This Issue Includes:

- Think Piece: Brian Montgomery on FHA rescissions, red-tape reduction, and the Administration’s push to streamline origination, servicing, and compliance standards.

- Three Questions: Michael Waldron on navigating a shifting enforcement environment and using compliance as a strategic advantage.

- Inside Voices: Credit reporting shakeups, CWCOT scrutiny, rising hazard insurance risk, escalating mortgage fraud, HUD leadership updates, and renewed GSE exit debates.

- Gate House Index: FHA market share trends, delinquency dynamics, foreclosure levels, securitization shifts, and HUD’s regulatory rollback efforts.

THINK PIECE

Rescissions Streamline FHA Lending as the Administration Seeks to Cut Red Tape

by Brian Montgomery

Recent actions by the U.S. Department of Housing and Urban Development underscore Secretary Scott Turner’s commitment to recalibrating HUD’s role in the housing finance system. The department’s sweeping overhaul of the FHA’s regulatory framework is laser-focused on efficiency, cost reduction, and alignment with industry best practices.

These changes were rolled out through a series of Mortgagee Letters and policy announcements aimed at cutting red tape and modernizing processes, and together they represent one of the most significant regulatory retrenchments in recent FHA history. Turner’s agenda and the efforts of Acting FHA Commissioner Frank Cassidy and FHA Single Family Deputy Assistant Secretary Matt Jones focus on eliminating inefficiencies and aligning with broader mortgage industry standards, and seek to make FHA-insured lending more accessible, less burdensome, and more responsive to market realities.

More recently, HUD’s June 29 announcement outlined the rescission of more than a dozen sub-regulatory policies that had shaped FHA loan origination for years. These rescissions, according to HUD, were designed to eliminate unnecessary financial and regulatory burdens that had driven up costs and impeded or delayed homeownership for borrowers — while complicating operations for lenders. For example, Mortgagee Letter 2025-18 eliminated noncritical appraisal protocols to reduce appraisal costs and align more closely with industry norms. In that same spirit, FHA also rescinded the proposed Reconsideration of Value (ROV) requirements, which had aimed to formalize the method for borrowers to challenge appraisal results. FHA concluded that the proposed ROV process would introduce operational complexity and delay, while not meaningfully improving appraisal accuracy or fairness.

Another major but less-publicized effort has been HUD’s removal of over 600 outdated or duplicative guidance documents and archived policy references. This initiative was specifically aimed at eliminating the use of incorrect or conflicting information that had begun to surface in automated systems—including AI-based tools used by lenders and servicers. By removing these legacy materials, HUD is attempting to reduce the administrative and financial burden caused by decisions based on inaccurate or obsolete policies. According to agency officials, outdated documents were increasingly being cited as authoritative by AI systems, leading to costly errors, compliance issues, and the need for time-consuming corrections.

HUD also removed the full-time employment requirement for Direct Endorsement (DE) underwriters, a change that provides greater staffing flexibility for lenders that could also ease operational bottlenecks. Other rollbacks included eliminating the mandatory collection of the Supplemental Consumer Information Form (SCIF), scrapping the Federal Flood Risk Management Standard (FFRMS) for new construction, and relaxing pre-endorsement inspection rules in disaster areas—all of which target pain points that increased transaction costs and complexity without improving loan quality.

Beyond origination reforms, HUD has also taken steps to streamline FHA loan servicing and loss mitigation practices. Mortgagee Letter 2025-12, published in April, revises the limit on how frequently a borrower may receive permanent loss mitigation assistance. It also rolls back certain language access and cash benefit provisions that HUD determined were overly burdensome or not cost-effective. These changes, HUD believes, will benefit the MMI fund while reducing servicing costs and promoting greater consistency in how servicers assist struggling homeowners.

However, not all changes have been met with universal approval. One of the more contentious actions was the modification of FHA borrower eligibility criteria through Mortgagee Letter 2025-09. Effective May 25, 2025, FHA-insured loans are limited to U.S. citizens, lawful permanent residents, and a small subset of Pacific Island citizens—excluding DACA recipients and most visa holders who had been permitted to utilize FHA since January 19, 2021, provided they met other eligibility criteria. While HUD positions this policy as a compliance and risk-management measure, critics contend it may disproportionately limit homeownership opportunities for immigrant communities and create new access barriers. What’s more, DACA status recipients and H1-B visa holders are currently permitted to remain in the US under a “legally permissible” standard and therefore are not necessarily illegal immigrants. As such, many question why they are no longer FHA eligible.

