This Issue Includes:

- Think Piece: Michael Marshall and Gerald Flood on America’s housing supply dilemma — competing shortage estimates, structural underbuilding, affordability strain, and policy pathways to expand supply.

- Three Questions: Dror Oppenheimer on the post-pandemic loss mitigation reset, rising insurance pressures, and evolving risk management within FHA’s portfolio.

- Inside Voices: Reconciliation bill housing provisions, AI regulatory battles, FHA rescissions and foreclosure guidance, VA partial claim restoration, crypto in mortgage underwriting, CFPB shifts, BNPL scrutiny, and trigger lead reform.

- Gate House Index: Household growth vs. housing stock, mortgage payment-to-income pressures, competing shortage estimates, delinquency drivers, and supply-demand indicators.

THINK PIECE

The U.S. Housing Market’s Supply Dilemma

by Michael Marshall and Gerald Flood

There are varying estimates of a “housing supply shortage” in America, a well-accepted and supported belief that we have underbuilt or under-preserved enough housing units for our current and future needs. On the low end of these estimates, the market is said to be 1.5 million units short, [1] on the high end as many as 12.6 million. [2], [3] HUD Secretary Scott Turner recently cited a 7-million-unit deficiency in the U.S. market. [4]

Most of these estimates are not comparable because they use different definitions and methodologies to measure housing supply, demand, and shortage. Each of these assessments rests upon explicit or implied assumptions related to household formation – the number of actual households vs. the number of desired households, affordability – the share of housing supply that is affordable to segments of the population, and the natural vacancy rate – the share of housing supply that is vacant due to normal market frictions (properties for sale, properties for rent, properties undergoing rehab, etc.). [5]

In addition, most estimates attempt to measure the housing shortage based on an analysis of nationwide housing supply and demand factors, but the severity of shortages will vary by location and be dependent on these factors at a local level.

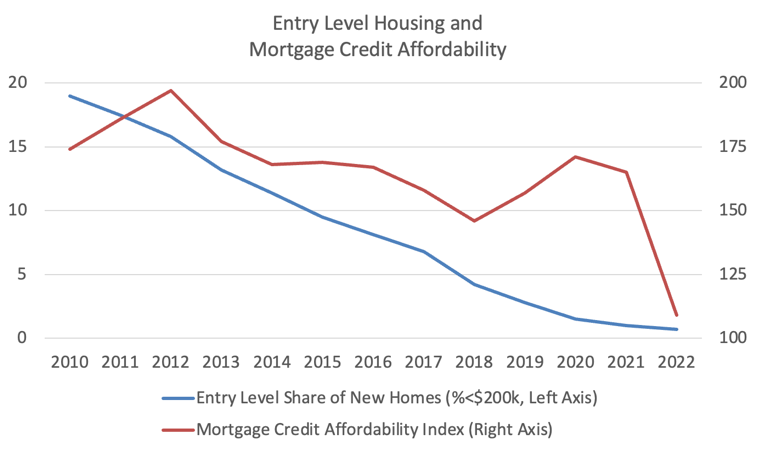

The sustained climb, and historically high, market prices for housing and home price-to-income ratios [6] are indicative of limited supply but also significantly influence the demand for housing. [7] In other words, if more units were available at affordable prices for rent or purchase, more individuals and families could and would make the meaningful milestone life transition to live in separate residences.

