so many people experiencing ongoing emergencies, government officials committed to a recovery effort that would last for many years – and it has taken more than two decades for the Crescent City to fully recover.

Long-term progress requires that key first steps be taken at the outset. Perhaps the single most important action by HUD following Katrina was the activation of the Community Development Block Grant–Disaster Recovery (CDBG-DR) funding. CDBG funding had been used prior to 2005, to address recovery efforts for the Northridge Earthquake in California, the Oklahoma City bombing and the September 11th terror attacks.

But with the massive scale of Katrina’s devastation, the congressionally appropriated CDBG-DR program had to be large enough to cover catastrophic damage that impacted communities in Louisiana, Texas, Mississippi, Alabama and Florida.

Since 2005, CDBG-DR has become HUD’s primary disaster recovery program. HUD program staff leverages the funding to help communities rebuild in the months and years following a disaster. In the 20 years since Hurricane Katrina, Congress has appropriated more than $107 billion to address the disaster recovery needs of 47 active grantees (23 states, 15 counties, eight cities and one territory) that faced hurricanes, tornadoes, typhoons, tsunamis, floods, fires, drought, freezes, and a pandemic. [1]

Successful long-term recovery efforts largely hinge on the congressional appropriations needed to address presidentially declared disasters. That’s a process that can take time. And time is the one thing that survivors and impacted communities cannot afford to lose. Efforts continue in Washington to craft legislation designed to make CDBG-DR program permanent. That could lead to a significant reduction in the time it takes to allocate recovery dollars. Closing the gap between a disaster event and the disbursement of long-term funding is needed to boost a community’s hopes for recovery and resilience.

For more information, contact: FHAplus@gatehousedc.com.

[1] https://www.hud.gov/sites/dfiles/CPD/documents/CDBG-DR/CDBG_DR_Grant_History_7_1_2024.pdf

THREE QUESTIONS

Stockton Williams on the ROAD to Housing Act and on state housing agencies’ partnership with mortgage lenders and the federal government.

Stockton Williams is Executive Director of the National Council of State Housing Agencies (NCSHA), a non-partisan, non-profit organization that represents and advocates for state housing finance agencies (HFAs) and their efforts to provide affordable housing for low- and moderate-income households. In this month’s “3 Questions,” Williams discusses the work NCSHA members do with HUD and the mortgage industry, and shares HFAs’ view of the Renewing Opportunity in the American Dream to Housing Act of 2025 currently moving through Congress. Also known as the ROAD to Housing Act, the bipartisan bill aims to expand and preserve housing supply, improve affordability and access, and accelerate home building.

Question: The ROAD Act is awaiting consideration by the full Senate. Are you optimistic about continued bipartisanship around housing, as the bill moves closer to possible congressional approval?

Williams: Absolutely. The fact that housing affordability is a national issue clearly has given the bill a sense of urgency. As a result, this package is truly the most substantive and wide-ranging housing bill that we have seen move through a Senate committee in an exceptionally long time. And it didn't only pass the committee on a bipartisan basis. It passed unanimously and with enthusiasm expressed by members on both sides of the aisle. It's not just one of those bills that has a few innocuous provisions that are non-controversial and not particularly impactful. Senate Banking Committee Chairman Tim Scott and Ranking Minority Member Elizabeth Warren engaged all their members, who without exception contributed at least one or two or three provisions for consideration in the committee. And instead of just giving those members a subcommittee hearing or letting their staffs draft reports that few people would read, the chairman and ranking member said, "Let's actually mold legislation. Let's put together a bill that includes these ideas.” It harkens back to a time when the Senate and House were working bodies that crafted and refined and produced legislation. It’s a significant step, something that all of us in housing are excited to help pass and then build on with other bipartisan efforts.

Question: What part of the Act is most important to state housing agencies?

Williams: There are some important components that are of particular interest. For one, there’s a provision in the bill to significantly expand the capacity of state and local governments to support home repairs and home improvements. Everyone in housing knows that adding supply is the most critical need in the market overall. Part of the solution to a supply shortage is preserving the existing stock, whether we're talking about the quality and affordability of rental apartments, or investing in the stock owned by lower-income families who, in many cases, won't be able to remain in place and be safely housed if they can't make some basic or even more extensive repairs. There really isn't a federal program that has much scale anymore. Of course, there are some existing home improvement insurance products on the shelf at FHA, such as Title 1, 203K. Those are not widely utilized. A simpler, more direct program for home repairs would make a significant impact by sustaining the existing supply of owner-occupied housing.

