This Issue Includes:

- Think Piece: Keith Becker on restoring the VA partial claim — strengthening home retention for veterans while protecting taxpayers and the VA Home Loan Program.

- Three Questions: Liz Scholz on ending Fannie Mae and Freddie Mac conservatorship — capital plans, UMBS safeguards, and managing market stability.

- Inside Voices: CFPB retrenchment, FHA policy resets, FHFA reorganization and fraud focus, AI-powered underwriting advances, and rising delinquency concerns.

- Gate House Index: FHA partial claim trends, VA and FHA delinquency shifts, foreclosure pressures, and early signals on housing supply dynamics.

THINK PIECE

A Benefit for Our Nation’s Warriors (and the VA Home Loan Program)

by Keith Becker

The U.S. Senate is poised to approve a bill to provide the Department of Veterans Affairs (VA) with the means to assist military and veteran homeowners facing temporary financial difficulty. The authorization and funding, passed by the House of Representatives on May 19, is critically important to the VA Home Loan Program. The additional home retention measure, the so-called “partial claim,” which moves missed payments to a non-interest bearing second lien, helps borrowers who have experienced a setback but who are ready to resume their regular payments.

While not a panacea for borrowers who have long-term financial issues, the new facility is a vital step toward remedying a major gap that currently exists in the VA’s toolkit. The hole has left warrior families at a disadvantage compared to Federal Housing Administration (FHA) and conventional loan borrowers. Filling it will benefit them and the health of the VA’s loan program.

Active-duty members of the U.S Armed Forces, veterans, and their surviving spouses have access to lower-cost mortgage loans through the VA Home Loan Program. The program guarantees a portion of the mortgage loan amount for eligible borrowers and in most cases does not require them to make a down payment. But FHA and Government Sponsored Enterprise (GSE) loan programs have certain capacities to help struggling borrowers that the VA lacks, including the partial claim, an absence that not only undermines the service member’s earned benefit, it adds costs to the program.

VA requires mortgage servicers to assist delinquent borrowers and manage potential loss to the government. VA’s loss mitigation approach prioritizes home retention when possible, but with prevailing mortgage rates above the note rate on many existing mortgages, loan modification options are often not a viable solution because they generally result in higher, not lower, monthly payments.

For the past year, prior to being cancelled May 1, VA options included a subsidized loan modification program -- The Veterans Affairs Servicing Purchase (VASP) program that reduced the mortgage rate to 2.5% -- as a last resort. VASP was helpful to struggling military families because it allowed them to become current on their loan and resume payments without requiring immediate repayment of past missed payments.

The VASP program did have issues, including exposing VA to more risk and, detractors argued, it exceeded Congressional intent related to the VA’s authority to purchase loans. Regardless, VASP was ended without providing a tool in its place that could work for borrowers in today’s economic environment. Cancellation of VASP leaves many families who are experiencing hardship with a tougher path to retaining their home. The need for an additional option that helps veteran and military families retain their homes rightfully garnered the attention of lawmakers on Capitol Hill.

The most obvious candidate was the partial claim because it has proven itself to benefit FHA borrowers, for example, while also reducing FHA mortgage credit losses.[1]

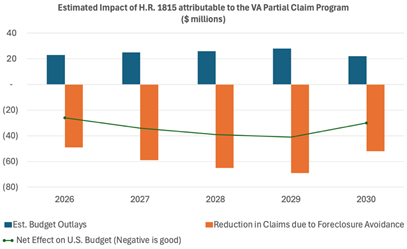

The partial claim enables additional VA families to avoid the trauma and disruption of losing their home while also providing a net benefit to the VA program. The CBO estimates the proposed partial claim provisions in the House bill (which are limited to 5 years) will prevent more than 12,000 foreclosures and have a net positive impact of $170 million on the federal budget over the next 5 years.[2]

It should be noted that for a period during the COVID-19 pandemic, July 27, 2021 – October 28, 2022, Congress granted the VA temporary authority to offer partial claims via its COVID-Veterans Assistance Partial Claim Payments Program. That effort included some execution challenges, but enabled over 145,000 veterans and their families to retain their homes and avoid foreclosure during and after the pandemic.[3] The VA experience with partial claims as recently as 2022 should streamline implementation and facilitate execution of the program in 2025.

Conclusion:

The partial claim is a win-win – helping veteran families retain their homes and reducing cost to the government.

The VA bill (H.R.1815) flew through the U.S. House on a voice vote. The Senate is set to move swiftly on a version of the same bill, granting the VA authority to develop and implement a partial claim program and also provide the funding to assist currently delinquent VA borrowers and those borrowers that may become delinquent in the future.