Looking ahead, HUD is also proposing adjustments to Mortgage Insurance Premiums (MIPs) to broaden cost-saving benefits across the multifamily housing sector. This move, announced on June 26, 2025, is intended to lower financing costs and stimulate the construction of more affordable rental housing—an urgent need amid an acknowledged national housing shortage.

Many in the lending community have welcomed these changes as overdue. As the housing landscape continues to evolve, it will be critical to watch the long-term effects of these actions — particularly on supply and balancing access and risks to FHA.

For more information, contact: FHAplus@gatehousedc.com.

THREE QUESTIONS

Michael Waldron on the Challenges and Opportunities in Mortgage Lending and Servicing

Michael Waldron, a founding partner of Gate House Compliance, is widely recognized in the mortgage business as a trusted advisor who helps shape executive decisions by delivering solutions that achieve business objectives while complying with investor and regulatory requirements and industry best practices. In this month’s “3 Questions,” Michael talks about how the new compliance environment creates both challenges and opportunities for lenders and servicers.

Question: In the realm of regulatory compliance, the mortgage industry currently is experiencing what might be termed a diminished enforcement environment. Does that mean practitioners can be more relaxed regarding compliance?

Waldron: It does not. While enforcement is a component of compliance, it is not, in my experience, what drives compliance. Compliance is driven by the obligation to comply with applicable laws and industry standards, to protect the customers we serve, and to mitigate risk for the platforms that we work for and represent. While some lenders and servicers are certainly taking comfort in a belief that they now won’t be subjected to the same heightened level of enforcement as before, our industry knows that compliance complexities continue and the federal and state regulatory landscape remains intact. The question of how the laws are applied and pursued is really the focus of today. In some ways, compliance is becoming more challenging, not easier, and arguably less predictable. Aside from enforcement, regulators were extremely active on other fronts such as the considerable efforts to provide a roadmap for compliance. There was a symbiotic relationship between industry and government where information was flowing in both directions. That doesn't mean there were always the right outcomes, but there were mechanisms in place that provided for some predictability within that framework.

That’s changing. We are now entering a time when the industry’s compliance platforms will need to be more self-reliant and show increased value in expanded ways.

Question: How so?

Waldron: Given the shifting landscape, we continue to urge clients and industry friends to take a broader view and focus on compliance not only with respect to enforcement but from a market differentiation and platform advancement perspective as well. Ask the questions: What opportunities does the current and projected compliance landscape allow for? How do we reallocate resources in ways that create additional market advantages and value for our customers and investors? Did the recission of a rule or the withdrawing of guidance alleviate compliance obligations or simply cloud them and create operational issues and who is analyzing that?

We are an industry that operates on cycles. In this moment of what is viewed as an enforcement lull, it would be wise to use this time to make sure you're positioning your entire platform to evolve so that you are strengthening your market position. A foundational exercise is to reassess your compliance management system in a clear-eyed way. Most CMSs were built, or based on designs from, 10 to 15 years ago. The question is, are they still positioned for success? And when I define success, it's not simply risk mitigation. I'm talking about creating the power to attract partners and get market advantages that build business because of the fundamental quality of, and confidence in, the products and services that you are delivering.

Inferior quality isn’t easily cured and is a huge drain on resources. When you create compliance while navigating curves on the road, it takes more time, and it gets far more expensive. You incur resource costs and reputational risks. You want to continually push quality into the business, by smoothing the road out and alleviating those costly turns.

Question: What’s the right way to get started with this approach?

Waldron: The obvious launching point is through evolving your CMS and creating greater efficiencies using CMS automation. That’s fine. That’s appropriate. But remember, at the end of the day, ours is a people business. It’s right to focus on technology for enhancing processes and we as an industry are beginning to embrace what other industries have already benefitted from so go for it. But in doing so, we also cannot forget the importance of attracting, from within and externally, the kind of talent and leadership who have deep industry and government experience and understand regulatory diplomacy and strategy. Those skills not only complement enhanced compliance automation, but they also inform the enhancement itself.

INSIDE VOICES

What we’re hearing around Washington and the industry

Credit Landscape: The FHFA wasted no time shaking things up—VantageScore is now officially part of the credit reporting mix, signaling a clear pivot from the bi-merge plans. While scoping is just beginning, the ripple effects are already sparking big questions across the industry for FHA, vendors, pricing, risk models, and beyond. The implications are wide—and we're only getting started. Stay tuned.