Another provision in the bill includes several enhancements to the long-running HOME housing block grant statute, which housing finance agencies administer at the state level in most states. These are funds that provide dollars for new construction and rehab of owner-occupied and rental units. It's the Swiss Army knife of housing programs. The ROAD Act makes some important improvements to some of the ways HOME funds can be used

Keep in mind that HFAs interact with virtually all HUD programs and regulations. The agencies have worked closely for decades with HUD under Republican and Democratic administrations. In single-family, the HFAs finance many thousands of home mortgages every year that have FHA insurance. HFAs also finance a lot of affordable rental housing developments that have FHA multifamily insurance. And most housing finance agencies also have a responsibility — that HUD delegated to them decades ago — to provide site and asset management support for HUD multifamily properties that have project-based rental assistance contracts.

Question: HFAs deal with a multitude of challenges. Construction costs, regulatory burdens, operating expenses, insufficient funding, NIMBYism, wait list management, aging stock, and of course high interest rates. As NCSHA members manage all these things, what would you say they would want mortgage lenders to consider when it comes to state housing agencies?

Williams: Well first on the homeownership side, remember there simply aren’t enough starter homes being built. That's a huge issue. And housing finance agencies across the country are starting to experiment with ways they directly support starter-home construction. It’s an interesting area in its infancy but showing promising early results.

In terms of down payment needs and low-cost financing, housing agencies have various tools they can use to access capital markets and make funds available in their state that lower-income, first-time home buyers need. It's harder when rates are higher, but that's certainly a big challenge both lenders and housing agencies are dealing with. Remember, the HFAs together are the largest source of down payment assistance in the industry. And they can provide lower-cost financing for home mortgage loans. We’re talking about 50 to 75 to 100 basis points lower, because of a housing finance agency's ability to access the tax-exempt bond market

Our members are already working with thousands of mortgage originators, depositories, IDBs, CDFIs and credit unions. Housing finance agencies in every state are partners with mortgage lenders in serving first-time buyers, especially in more rural and economically challenged communities. If a lender isn't working with their housing finance agency, they should look them up in the states where they do business or give NCSHA a call – we’d be glad to help you grow your business.

INSIDE VOICES

What we’re hearing around Washington and the industry

The Long and Winding ROAD: The Senate Banking Committee greenlit the ROAD to Housing Act — a sweeping, bipartisan package that tackles everything from zoning to financing reforms. It’s an unusually comprehensive effort with real potential, though its sheer scope could make broader passage a steep climb, and full implementation would be a years-long marathon. If some or all of it should pass, HUD and FHA would have a lot on their plate to bring its many provisions to life. Still, its momentum signals a rare moment of bipartisan alignment on housing. “This is the kind of big-tent housing bill we almost never see - ambitious, bipartisan, and brimming with ideas that could reshape the market for a generation. Now comes the hard part,” said Brian Montgomery, Chairman and Co-Founder of Gate House Strategies.

Condo Buyers? There’d Be Plenty If …: Condominiums remain a stubborn weak spot in the housing market—caught between rising costs, tighter underwriting, and outdated project approval rules that keep many units out of reach for buyers. The result: constrained supply in a segment that should be an entry point for first-time and moderate-income homeowners. Work is underway, but the question on the minds of many industry watchers remains—what will FHA and the GSEs do to finally break this logjam?

And if That Wasn’t Enough: Insurance costs are soaring—piling pressure on current homeowners and putting the dream of ownership further out of reach for future buyers. In some markets, premiums are rising faster than home prices and incomes, threatening affordability and market stability alike. The issue has landed squarely on the radar of federal policymakers, with key federal officials said to be quietly exploring ways to blunt the impact.

Watch Your Language: HUD's new policy, outlined in a memo from Deputy Secretary Andrew Hughes, designates English as the primary language for all services and operations. As a result, HUD will no longer provide translation services, in line with President Trump’s executive order and recent Justice Department guidance. The department will still meet accessibility needs for individuals with visual or hearing impairments, ensuring compliance with legal requirements while streamlining operations.

GSE IPO TBD: President Trump has put forward a big, bold vision for the future of Fannie Mae and Freddie Mac—framing their eventual IPOs as a potential record-shattering moment in U.S. market history. The pitch is headline-grabbing. But the path is tangled too with significant and unsettled policy, politics and market mechanics that will take time to sort out. One big question on the minds of Washington players who we’re hearing from: One GSE or two? Let the games begin.