A month has passed since VASP ended. It is urgent that the Senate act quickly so the VA can move decisively to implement the partial claim program and help ensure veterans do not suffer foreclosure unnecessarily. In addition, VA should take advantage of lessons learned from its prior experience with partial claims and the experience of FHA in this area (and work with FHA as necessary) to speed the implementation.

Our nation’s warriors and their families that experience temporary financial difficulties deserve our support.

For more information, contact: FHAplus@gatehousedc.com.

[1] The reduction in foreclosures and foreclosure losses more than offsets the cost of the partial claims.

[2] CBO Cost Estimate of H.R. 1815, https://www.cbo.gov/system/files/2025-05/hr1815.pdf

[3] John Bell, Executive Director of Loan Guaranty Service at VA, to a House subcommittee on Veterans Affairs:

https://www.congress.gov/118/meeting/house/116827/witnesses/HHRG-118-VR10-Wstate-BellJ-20240215.pdf

THREE QUESTIONS

Liz Scholz on the Path to Ending Fannie Mae and Freddie Mac Conservatorship

Liz Scholz is a Senior Advisor at Gate House Strategies, where she specializes in compliance, risk, and client strategies. She spent 12 years as an executive at the Federal Housing Finance Agency (FHFA), leading key work in examination, regulatory policy, and board oversight of Fannie Mae and Freddie Mac. In this month’s “Three Questions,” Liz shares her perspective on what’s ahead for ending the conservatorship of the Government-Sponsored Enterprises (GSEs).

QUESTION: When we listen to the current chatter around conservatorship, much of it focuses on the MBS market. You’ve said some of that talk misses the point. Can you explain what you mean?

SCHOLZ: As a former FHFA executive, I was deeply involved in conservatorship operations, including the development and launch of the UMBS. Some chatter includes a concern that the Fannie and Freddie MBS might be disrupted by an exit. What’s often overlooked in the narrative is that FHFA issued a formal rule[4]—effective May 2019—specifically to govern the structure and oversight[5] of the combined Fannie Mae–Freddie Mac UMBS.

A common concern is that in a post-conservatorship era, the Enterprises could diverge in their approach to mortgage-backed securities, creating bifurcation and even disruption. But that’s exactly the scenario the 2019 rule was designed to prevent. The rule requires FHFA to ensure ongoing alignment between the Enterprises’ MBS-related policies. It wasn’t a temporary measure—it’s binding, and it ensures that the core goal of the UMBS remains intact: to maintain a single, interchangeable security that maintains a market standard and liquidity, even after the GSEs exit conservatorship. Maintaining that alignment remains FHFA’s obligation.

[5] https://www.ecfr.gov/current/title-12/chapter-XII/subchapter-C/part-1248

QUESTION: Assuming an end to the GSE conservatorships will be pursued, can you walk us through how you envision the transition process unfolding?

SCHOLZ: The first step is comprehensive planning. Much of the groundwork was laid during Director Calabria’s tenure, and that work is still highly relevant. At the time, both Fannie and Freddie, with FHFA’s leadership, engaged advisory firms to help with the analysis of capital-raising strategies and transaction structuring.

With Director Pulte now at the helm of FHFA and the GSE Boards, FHFA is in a strong position to take a proactive role. Treasury will play a critical role, given its financial stake and its responsibility to taxpayers. Collaboration between FHFA and Treasury will be crucial—particularly around the terms of the Preferred Stock Purchase Agreements, which may require revision or even termination.

Another key consideration is the GSEs’ capital position. Fannie and Freddie have retained over $150+ billion in capital—significant progress, but more to do here. And exiting conservatorship will require more than just meeting the current capital rule. FHFA must ensure that there are credible capital plans, while also putting in place additional guardrails to preserve safety and soundness post-exit.

FHFA also needs to conduct a thorough gap analysis—evaluating which authorities it holds today as conservator and what powers it would lose post-conservatorship. Identifying those gaps early is essential. From there, the agency can determine how to preserve critical authorities, whether through new regulations, guidance, or administrative mechanisms. While legislation might be a heavier lift, FHFA’s existing regulatory toolbox should be sufficient to address most, if not all, of the transition challenges.

QUESTION: Are you concerned about market disruption during this transition?

SCHOLZ: It’s important to acknowledge the potential for disruption—but equally important to recognize that it can be managed. The key is thoughtful planning, risk mitigation, and a disciplined approach to execution.