FHA Claim Without Conveyance of Title (CWCOT) Bids: We're hearing this is one to watch closely. FHA’s recent guidance on the CWCOT bidding policy may sound procedural on the surface, but we see this this as potentially impactful. The Commissioner’s Adjusted Fair Market Value (CAFMV) bidding clarity reflects FHA expectations in bidding practices, which could be costly if not followed.

Hazard Insurance: With recent catastrophic floods underscoring the stakes, hazard insurance is facing renewed scrutiny—and the risks are only rising. As natural disasters grow in frequency and intensity, lenders and homeowners are more exposed than ever. Regulators are tightening expectations around coverage verification, claim timelines, and force-placed policies to protect both collateral and borrowers, while Congress is watching the fallout closely. Underwriting and servicing teams are feeling the squeeze. Expect more policy changes on the horizon.

Mortgage Fraud Concerns: Mortgage fraud is back in the spotlight, with growing cases of income misrepresentation, synthetic identities, and inflated appraisals. What’s new—and more dangerous—is the rise of social engineering scams that trick borrowers or lenders into sharing sensitive info, enabling fraudsters to bypass traditional checks. As more loans flow through digital channels and rely on nontraditional income sources, detection is getting harder, and raising red flags on loan quality for insurers and investors.

Speaking of fraud: In a startling new twist, imposters have crashed some home purchases and closed deals—virtually. Fraudsters are posing as buyers, sellers, and even agents, hijacking transactions and vanishing with the money. It's a digital heist happening behind screens, leaving victims stunned and deals in chaos. Now, lenders are being forced to rethink security from the ground up to protect their clients and reputations.

HUD Appointments: Congratulations to David Woll on his Senate confirmation as HUD General Counsel! David has an impressive management and legal background with deep experience at HUD and DOJ. We look forward to seeing the impact of his leadership at HUD. Congrats also to Frank Cassidy on his nomination to be FHA Commissioner and former colleague Joe Gormley to be President of Ginnie Mae. When confirmed Gormley will be the first Republican-appointed President of Ginnie Mae confirmed by the Senate since 2009.

GSE Conservatorship Exit Considerations: When it comes to a GSE exit, there’s no shortage of opinions—and even more questions. From the future structure and Treasury’s payoff terms to potential MBS market splits, regulatory constraints, capital plans, and competition, the landscape is anything but clear. Democratic Senators are pressing for answers, and the debates are heating up. More recently, the FHFA’s announcement of the newly named U.S. Financial Technology platform (formerly CSS) has added yet another layer to the conversation, raising questions about the role of innovation and access in a post-conservatorship world. One thing’s certain: this ride isn’t over.

THE GATE HOUSE INDEX

The Gate House Index and analysis is designed to provide insight into the status of FHA’s business at a moment in time and over a period of time, as well as other pertinent data points we’re following.

This month, we return to key metrics of FHA’s book of business, including its share of endorsements, its SDQ rate, new 90+ delinquencies, foreclosure and bankruptcy, and the reasons for delinquencies.