THE GATE HOUSE INDEX

The Gate House Index and analysis is designed to provide insight into the status of FHA’s business at a moment in time and over a period of time, as well as other pertinent data points we’re following.

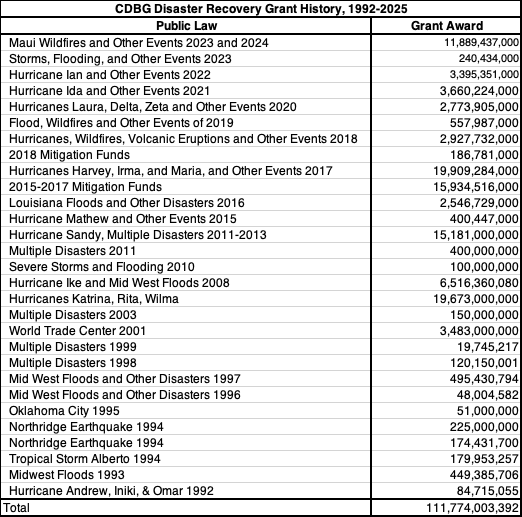

This month, we look at important figures related to disaster recovery efforts in the U.S., coinciding with the Think Piece above by Earl and Hunter. Below is a table summarizing Congressionally appropriated CDBG-DR grants since 1992 with a marked increase since Hurricane Katrina:

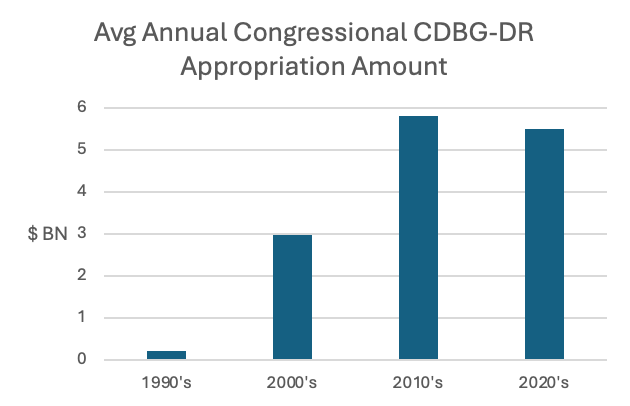

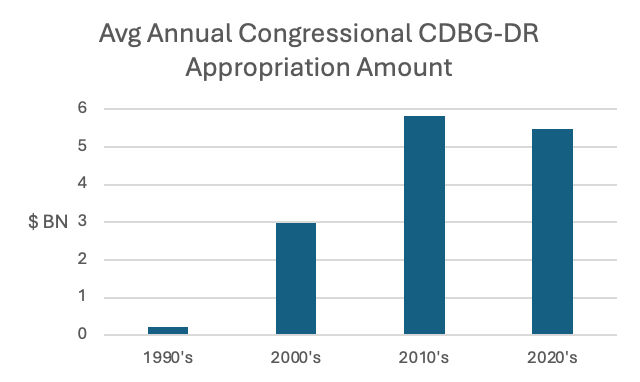

The average appropriation for CDBG-DR has risen in the most recent decades:

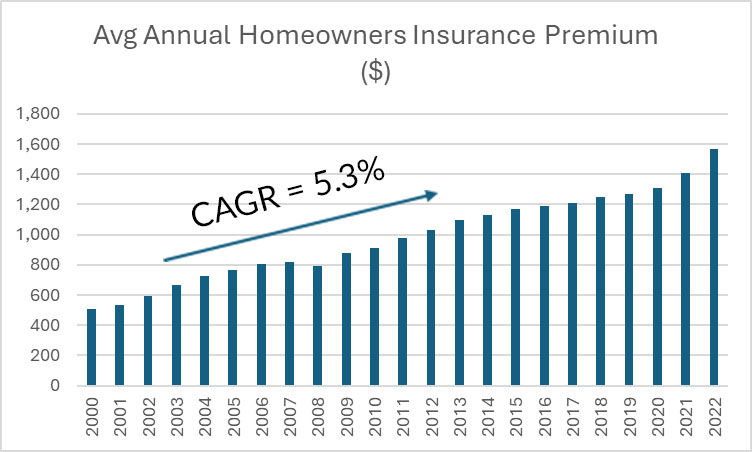

Meanwhile, homeowners Insurance premiums continue to rise faster than inflation:

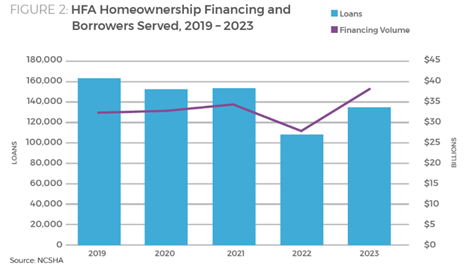

As we highlighted next to Three Questions with Stockton Williams, HFAs are providing more than $30 billion in financing for more than one hundred thousand homebuyers per year…

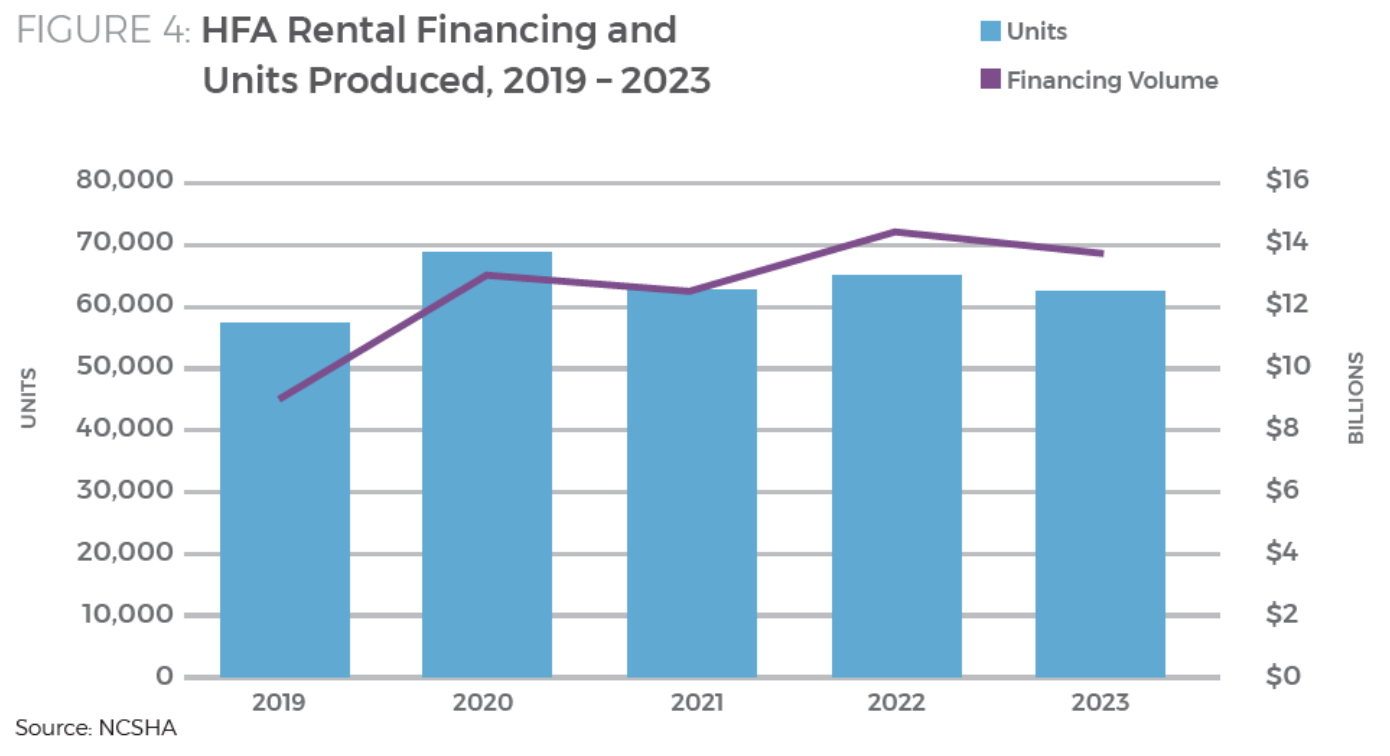

…in addition to financing for more than 50,000 rental units per year

This Month In History

The Housing and Urban Development Act of 1968 created Ginnie Mae as a separate entity within HUD to guarantee MBS backed by FHA and VA loans. The Act was part of the Great Society and also called for the construction or rehabilitation of 26 million housing units over 10 years, 6 million for low- and moderate-income families.

FHA+ is published monthly by Gate House Strategies, a Washington, DC area-based advisory firm focused within the financial services, mortgage lending and servicing, community development, and public housing sectors. Contact us at FHAplus@gatehousedc.com