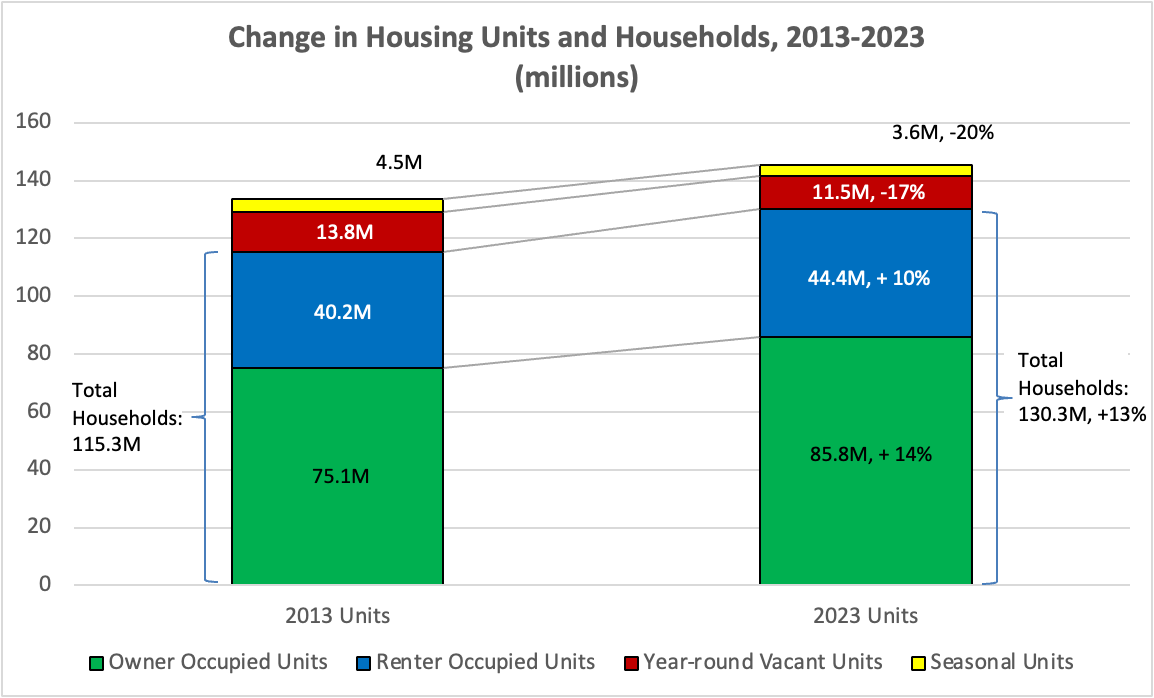

While in a functioning market rising price signals would induce more supply, ultimately relieving price pressures, that has not been occurring in sufficient numbers, particularly for affordable housing. Total housing stock, excluding seasonal units, grew 10% between 2013 and 2023, less than the 13% increase in the number of households. [8] In addition, total rental units grew only 8% between 2013 and 2023 and the number of units renting for less than $1,000 per month after adjusting for inflation declined more than 30 percent, but the number of units renting for $2,000 or more nearly tripled. [9]

Where does that leave the U.S. housing market? Looking to the next decade, households headed by a member of the Baby Boomer generation, now aged 61-79, are anticipated to decline due to expected mortality rates and transitions to assisted living or living with other households, often family members. A recent study commissioned by the Mortgage Bankers Association (MBA) estimates that homeowners aged 50 and above will add about 9 million units to housing supply between 2025 and 2035. [10] Adjusting MBA’s number to include renters means that householders aged 50 and above would add ~12 million units to housing supply over the next 10 years, a significant contribution…but not enough.

Consider recent projections from the Joint Center for Housing Studies of Harvard University (JCHS). JCHS expects the total number of households to increase by 8.6 million between 2025 and 2035, net of older Gen X and Baby Boomer effects. After accounting for natural vacancies, units built for seasonal use, and expected loss of some existing units, [11] JCHS projects the need for an additional 11.3 million units by 2035. [12]

During the prior decade (2010-2020), 9.9 million housing units were produced. Therefore, the U.S market will need to increase housing unit production by more than 10% and the supply of affordable housing will need to grow even more to meet expected demand in the coming decade. In the current environment, homebuilder confidence is near post-Great Recession lows [13] and many of the challenges to new home construction that persisted over the last decade continue: regulatory burdens – fees, permits, zoning; [14], [15] labor shortages, particularly skilled labor; and volatility in building material costs that have been affected by supply chain disruptions and tariffs. These challenges have driven up production costs, made the lower-priced homes that are affordable to median income earners and below less profitable to build, and contributed to a decreasing number of low-income units at the same time that the United States has an increasing number of low-income households.

Meanwhile, home sales including trade-up transactions have been suppressed by the lock-in effect for many homeowners who have a mortgage rate far below current levels, and an increasing number of homeowners who will be reluctant to sell because their property value has increased by more than the tax-exempt threshold for capital gains. That is to say, higher-income households are remaining in properties that are affordable to lower-income households more often than in prior periods, reducing the supply of affordable homes.