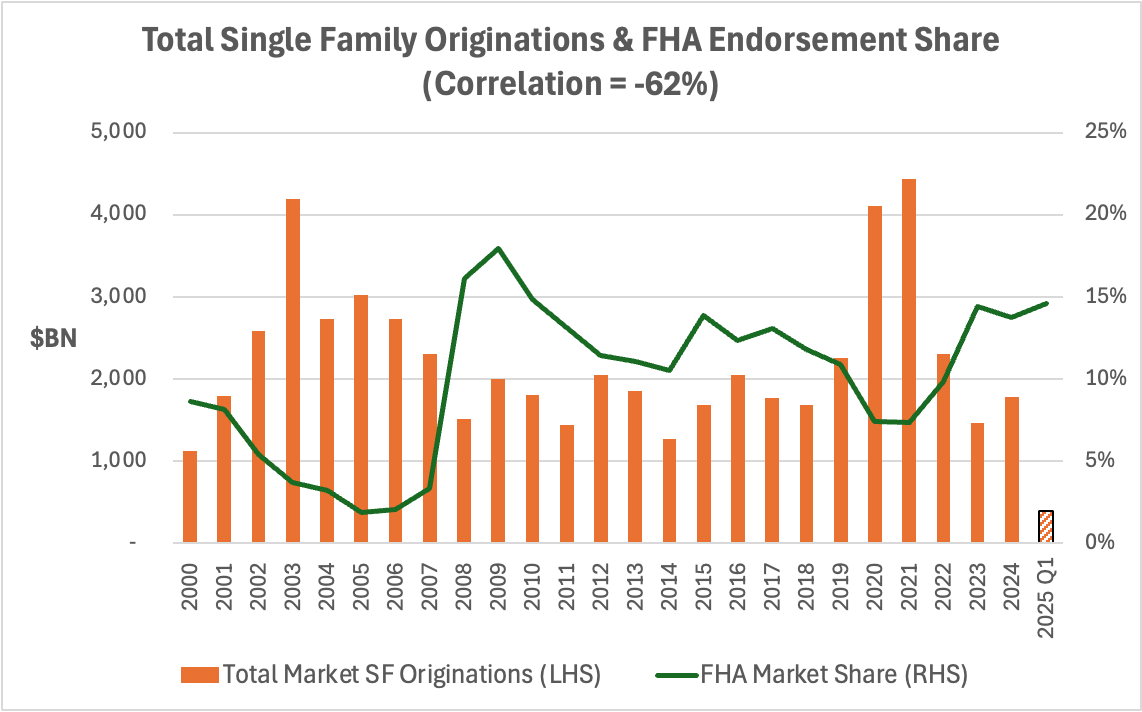

The following chart shows the countercyclical nature of FHA’s business. The green line denoting FHA’s share of total single family originations (orange bars) demonstrates that when economic conditions are more difficult and new mortgage activity declines, more borrowers tend to use FHA loans. Q1 2025 (shaded orange bar on the far right) appears to be showing a slight uptick in FHA’s share as total originations have waned:

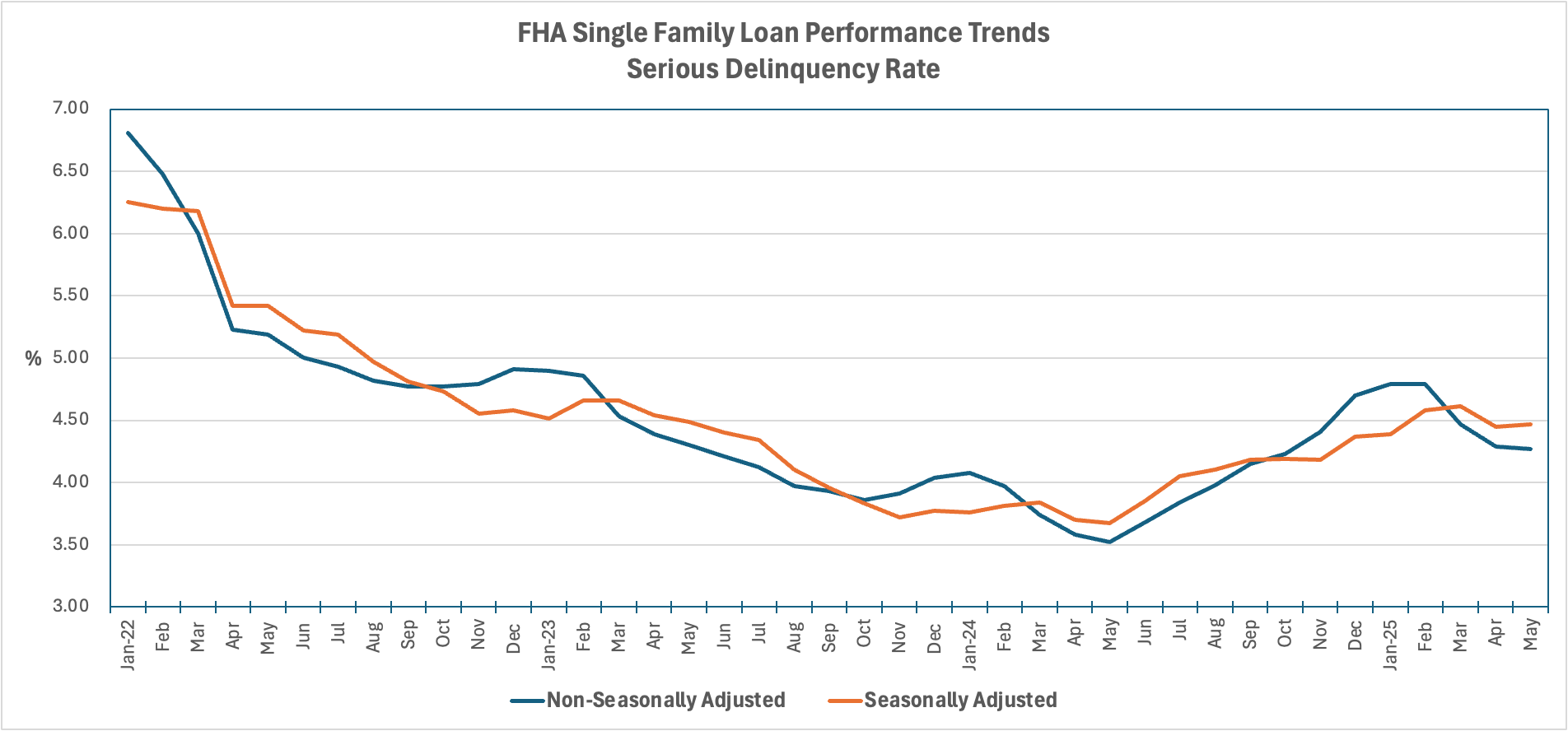

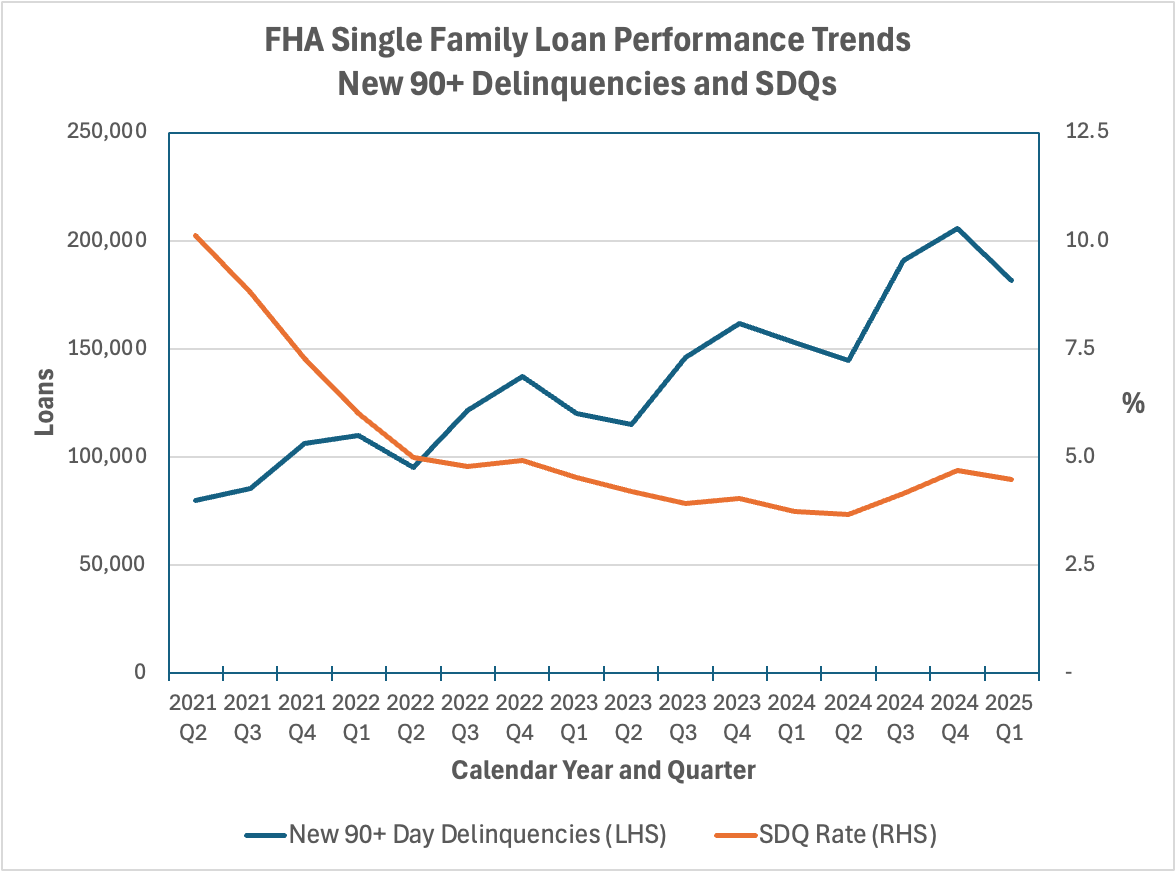

After declining significantly from pandemic highs, FHA SDQs appear to have leveled off as new 90+ delinquencies have trended upwards. We will continue to watch as the limits on permanent loss mitigation take effect October 1.

