This Issue Includes:

- Think Piece: Paul Hancock on appraisal bias allegations, TILA independence rules, FHA policy rescissions, and how lenders can navigate fair lending risk without crossing legal lines.

- Three Questions: Brian Montgomery on why RESPA belongs back at HUD — restoring housing-focused oversight and regulatory clarity.

- Inside Voices: Rising FHA delinquencies, DACA eligibility shifts, loss mitigation transitions, SDQ trends, and the end of VASP amid calls for VA partial claim authority.

- Gate House Index: FHA’s countercyclical role, delinquency drivers, foreclosure trends, Ginnie Mae market share growth, and evolving MBS dynamics.

THINK PIECE

When Allegations of Appraisal Bias Put Lenders “Between a Rock and a Hard Place”

by Paul F. Hancock

In recent years, mortgage lenders have faced a double bind when it comes to avoiding charges of discrimination in property appraisals. On one hand, the Truth in Lending Act (TILA) mandates appraisal independence, prohibiting lenders from interfering with the appraisal. Under TILA, a lender can face liability by encouraging an appraiser to increase the value of a property. Conversely, enforcement agencies have been quick to charge originating lenders with liability under the Fair Housing Act if the agencies believe the appraisal supporting a loan is tainted by discrimination—and the lender has not taken steps to remedy the discrimination. “These conflicting forces put a lender between a rock and a hard place,” says one industry observer.

Allegations of discrimination in appraisals rank among the hottest fair lending issues in recent years, with federal, state, and local agencies, and consumer advocacy groups, all joining the fray. Claims most frequently arise in refinance lending where homeowners, no matter what their race, believe their homes have been undervalued by appraisers. To confuse matters, lenders over the past year have received contradictory direction from the U.S. Department of Housing and Urban Development (HUD). In May 2024, the Biden administration issued HUD’s Mortgagee Letter 2024-07, which established detailed appraisal requirements for FHA loans, including appraisal reviews, second appraisals, and borrower-initiated requests for Reconsideration of Value (ROV).

In March, the Trump administration issued Mortgagee Letter 2025-08 that rescinded Mortgagee Letter 2024—07 and certain other FHA policies, with the purpose of “aligning with the Administration’s broader goal to reduce regulatory burden and foster long-term economic stability for all Americans.” Many practitioners expect that the same standard will be applied to loans acquired by Fannie Mae and Freddie Mac.

Case closed? Not so fast. In a March 4 federal court filing, HUD stated that it “views a [Fair Housing Act] violation as possible when a lender uses an appraisal... when the lender knows or reasonably should know that the appraisal improperly takes into consideration race.”

That appears to put lenders in the same predicament. While HUD is saying lenders should know when an appraisal is infected by racial bias (that results in an invalid reduction in property value), lenders still face the TILA requirement not to influence the independent judgment of the appraiser. Little guidance exists as to how a lender could respond to potential racial bias without contravening the TILA requirements.

But as always, the devil is in the details. A careful reading of HUD’s court filing reveals a note that TILA—notwithstanding its prohibitions—allows a lender to request an appraiser to consider additional information, provide further details, and correct errors. And although the strictures of the Biden era letter are rescinded, the document contains useful guidance for taking steps to address fair lending risk, such as establishing and disclosing processes and procedures for responding to borrower-initiated ROV requests, and training underwriters to recognize deficiencies in appraisals. When faced with plausible claims of bias, there are ways for a lender to lower its risk of legal liabilities.

For more information, contact: FHAplus@gatehousedc.com.

THREE QUESTIONS

for Brian Montgomery on RESPA

Gate House Strategies chairman and co-founder Brian Montgomery believes the Real Estate Settlement Procedures Act (RESPA) should be administered by the U.S. Department of Housing and Urban Development (HUD) … where it was managed for almost 40 years … and not by the Consumer Financial Protection Bureau (CFPB), where the responsibility currently resides. In this Q&A, the former HUD Deputy Secretary and FHA commissioner describes why the move makes sense.

Question: We should probably start by asking what is the purpose of RESPA?

