This Issue Includes:

- Think Piece: Len Wolfson on the bipartisan housing package advancing in Congress and what comes next.

- Three Questions: Rodney Hood on AI’s role in expanding financial inclusion, the importance of model transparency and governance, and the continued strength of the U.S. financial system.

- Inside Voices: State of the Union housing signals, bipartisan manufactured housing reform efforts, debate over bank capital rules and nonbank risk of governance and liquidity, and rising calls for consistent federal AI standards in mortgage lending.

- Gate House Index:I Institutional investor ownership of single-family homes, the cost of regulations, AI in lending, bank strength, and other key housing and mortgage indicators.

THINK PIECE

The Bipartisan Housing Deal: Where Things Stand

For the March edition of our Think Piece, we’ve asked former HUD Assistant Secretary for Congressional and Intergovernmental Relations and our former colleague Len Wolfson to share his thoughts on the housing legislation working its way through Congress. With the final vote in the Senate having been delayed, we will release a supplemental with Len’s summary and thoughts if and when it passes.

If you recall, the Senate passed the "Renewing Opportunity in the American Dream (ROAD) to Housing Act of 2025" on October 9, 2025 after attaching it to the National Defense Authorization Act (NDAA). The House stripped ROAD to Housing from the NDAA when it passed that bill. On February 9, the House passed the "Housing for the 21st Century Act” (H.R. 6644). On Monday, March 2, the Senate invoked cloture on the motion to proceed with H.R. 6644 by a vote of 84-6. On Wednesday morning, March 4, the Senate passed an additional motion to proceed, 90-8-1.

Len Wolfson on the current status of negotiations:

“The Senate is on the verge of passing the bipartisanhousing package negotiated by Senators Tim Scott (R-SC) and Elizabeth Warren(D-MA). The revamped legislation, released Monday, largely reflects the text of the original Senate bill approved by the Banking Committee last summer, but ina nod to the House also incorporates several of the lower chamber's priorities, as well as the Trump administration’s recent call to restrict investorpurchases of single-family rental homes.

Moments after the legislation was released, the White House formally announced its support for the new bill. The statement of administration policy said the bill will expand housing supply and affordability while banning "large institutional investors from competing with individuals in single-family home markets.”

Over the course of the week, the Senate held two procedural votes that demonstrated overwhelming bipartisan support for the housing package. Despite those votes, the legislation has encountered headwinds, primarily owing to the newly inserted restrictions on the single-family home rental industry.

Housing groups have objected to the bill’s requirement that investors divest of newly constructed rental homes, known as build-to-rent (BTR), within 7 years, noting the President’s executive order specifically exempted investments that expand housing supply from the broader ban.

While Senators Scott and Warren continue to work with the White House to find a way to address the bill’s BTR language, Senate Majority Leader Thune has filed cloture on the housing bill and the Senate remains on track to pass it early next week.

From there, the bill will go to the House, which will be under enormous pressure to swiftly approve it and send it to President Trump’s desk.”

Look for more on what makes into a final bill in our supplemental addition of FHA+.

For your information, at the end of the Gate House Index is a very brief comparison of the ROAD to Housing Act that passed the Senate in October and the 21st Century Housing Act that passed the House in February.

THREE QUESTIONS

by Rodney Hood

Rodney E. Hood served as Acting Comptroller of the Currency from February 10, 2025, to July 15, 2025. As Acting Comptroller of the Currency, Hood was the administrator of the federal banking system and chief executive officer of the Office of the Comptroller of the Currency (OCC). The Comptroller also serves as a Director of the Federal Deposit Insurance Corporation and a member of the Financial Stability Oversight Council and the Federal Financial Institutions Examination Council. In 2019, President Trump designated Hood as Chairman of the NCUA Board, making Hood the first African American to lead a federal banking regulatory agency. While at the NCUA, he also served as a voting member of the Financial Stability Oversight Council, as the NeighborWorks America Board Chairman, and as Vice Chairman of the Federal Financial Institutions Examination Council. Before public service, Hood held senior roles in retail finance, commercial banking, affordable housing, and community development in the private sector.