The result of all of this has been high-priced housing areas yielding higher prices; reduced affordability and fewer units available in areas with high job growth; reduced labor mobility; less ability for new construction to moderate home prices; [16] and importantly, a meaningful impact on the fabric of our society by altering typical, very natural household formation patterns – a dream deferred for millions of people perhaps.

The solutions have been elusive, but there are opportunities to make progress:

- Regulatory reform for residential property and new home development

- Streamline and reduce the cost of traditional single family and multifamily construction

- Support innovative building techniques and technologies that can bring down the price per square foot

- Optimization of vacant properties

- Encourage homes held off market to become available to new households.

- Promote rehab/restoration of vacant properties that can become occupied

- Lubrication of the market

- Tax reform that raises the exemption for capital gains on real property and indexes to inflation to accelerate existing home sales including units held off market

- New opportunities for government, GSE, and mortgage industry participants to respond to the evolving market, reduce costs, and encourage supply of affordable housing

It’s not all doom-and-gloom. That is, there are solutions that right-size supply and demand in the affordable space. But the current environment, saddled with regulatory and macroeconomic weights, is holding the market back and many aspiring households with it.

For more information, contact: FHAplus@gatehousedc.com.

THREE QUESTIONS

Dror Oppenheimer on the Changing Loss Mitigation Landscape, Policy Shifts --- and What to Watch

Dror Oppenheimer is a founding partner at Gate House Strategies, with over 35 years of experience in the mortgage industry. Most recently, he served as Senior Advisor to the FHA Commissioner, where he played a central role in modernizing single family servicing policies and FHA Catalyst technology. He helped lead FHA’s servicing response to COVID-19. Prior to FHA, he spent more than three decades at Fannie Mae, where he held leadership roles including Senior Vice President of Credit Default Operations and the National Underwriting Center.

Question: What has changed in the loss mitigation landscape, and how do you see it evolving?

Oppenheimer: Over the past few years, loss mitigation has been dominated by the COVID-19 response. The loss mitigation policies introduced in 2020 were designed as emergency relief for pandemic-related hardship, but they have extended well beyond the pandemic itself. I see 2025 as the turning point, when FHA transitions to a more normalized policy environment.

This next phase must focus on long-term sustainability for borrowers facing non-COVID hardships. With new limitations—such as borrowers being eligible for loss mitigation only once every 24 months starting in October—the need to find sustainable alternatives becomes more pressing. In many cases, a pre-foreclosure sale may be the best solution, especially if retaining the home is no longer viable. These softer dispositions can provide a win-win outcome by helping borrowers avoid foreclosure while preserving FHA Mutual Mortgage Insurance (MMI) Fund resources.

Question: What are the biggest shifts you see in the coming year?

Oppenheimer: The post-pandemic policy shift reflects dual goals: supporting sustainable homeownership and protecting taxpayers through responsible management of the MMI Fund. While the loss mitigation process remains relatively streamlined, borrowers are ultimately responsible for making key decisions.

One of the consequences of pandemic-era relief is a backlog of unresolved distress. Those policies let borrowers repeatedly request relief, and for some, this cycle may lead to increased delinquencies without long-term solutions. Some borrowers are now exhausting their options. Many who repeatedly accessed a partial claim may now be facing the reality that their financial situations haven’t improved enough to sustain homeownership.

Looking ahead, servicers will need to be proactive. A greater emphasis on evaluating long-term affordability and, when appropriate, guiding borrowers toward alternatives such as home sales or pre-foreclosure sales will be crucial to preventing unnecessary foreclosures.

Question: What makes the FHA portfolio unique, and how will FHA identify and mitigate risk?

Oppenheimer: FHA’s borrower profile and loan characteristics set it apart. Many FHA borrowers, especially recent ones, entered the market with higher loan-to-value (LTV) ratios and may not have built significant equity. In today’s higher-rate environment, home retention options like 40-year loan modifications are less effective and often require loans to be bought out of Ginnie Mae pools, adding cost and complexity. While well-intentioned, many of FHA’s retention options over the last few years have not delivered the desired success rates. The partial claim, which creates a second lien to defer missed payments, was being used more frequently and sometimes repeatedly on the same loans, which brings operational challenges and long-term risk to the MMI Fund. This concern was a motivation for the recent FHA policy change and is likely to be a focus area for FHA over the next year.