There’s speculation that rates could rise or that the market might destabilize as conservatorship ends. I don’t share that view. Yes, I agree that there are risks, but they can be addressed. A major mitigant is the UMBS itself. Its 2019 launch created a unified, $7+ trillion market by merging Fannie’s and Freddie’s previously separate MBS platforms, creating unprecedented MBS market liquidity. This move also eliminated the so-called MAP costs—inefficiencies that added over $800 million annually[6] in guarantee fee costs due to Freddie’s historically less liquid securities. That fragmentation is gone.

The UMBS framework was intentionally built to create and preserve the combined market liquidity. FHFA has both the authority and the ongoing responsibility to protect the UMBS market’s integrity. That means continuing to act as the UMBS regulator—even when it’s unpopular—to ensure stability in the broader housing finance system.

Under previous Director Calabria, FHFA proposed a methodical conservatorship exit framework centered on safety, capital adequacy, market stability, and transparency. I expect those same principles will guide the process under this administration. That includes stakeholder engagement, market impact analysis, risk mitigation plans, and coordination within the federal government.

Both Director Pulte and Treasury Secretary Bessent have emphasized that market disruption is unacceptable – this means developing a sound and thoughtful approach. Moving too quickly, without a comprehensive plan, could destabilize the mortgage market—something no one wants. What’s clear is that this administration is committed to a thoughtful, orderly exit. With solid analysis, smart planning, adequate resources, and steady leadership, I believe that’s very achievable.

[6] https://www.newyorkfed.org/medialibrary/media/research/staff_reports/sr965.pdf?sc_lang=en

INSIDE VOICES

What we’re hearing around Washington and the industry

CFPB: What we’re seeing for the CFPB: Withdrawal of at least 67 various regulatory actions. A scale back to prevent duplication with states. Some states will likely pick up regulatory activity. Sources are indicating large banks will become more of a future CFPB target. Mortgage fraud and bad actors remain key areas of concern. CFPB is re-reviewing actions, and where cases are not well proven, including discrimination cases, they will be dropped. Recent internal guidance curtails examination and supervision activity. OMB Director Russell Vought and former FHFA Director Mark Calabria continue to play a large role in CFPB actions.

FHA: At FHA, resources and budget cuts are top of mind. Over 600 policy documents were archived to support AI inquiries. Biden era post REO sales restrictions were rescinded. Recent MLs include loss mitigation waterfall changes that bring pre-pandemic policy back (with guardrails). The Payment Supplement effectiveness is under review. Defaults and foreclosure may increase due to limits on forbearance options.

FHFA: We’re hearing the reorganization at FHFA is done for now. Significant changes were made. Director Pulte fired GSE staff for fraud and unethical conduct (contractors, falsifying residency status and more); let go of 27% of FHFA staff. Increased focus for the agency: concerns about mortgage fraud. The Director also announced A Crime Detection Unit powered by Palantir AI will dig deeper at Fannie Mae to detect fraud. Director Pulte garnering big kudos for greenlighting Freddie Mac’s new AI-powered underwriting tools—cutting mortgage costs, speeding up closings, and helping gig workers buy homes. “These are the kinds of smart, tech-forward ideas housing needs right now,” Gate House Strategies co-founder Brian Montgomery posted on LinkedIn.

THE GATE HOUSE INDEX

The Gate House Index and analysis is designed to provide insight into the status of FHA’s business at a moment in time and over a period of time, as well as other pertinent data points we’re following.

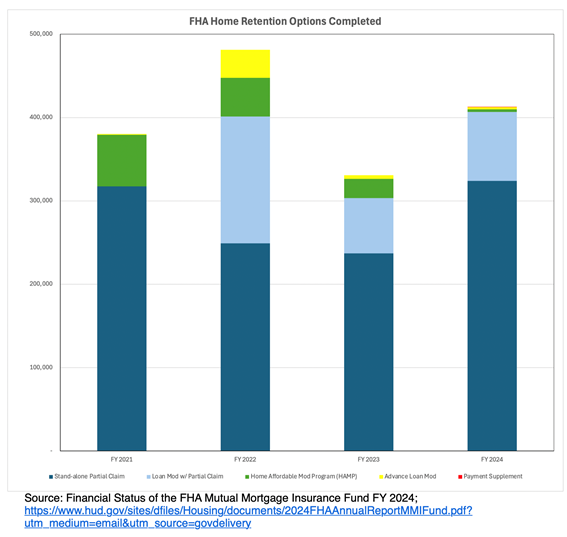

The following chart demonstrates that in recent years, partial claims have been the leading home retention option for FHA loans. "While active loss mitigation using Partial Claims funds uses resources from the MMI Fund, many more losses are avoided given the high costs of foreclosure," FHA’s Report to Congress on the Status of the Mutual Mortgage Insurance Fund said.