Hood currently serves on several boards, including the board of the Federal Home Loan Bank of Atlanta. Through his service on the boards of a few fintech firms, Hood has focused recently on issues and implications of artificial intelligence on the financial services industry. That’s where we start the conversation.

Question: What are your thoughts on the potential value of artificial intelligence to lenders?

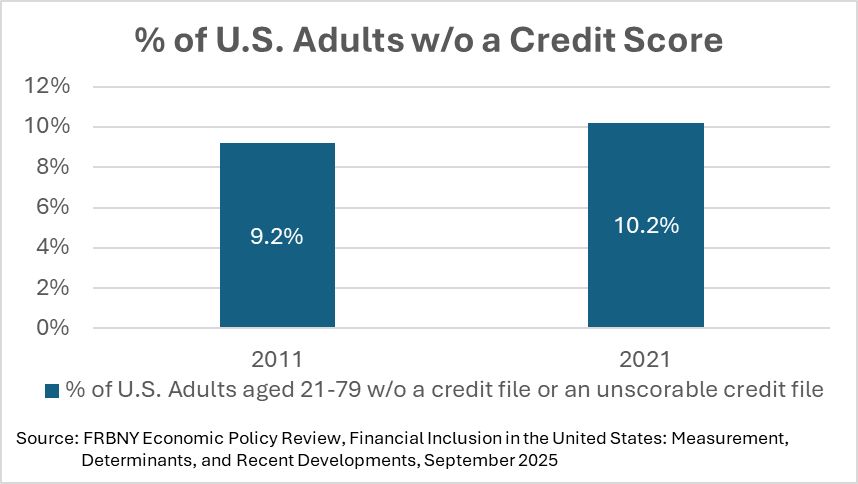

HOOD: I'm a proponent of AI and machine learning for one important reason: I believe AI will expand access to credit. And financial inclusion is the civil rights issue of our time. Forty percent of American households are unable to obtain a $400 loan for an emergency. Sixty to seventy million Americans don’t have a credit score. They are credit invisible. AI will help banks and credit unions open the credit aperture and go deeper with these folks.

Integrating these new technologies into underwriting will help us look at new methods of determining a borrower’s ability and willingness to repay a loan, without any degradation in asset or credit quality. It can be done while remaining mindful of the guardrails for safety, soundness and compliance.

Question: And then what do you see as the risks that lenders face when it comes to AI?

HOOD: The main threat is the opacity of these AI models. They are not transparent. And that creates a very human problem. Because you don’t want management simply taking an AI model and then just assuming it works without truly understanding it. AI on auto-pilot is not a strategy. Instead, you want to build explainability. That means continually learning, analyzing, testing and really scrutinizing the model. To truly understand it. Be prepared for that moment of proof when you’re being examined. You’ll want to be able to explain the model, explain the governance, the audit. Able to describe the steps taken to ensure that risks haven’t been embedded into the model.

You don’t have to become a data scientist and learn coding. But I will say that I’ve seen directors and C-suite executives get into regulatory cross hairs by not demonstrating the ability to explain the model and the governance around it. You want to be rigorous about it.

Question: The combination of your experience has put you at the intersection of banking, housing, public policy and community investment. Given your unique perspective, what do you view as the single most constant threat to the stability of the U.S. financial system?