Additionally, rising homeowner insurance costs—estimated to have increased roughly 24 percent over the past three years—are compounding affordability issues and increasing delinquencies due to the higher monthly payments. [17]

Going forward, I expect FHA will monitor performance closely, measuring both borrower outcomes and taxpayer costs, and adjust loss mitigation policies accordingly. Re-default rates will be one key metric. Servicers should take this moment to reassess their readiness, capacity, and policies in light of evolving borrower needs and potential increases in default rates.

INSIDE VOICES

What we’re hearing around Washington and the industry

One Big Beautiful Bill: The U.S. Senate passed its version of the budget reconciliation bill, expected to clear the House prior to the July 4 holiday. In addition to general tax provisions and tax cut extensions, the bill includes a number of provisions related to housing, including LIHTC expansion, a mortgage interest deduction extension, support for Opportunity Zones, a New Markets Tax Credit (NMTC) Program extension, and increases to the State and Local Tax (SALT) Deduction cap, among others.

AI in the Reconciliation Bill: On July 1, the Senate voted 99-1 in favor of a bipartisan amendment to strip a ten-year moratorium on state AI regulations from the Republican budget reconciliation bill. Earlier, the bill had included a federal override on state AI laws. With the amendment's overwhelming support, that override is now effectively dead—underscoring the ongoing challenges of navigating a patchwork of state-specific AI rules.

FHA Rescissions: On June 27, FHA announced the rescission of more than 12 sub-regulatory policies under its Single-Family mortgage insurance program. The changes include eliminating outdated appraisal protocols, easing underwriter employment requirements, and removing the Supplemental Consumer Information Form (SCIF) mandate. FHA also rescinded the Federal Flood Risk Management Standard for new construction and dropped mandatory disaster inspection requirements.

FHA Foreclosure Bidding Practices: FHA’s foreclosure bidding practices are drawing scrutiny amid conflicting guidance—understandable, given the complex claims process, varied state laws, and the need to protect taxpayer funds. FHA is moving to update and clarify policies, a timely and welcome step.

VA Permanent Partial Claim: The VA Home Loan Program Reform Act is very close to a Senate vote to restore the permanent partial claim option. This vital tool may help veterans avoid foreclosure, replacing the temporary VASP program that ended in May. With strong bipartisan and veteran support, Senate action appears imminent.

VA Audits on Invoices: Speaking of the VA, auditors are zeroing in on detailed invoices for fees charged to VA borrowers per September’s Circular 26-24-19. If those invoices can’t be produced, borrower reimbursement may be required. Now’s a smart time for lenders to take a fresh look at this policy.

FHFA Directs GSEs to Weigh Crypto in Mortgages: The FHFA has ordered Fannie Mae and Freddie Mac to develop proposals for incorporating cryptocurrency into loan evaluations. This marks a major shift, integrating digital assets directly into the housing finance system for the first time. If implemented, this could allow crypto-savvy borrowers to leverage their holdings in the homebuying process.

CFPB Shifts and Funding Battle: The CFPB is scaling back enforcement and deprioritizing areas such as medical debt, student loans, and peer-to-peer (BNPL) platforms. A GOP-led push to cut the Bureau’s Fed-based funding is paving the way for partisan clashes. Legal challenges also loom as the agency moves to unwind Obama- and Biden-era regulations. As this plays out, in the meantime, expect state regulators to fill any gaps.

Mortgage Underwriting & Undisclosed Debt: Mortgage underwriting faces new risks from undisclosed borrower debt—especially BNPL accounts—that often escape traditional credit checks, complicating ability-to-repay assessments. Regulators are paying close attention, concerned about BNPL reporting gaps distorting DTI ratios and risk models. HUD issued an RFI seeking feedback by August 25.