Montgomery: Right. So, RESPA has two equally important goals. The first is to protect homebuyers from abusive practices in the real estate settlement process. It ensures they are fully informed about costs and prevents unnecessary charges. Equally important is the task of eliminating hidden costs to consumers by prohibiting kickbacks and referral-fees between real estate professionals involved in the process, including lenders, realtors, title companies, among others.

Question: Does RESPA achieve what it’s designed to do?

Montgomery: Yes, I believe it does. It took a while to get there but it was worth the effort. The entire mortgage process can be very intimidating for homebuyers especially first-time purchasers. It is more than likely the largest purchase of their life and they are under tremendous pressure, especially at loan closing. It’s something they go through only infrequently at best. And anyone who’s been there knows you’re sitting at a table with a stack of documents an inch or two tall. In the past, too many people were seeing the documents for the first time only when they were sitting down in the settlement or title company offices. And they’d be told, “OK, let’s start signing!” That’s all you did for an hour and a half until your fingers cramped. With no real opportunity to ask questions or understand the legalese of what you were signing.

With RESPA reform in 2008 and subsequent improvements, the language is all very clear now. Consumers can see the documents, ask questions, and know the amount of all closing fees days in advance of the closing day. The reform effort created greater transparency and greater certainty of costs. Buyers now have a much better sense of where their money is going, to whom and for what.

Question: Why should HUD administer RESPA, rather than the CFPB?

Montgomery: Well, first remember that HUD is where RESPA was administered for almost four decades following the Act’s passage in 1974. That made sense given that HUD is the nation’s housing agency.

Today, a particularly good case can be made that RESPA would be more efficiently and more effectively administered back in its original home—HUD. When Congress created the CFPB in 2010 as part of the Dodd-Frank legislation, it’s fair to say that those in power at the time figured they’d stand up what I’d call an uber-regulatory agency whose focus goes way beyond mortgages. In the process, they pulled RESPA under its purview. I think that was a mistake.

A housing mission isn’t really in the CFPB’s DNA quite frankly. CFPB has never focused on homeownership while that is HUD’s s most organic mission. Given that housing is outside the CFPB’s primary scope, I believe RESPA has been lost in the shuffle over there. On the other hand, HUD at its core is housing. That’s where the expertise and focus is for what it takes to administer a fundamentally housing-centric law. It’s simply common sense, from a practical, logistical, and operational perspective.

Now to be clear it’s not as if you could instantly move a singular division of one agency over to another. Because the CFPB organized itself by function rather than by law or market, there isn’t a separate “RESPA Office” so to speak. There is the enforcement team that is responsible for identifying and litigating violations of RESPA and TILA, as well as ECOA and UDAAP. There are examiners who are responsible for evaluating compliance with those laws. And there are rule writers who craft regulations consistent with those laws.

But with the future of CFPB’s structure and focus in question, it’s appropriate for Congress to act and move RESPA back to HUD. As the Trump Administration and Washington policymakers are working hard to create greater efficiencies in the federal government, I believe it’s time to bring RESPA home to HUD.