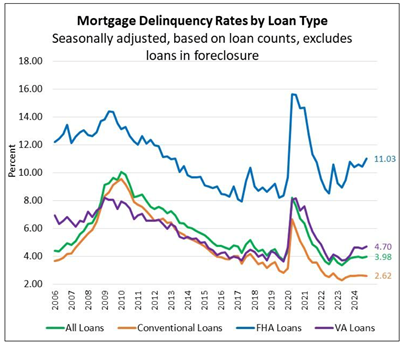

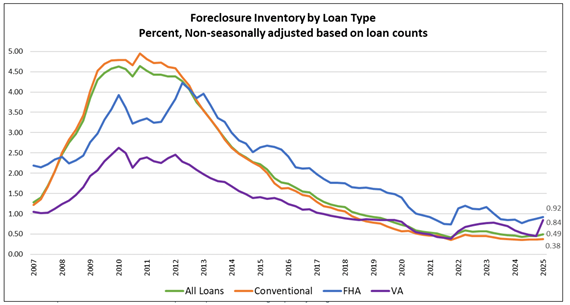

The next two charts highlight perhaps even greater urgency to the bill being considered by Congress. FHA and VA delinquencies have trended up to above pre-pandemic levels and VA foreclosures spiked upward in early 2025.

Source: MBA Delinquency Survey

Marina Walsh of the MBA noted: “The percentage of VA loans in the foreclosure process rose to 0.84 percent, the highest level since the fourth quarter of 2019.” Also, Walsh explained: "a voluntary VA foreclosure moratorium was in effect through the end of 2024 to allow time to implement the Veterans Affairs Servicing Purchase (VASP) Program. That program has since ended without a replacement loss mitigation option approved by Congress. Further increases in the foreclosure rate could result if economic conditions worsen and loan workout options are unavailable."

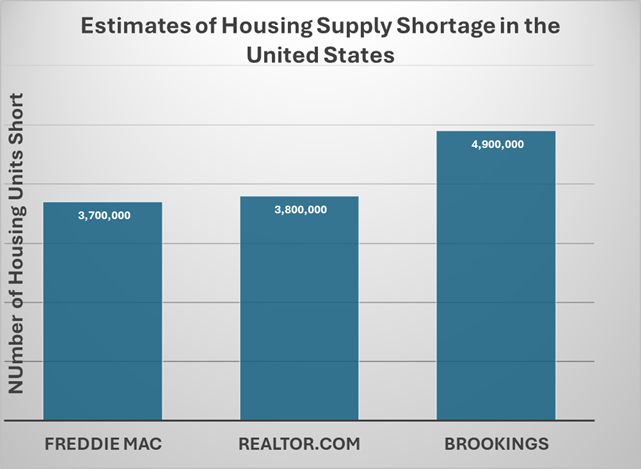

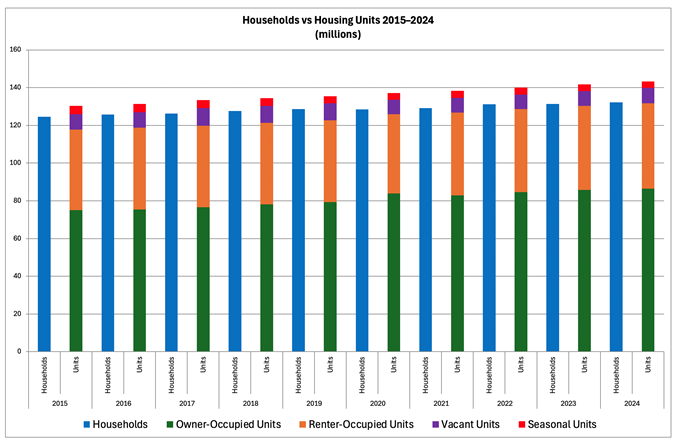

We’ll be looking at the housing supply in the next issue of FHA+. We thought we would share just two charts. The first one simply provides a few of the recent estimates of how undersupplied the current market is based on different methodologies. The second chart illustrates that, despite the shortage in housing supply, the total number and growth rate of U.S. Housing Units has exceeded the number and growth rate of U.S. Households over the past 10 years. Of course, household formation has been held back by lack of affordable units in locations where they are needed. We’ll get into all of this and the mismatch in housing in some places next month, but it’s interesting.

FHA+ is published monthly by Gate House Strategies, a Washington, DC area-based advisory firm focused within the financial services, mortgage lending and servicing, community development, and public housing sectors. Contact us at FHAplus@gatehousedc.com