FHA loans in foreclosure and bankruptcy remain low, though we will continue to monitor as permanent loss mit options expire.

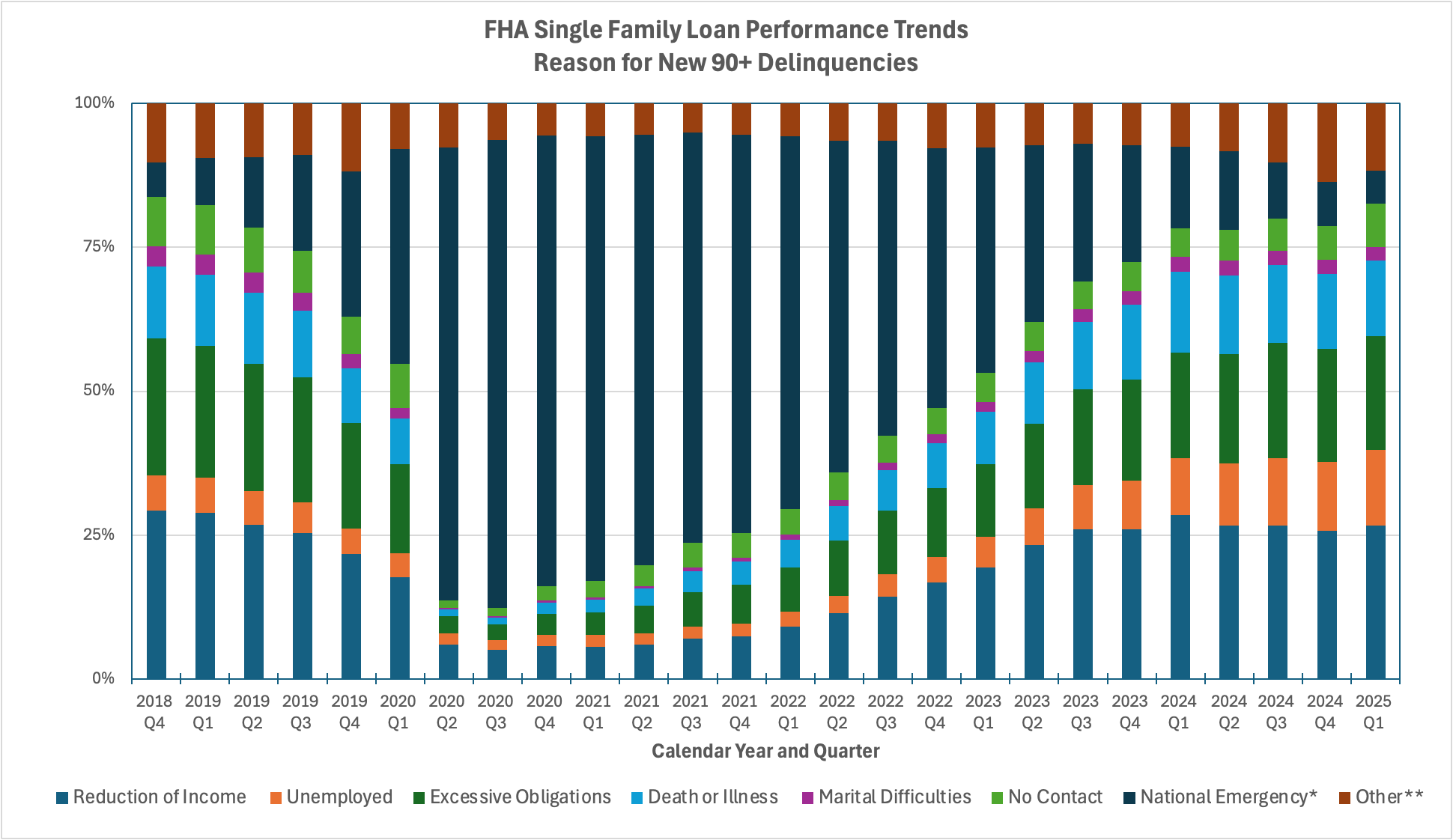

The following chart shows the share of FHA delinquencies attributable to the pandemic continued to decline through Q1 2025. The reason for serious delinquency is led by ‘Reduction of Income’ and ‘Excessive Obligations’ and, as we noted in Issue #1 of FHA+, we expected the Q4 2024 share denoted ‘No contact’ to decline and be distributed to other categories in future reports. That is indeed the case in 2025.