INSIDE VOICES

What we’re hearing around Washington and the industry

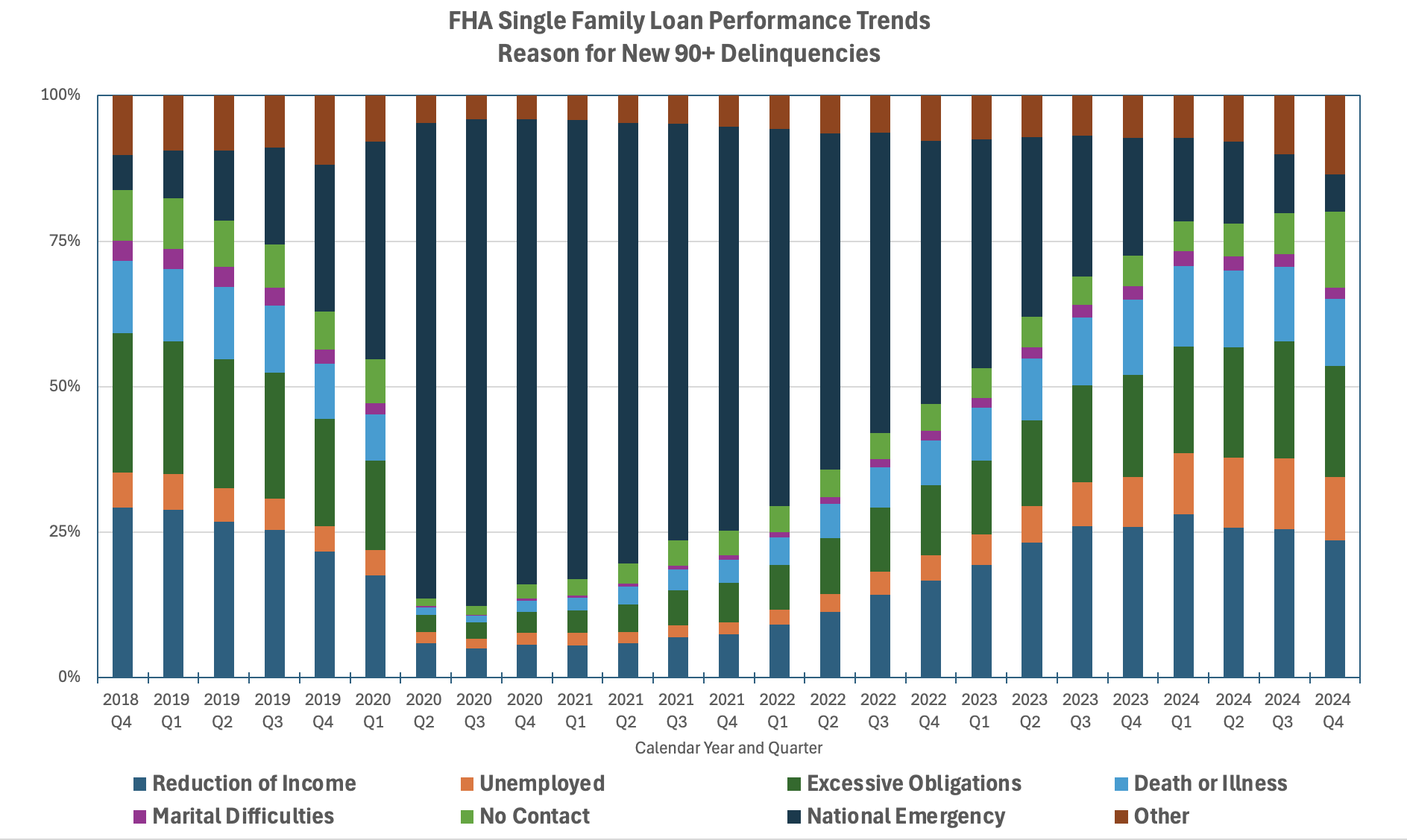

FHA Performance: As of this writing, FHA had published its data on reasons for loan delinquency through January 2025, the first month of the 2025 fiscal second quarter (Q2 2025). Through January, the FHA loan performance report showed new 90+ day delinquencies continuing to grow. As the share of delinquencies attributable to the pandemic continues to decline, the reasons for borrowers to be seriously delinquent were led by ‘Reduction of Income’ (23%) and ‘Excessive Obligations’ (18%) at the beginning of Q2 2025. “Based on loss mitigation programs at the end of 2024, most in the industry were staying calm. With its claims paying capacity the highest in its history, FHA should be well positioned to manage any number of economic downturns,” says Gate House founding partner Keith Becker and former FHA chief risk officer.

DACA: Now that HUD announced it would eliminate the “non-permanent residents” category from FHA loan eligibility (including DACA status recipients and H1-B visa holders even though they are legally permitted to remain in the U.S.), insiders are wondering if Fannie and Freddie will follow suit. If so, immigrants, including DACA recipients and H1-B visa holders, would be barred from GSE-backed mortgages. Concern is growing that new federal housing policies will disrupt business models built in recent years.

Loss Mitigation: HUD released an April 15 Mortgagee Letter that provides more guidance on the loss mitigation waterfall. Current policies include COVID emergency provisions. The new and more permanent offering will transition to reflect certain pre-pandemic policies, including important guardrails while retaining benefits such as the streamlined features for processing. “FHA likely will continue to monitor performance and adjust policy as needed over time,” says Dror Oppenheimer, founding partner and former senior advisor to the FHA Commissioner.