Trigger Leads Crackdown: The House Financial Services Committee unanimously passed a crackdown on trigger leads, and the legislation is now at a critical stage as the House and Senate versions must be reconciled before final passage and presidential signature. If it becomes law, it’s game over for the flood of 50+ spam calls and misleading texts borrowers often receive after applying for a loan—calls that go beyond annoying to outright deceptive.

THE GATE HOUSE INDEX

The Gate House Index and analysis is designed to provide insight into the status of FHA’s business at a moment in time and over a period of time, as well as other pertinent data points we’re following.

This month, we focus on factors influencing both the supply and demand for housing that impact the rise in unaffordability in many areas of the country.

Household growth (+13%) exceeded growth in housing units (+10%) between 2013 and 2023 ….

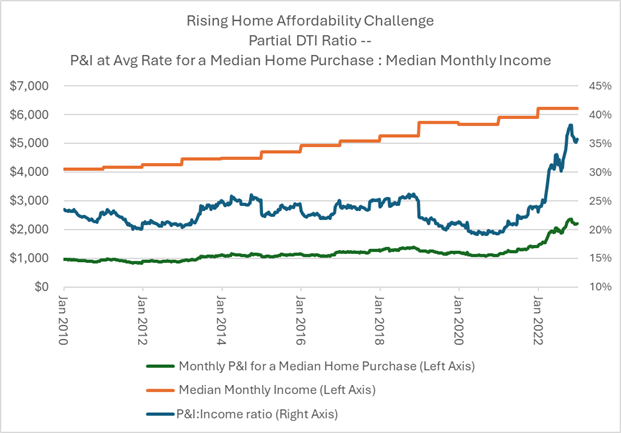

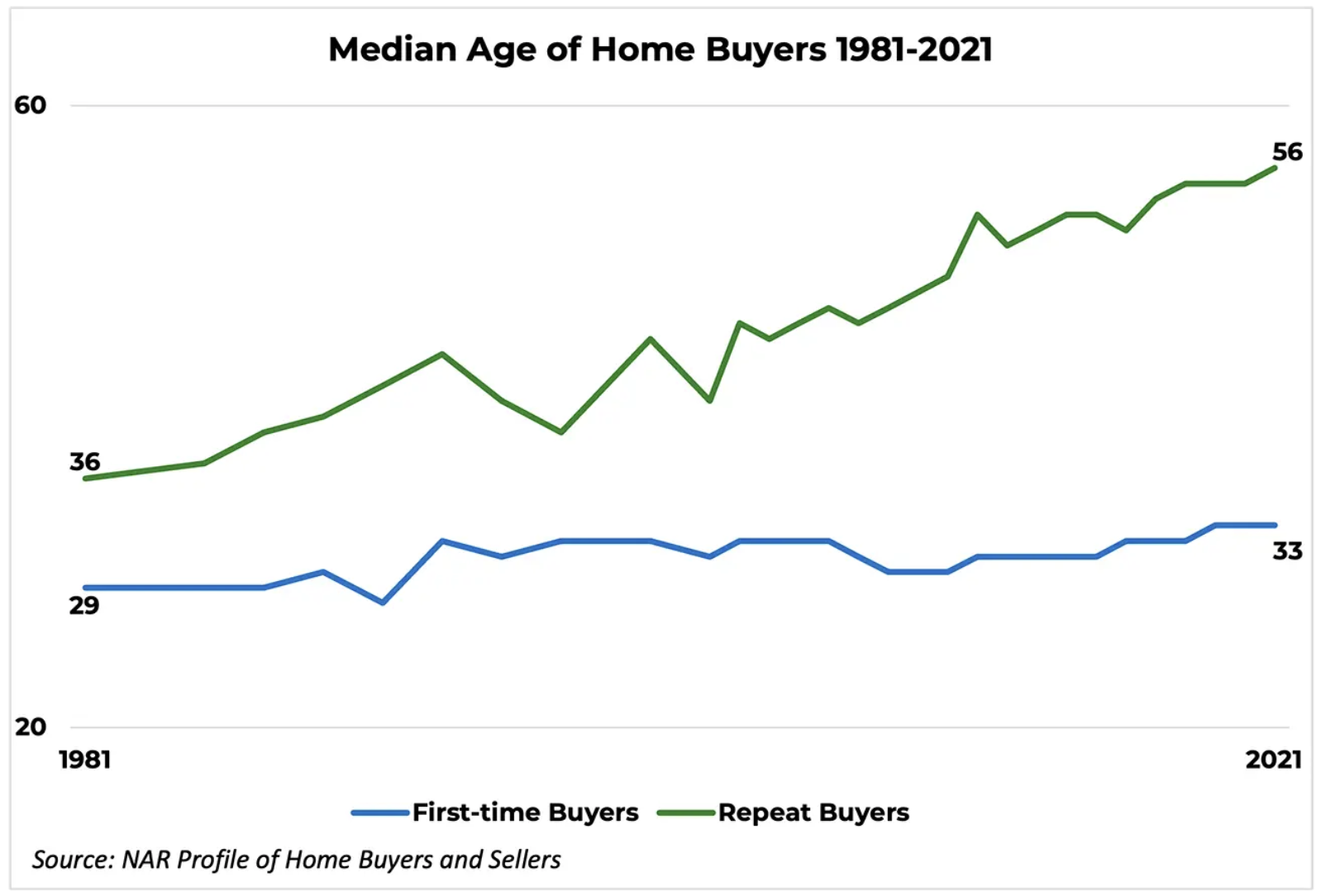

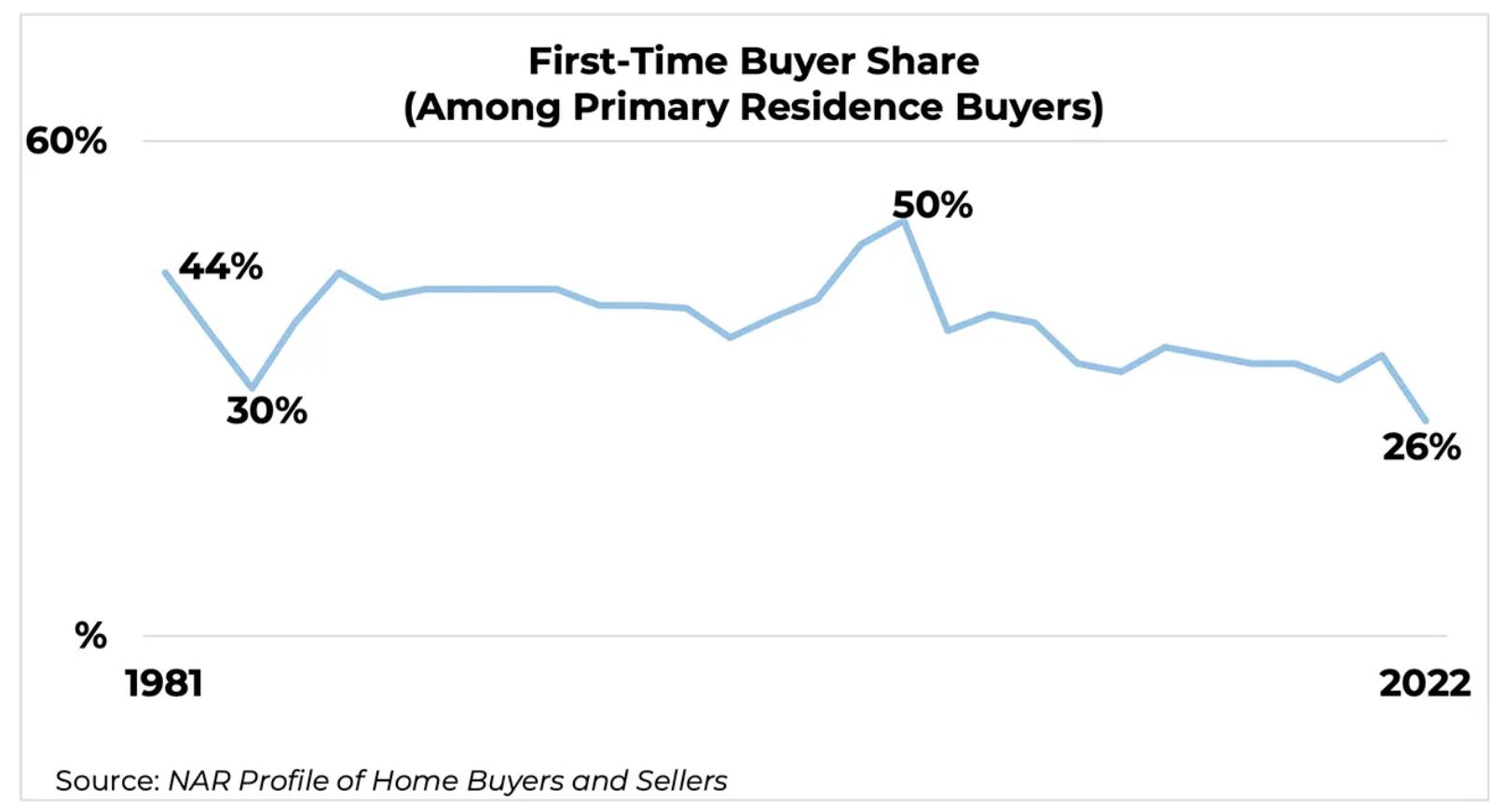

We can see the rapid increase in average mortgage P&I relative to median income (blue line) in the United States ….

/millennials-still-underperforming-amid-gains-in-homeownership-rate

There are a variety of estimates for U.S. housing shortage:

This Month In History