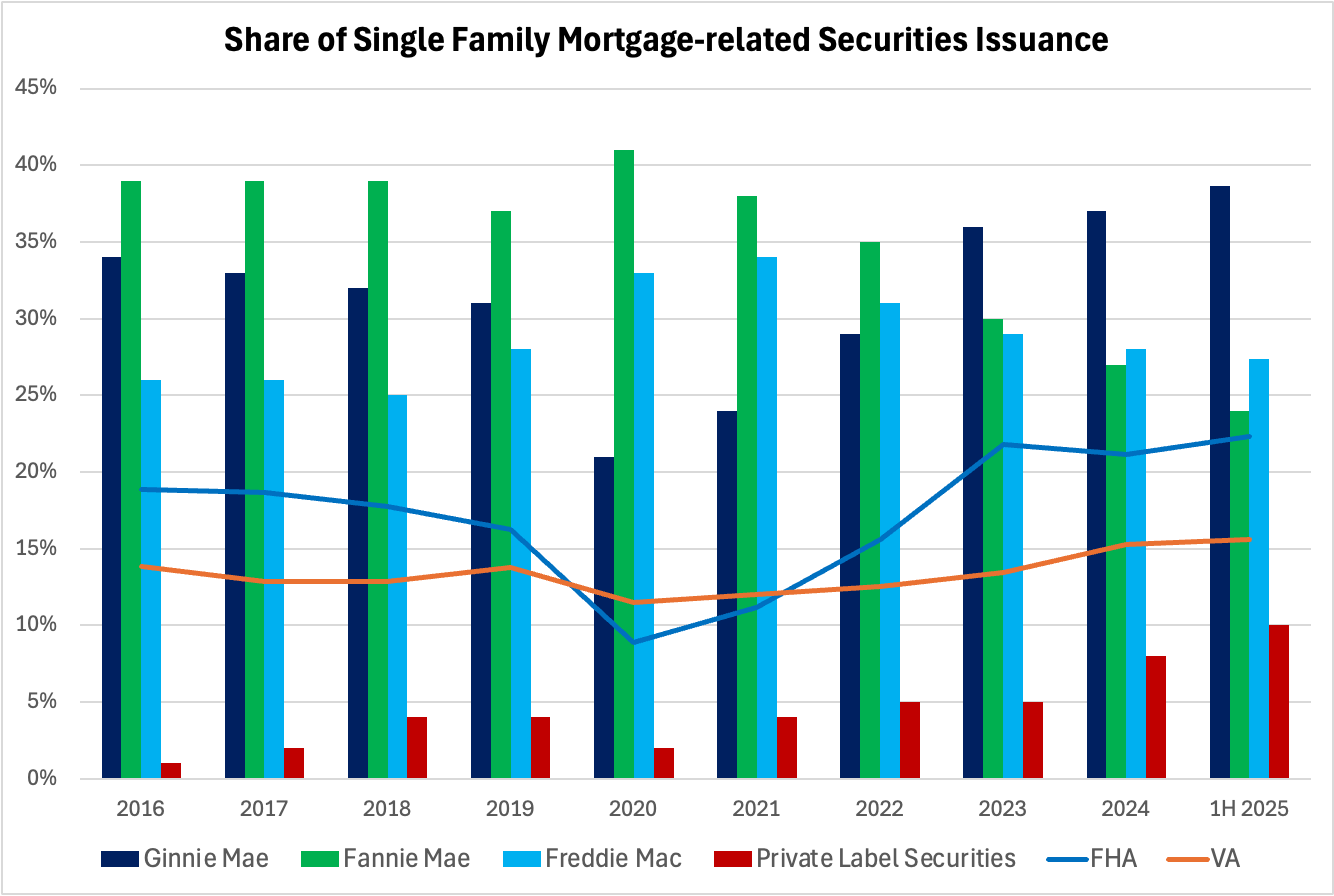

Ginnie Mae and Private Label Securities issuers have continued to grow share in the first half of 2025 (1H 2025) relative to the GSEs.