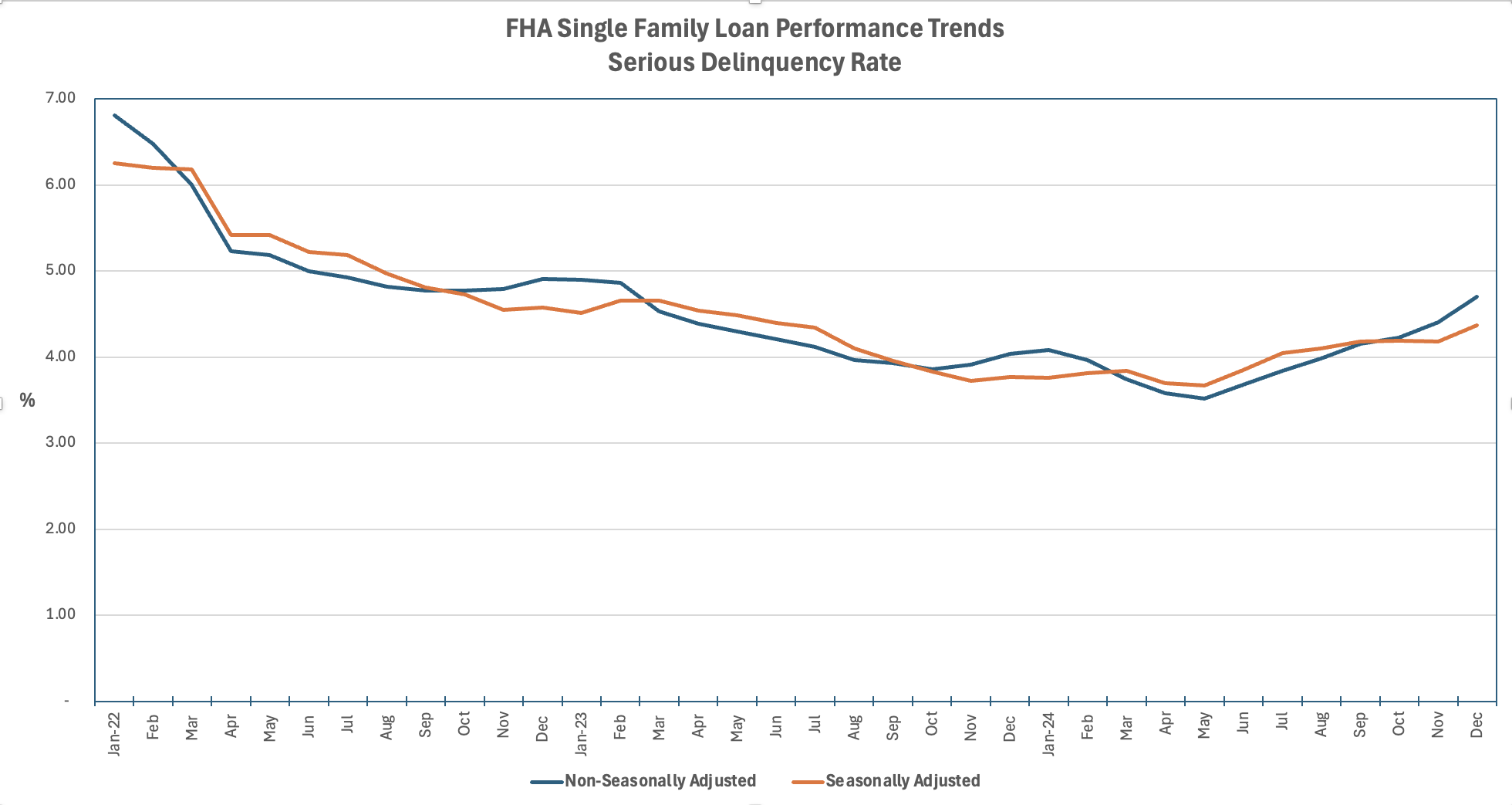

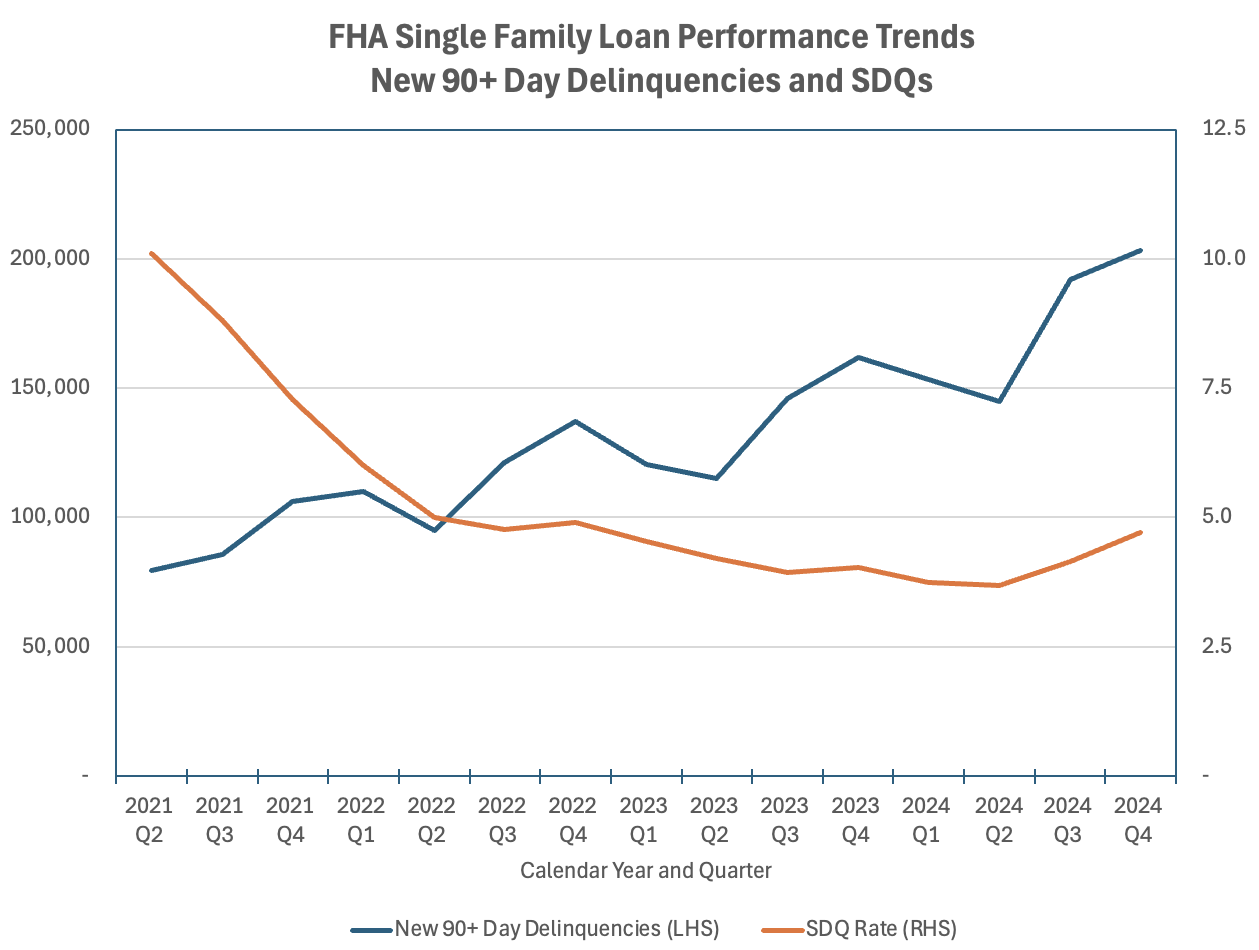

FHA SDQs: While “re-default” data on FHA borrowers is not publicly available, “We saw 90-day delinquencies rise over several quarters with no appreciable effect on the SDQ rate, one indication that loss mitigation efforts are keeping those who re-default from SDQ status,” says Gate House founding partner Michael Marshall who served as Acting Assistant Secretary for the Office of Policy Development and Research (PD&R) at HUD. “SDQs turned slightly upward in recent months and could continue higher as potential recycling of defaulted loans is reduced by the servicing policy change that limits loan modifications to 1 every 2 years as of October 1, 2025. In addition, a reduction in loan modifications and partial claims could put upward pressure on servicer advances.”