The Federal Home Loan Banks were created by an act of Congress signed into law by President Herbert Hoover on July 22, 1932, aimed at providing financial services to member institutions, assist in housing finance, and stimulate community investment.

FHA+ is published monthly by Gate House Strategies, a Washington, DC area-based advisory firm focused within the financial services, mortgage lending and servicing, community development, and public housing sectors. Contact us at FHAplus@gatehousedc.com

[1] National Association of Home Builders; https://eyeonhousing.org/2022/12/the-size-of-the-housing-shortage-2021-data/

[2] The National Low Income Housing Coalition; The GAP: A Shortage of Affordable Homes, 2025; https://nlihc.org/gap, pgs 8, 10

[3] Although not a measure of housing shortage, the Harvard Joint Center for Housing Studies (JCHS) estimates that 42.9 million U.S. households were cost-burdened (housing expenses > 30% of income) in 2023, including 21.5 million households that were severely cost-burdened (housing expenses > 50% of income); https://www.jchs.harvard.edu/sites/default/files/reports/files/Harvard_JCHS_The_State_of_the_Nations_Housing_2025.pdf, pg 48

[4] Bipartisan Policy Center Housing Supply Summit, June 18, 2025

[5] In 2024, there were 15.1 million more housing units than households due to various reasons for vacancy.

[6]Harvard JCHS; The State of the Nation’s Housing, 2025, pgs 1, 10-11

[7] https://www.brookings.edu/articles/make-it-count-measuring-our-housing-supply-shortage/