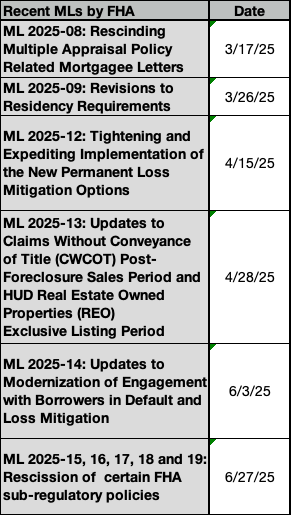

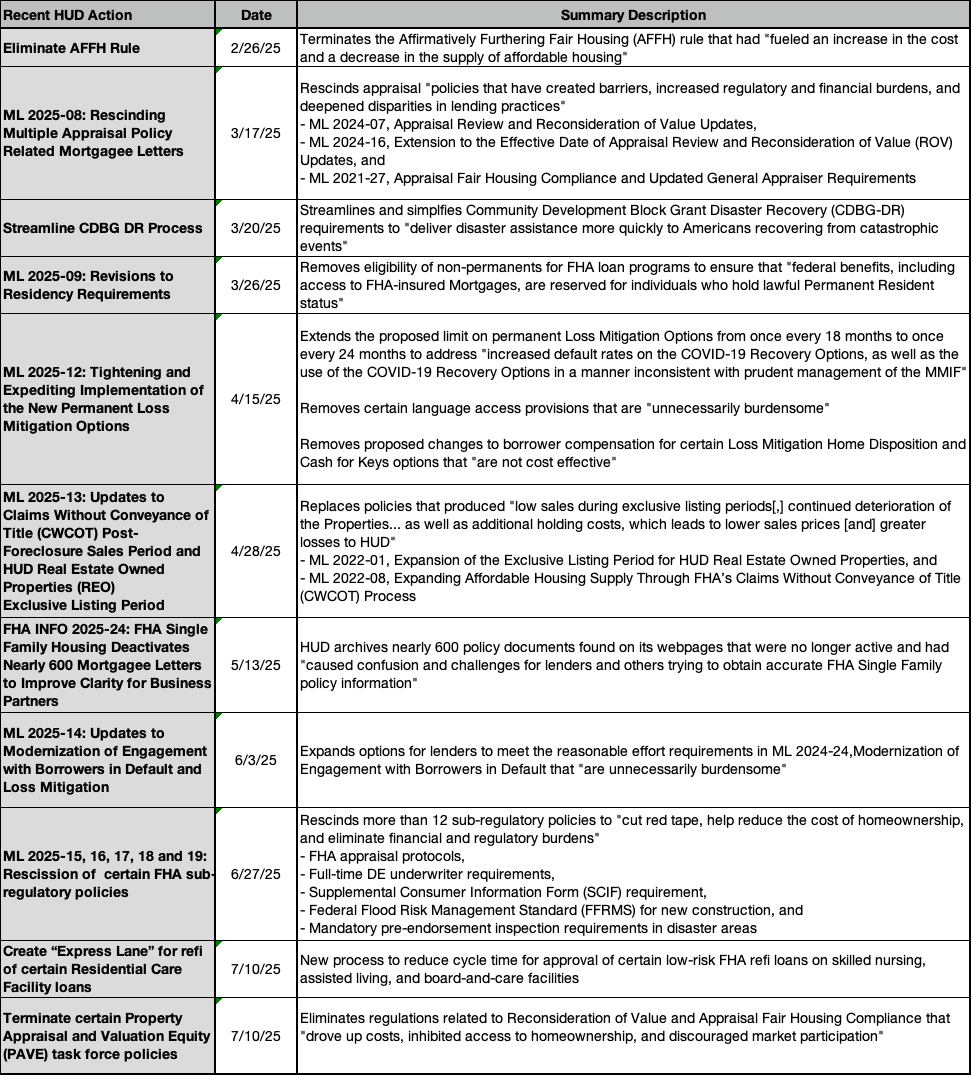

HUD has been actively pursuing its goals to reduce regulatory burden. The following is a summary of its actions this year:

This Month In History

The Housing and Urban Development Act of 1968 created Ginnie Mae as a separate entity within HUD to guarantee MBS backed by FHA and VA loans. The Act was part of the Great Society and also called for the construction or rehabilitation of 26 million housing units over 10 years, 6 million for low- and moderate-income families.

FHA+ is published monthly by Gate House Strategies, a Washington, DC area-based advisory firm focused within the financial services, mortgage lending and servicing, community development, and public housing sectors. Contact us at FHAplus@gatehousedc.com