VASP: After political criticism for lack of accountability and risks posed to the VA, the VA Servicing Purchase program (VASP) ceased to accept new applications as of May 1. As lenders and servicers look for ways to help military service members and veterans who are struggling to avoid foreclosure, Congress has introduced legislation to provide partial claim authority to the agency similar to FHA’s. With a Senate Veterans Affairs Committee hearing set for this week and both House and Senate bills introduced, we can hope for an expedited process. It is important that veterans have loss mitigation options that prevent unnecessary foreclosures similar to FHA and the GSEs.

THE GATE HOUSE INDEX

The Gate House Index and analysis is designed to provide insight into the status of FHA’s business at a moment in time and over a period of time, as well as other pertinent data points we’re following.

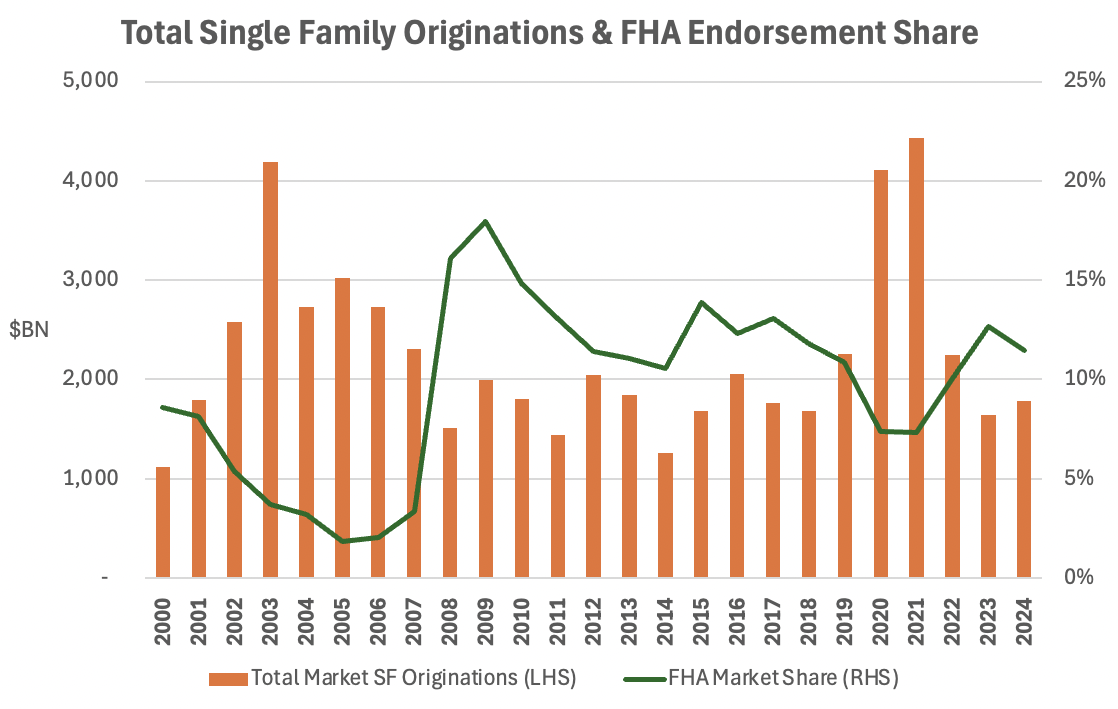

The following chart demonstrates the countercyclical nature of FHA’s business. When economic conditions are more difficult and new mortgage activity declines, more borrowers tend to use FHA loans to buy their homes:

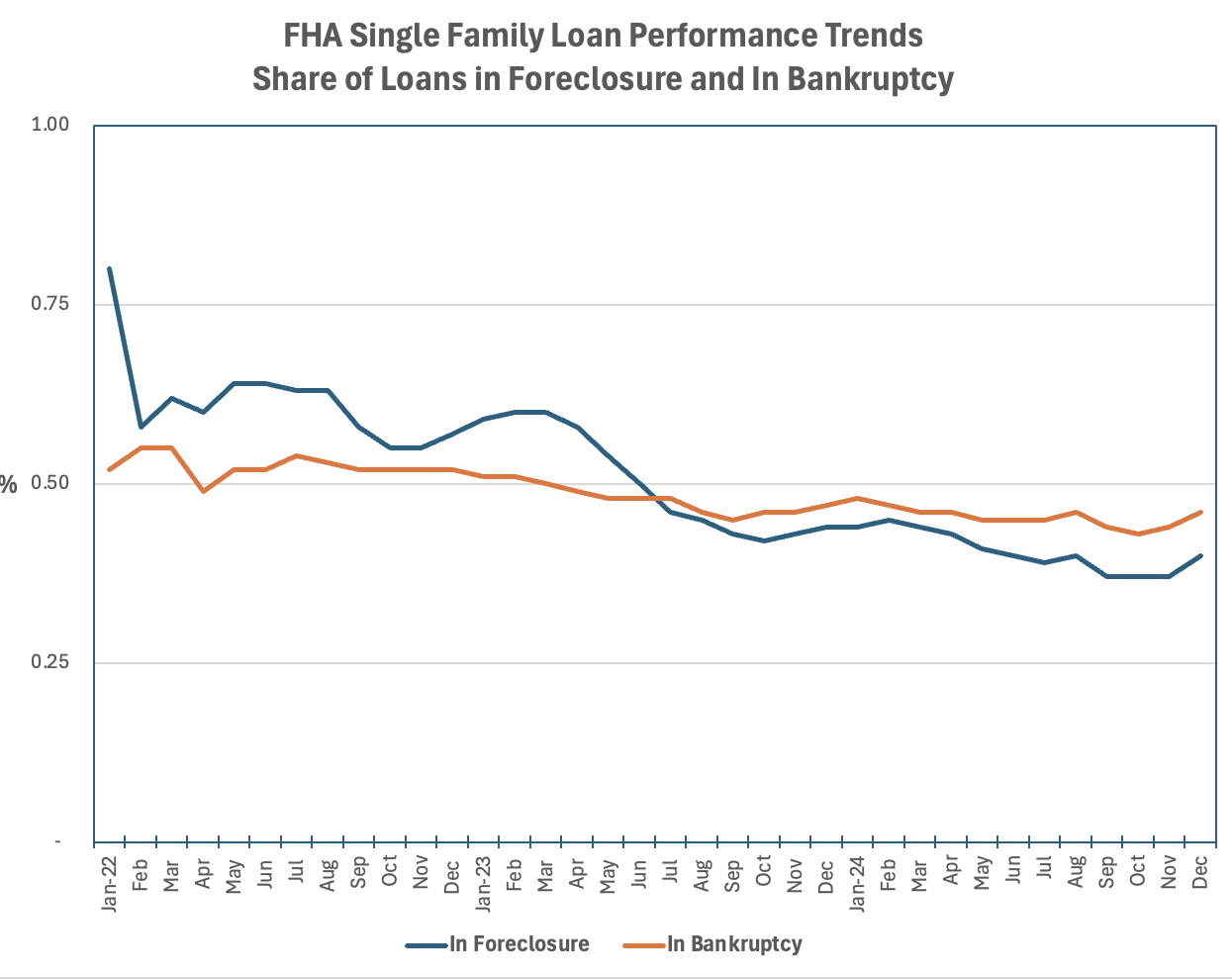

FHA SDQs have declined from pandemic highs. Though relatively flat relative compared to new 90+ delinquencies, the rate appears to have turned up since Q2 2024. FHA loans in foreclosure and bankruptcy remains low. COVID modifications may have continued to depress these rates, which is set to change.

The share of FHA delinquencies attributable to the pandemic have declined significantly. The reason for serious delinquency is now led by ‘Reduction of Income’ and ‘Excessive Obligations.’ (We expect the Q4 2024 ‘No contact’ share to decline and be distributed to other categories in future reports.)