[8] The number of vacant properties declined by 18%. U.S Census; Housing Vacancy Survey Table 7a; https://www.census.gov/housing/hvs/data/histtabs.html

[9] Harvard JCHS, The State of the Nation’s Housing 2025; pg 5

[10] MBA; Who Will Buy the Baby Boomers’ Homes When They Leave Them? An Update; https://www.mba.org/docs/default-source/research---riha-reports/27088-research-riha-silver-tsunami-update-2024.pdf?sfvrsn=19894734_1, pg 5

[11] Units removed from the market due to demolition, natural disasters, repurposing, etc.

[12] In an alternative low-immigration scenario, households are projected to increase by 6.9 million and the number of required new units would be 9.5 million.

[13] NAHB; https://eyeonhousing.org/2025/06/builder-sentiment-at-third-lowest-reading-since-2012/

[14] NAHB; Government Regulation in the Price of a New Home, 2021: “regulation … accounts for 23.8 percent of the final price of a single-family home”

https://www.nahb.org/blog/2021/05/Regulatory-Costs-Add-a-Whopping-93870-to-New-Home-Prices

[15] NAHB; Regulation: 40.6 Percent of the Cost of a Multifamily Development;

[16] NBER; https://www.nber.org/system/files/working_papers/w33876/w33876.pdf

Units held off market: occasional use, usual residents elsewhere (URE), and other (undergoing renovation; in legal dispute; uninhabitable; awaiting demolition; abandoned)