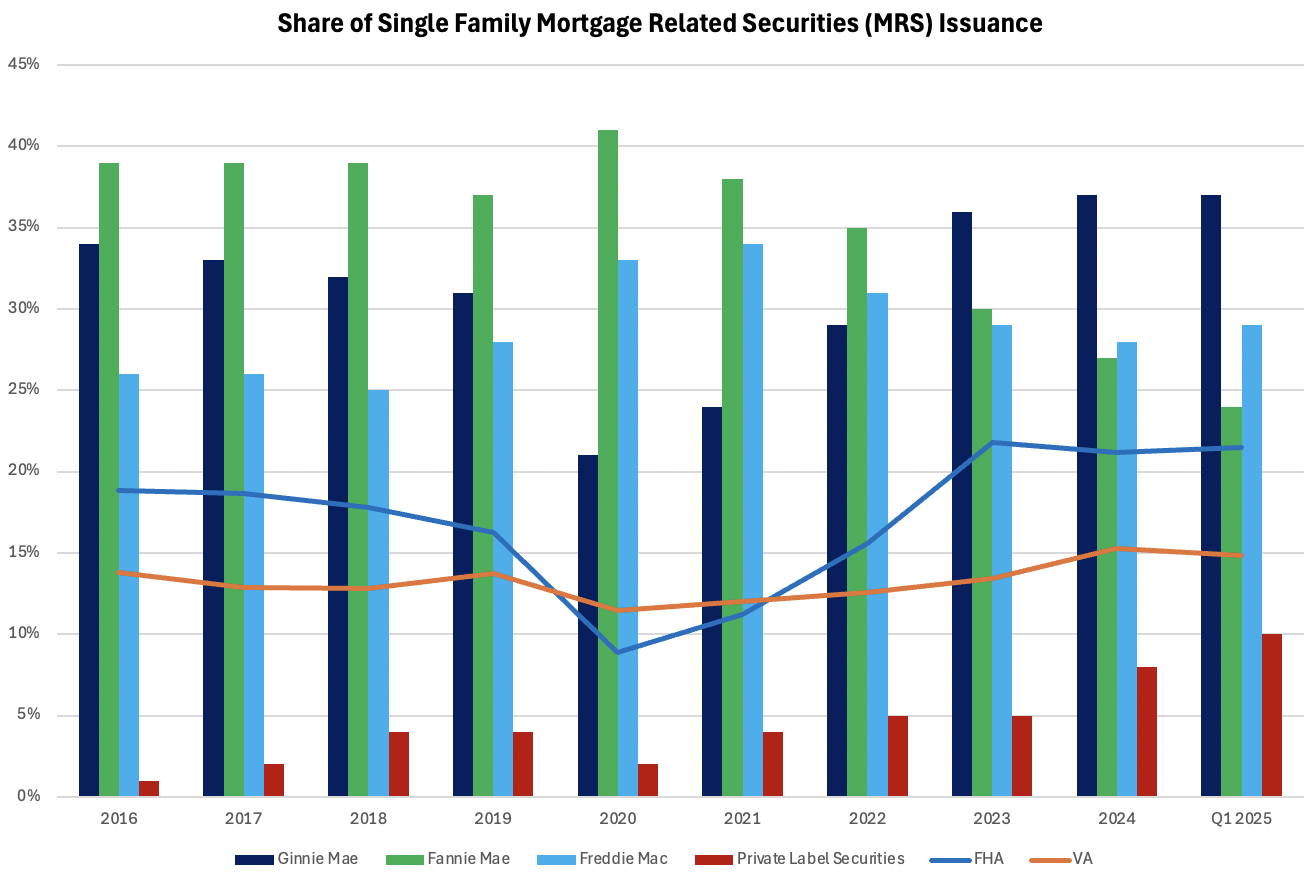

Ginnie Mae share of Mortgage Related Securities (MRS) issuance has exceeded Fannie Mae and Freddie Mac share since 2023.

- FHA share of MRS issuance is approaching Fannie Mae issuance in early 2025

- Freddie Mac share of MRS issuance has exceeded Fannie Mae share since 2024

- Private label share continues to trend up in early 2025

The first Uniform Mortgage Backed Securities (UMBS) issuance was in mid-2019 and UMBS liquidity as measured by trading volume continues to far exceed the GSE share of total agency issuance (SIFMA).

FHA+ is published monthly by Gate House Strategies, a Washington, DC area-based advisory firm focused within the financial services, mortgage lending and servicing, community development, and public housing sectors. Contact us at FHAplus@gatehousedc.com