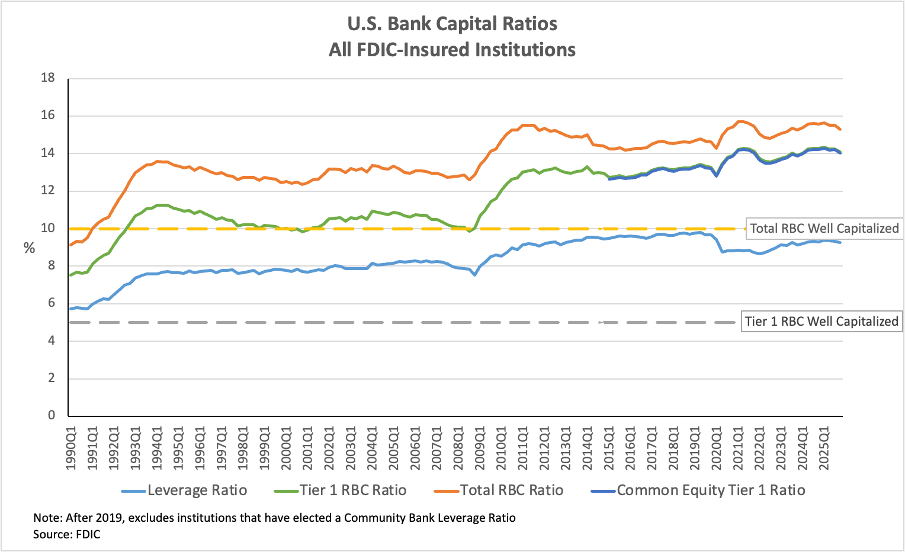

HOOD: I’ll tell you what keeps me up at night. But let me first say I believe the system has never been stronger. We're looking at capital levels that exceed statutory requirements. We see very little to risk regarding credit and asset quality. And delinquencies and foreclosure remain low. U.S. lending institutions are operating on all cylinders.

The one thing that concerns me is the possibility of complacency. Financial strength can sometimes lull institutions into thinking that they can let their guard down. The key always is to remain focused on the fundamentals. That means good sound credit underwriting, making sure we look at the borrower's ability to repay. And it means staying focused on the range of operational risk, fraud risk, and geopolitical risk. These are elements that can adversely affect the underlying strength of an institution if not actively and intelligently managed. We’re not talking about the avoidance of these risks. We never want to stifle growth. The message here is we want growth to be sustainable.

INSIDE VOICES

What we’re hearing around Washington and the industry

State of The Union:

President Trump framed housing as a kitchen-table affordability issue, with a particular focus on mortgage costs and access to homeownership. He highlighted concerns about investor purchases crowding out families, pointed to lower borrowing costs as key to improving affordability, and referenced broader economic momentum in construction and building activity. The emphasis was practical - focused on protecting homeownership (and home values), lowering interest rates, and boosting supply for families trying to buy homes.

Manufactured Housing:

Both chambers of Congress are gearing up to reshape the manufactured housing sector with bipartisan legislative proposals that would, among other things, designate HUD as the primary federal authority on manufactured housing standards and eliminate the outdated “permanent chassis” requirement which could reduce per-unit costs by up to about $10,000. Alongside this push on the Hill, HUD has just announced appointments of six new members to the Manufactured Housing Consensus Committee to advise on modernizing the HUD Code and lowering regulatory barriers. Manufactured housing currently houses roughly 22 million Americans and accounts for about 10% of new single-family home starts.

Nonbanks:

A new GAO study examines the systemic importance of nonbank mortgage companies that now dominate the housing finance system—originating and servicing roughly two-thirds of loans in the more than $9 trillion of federally guaranteed securities. The report requests that FHFA and Ginnie Mae tighten risk governance by improving validation of data, improve assessment of short-term credit exposures, and expand stress-testing scenarios.

Speaking of Nonbanks:

Fed Vice Chair Michelle Bowman recently discussed bank MSR related mortgage capital rules that are discouraging bank participation in mortgage lending - thereby limiting consumer choice and adding costs. The speech included some mention of nonbank risks relative to banks. Industry observers have since noted that nonbanks have successfully originated and serviced a majority of the mortgage market as the banks retreated. Many won’t forget the extensive forbearance offered by nonbanks during the pandemic, while abiding by prescriptive FHFA, FHA, GSE, and Ginnie Mae risk, exam and policy frameworks. Some suggest that more liquidity support for nonbanks—similar to what banks enjoy—would enhance market stability.

AI Standards:

The Colorado Artificial Intelligence Act classifies AI systems used in mortgage approvals and pricing as “high-risk,” requiring impact assessments, consumer disclosures, explanations for adverse decisions, and opportunities for human review—backed by fines of up to $20,000 per violation. While the CO safeguards promote fairness and transparency, it illustrates the difficulty of a state-by-state patchwork approach and why consistent federal AI standards are needed in mortgage lending. Current and pending state laws create uneven protections for borrowers and compliance burdens for lenders operating nationwide. The President issued an Executive Order in December of 2025 aimed at promoting U.S, leadership in AI through a "minimally burdensome national" regulatory framework that does not impede AI innovation. In addition, it establishes an AI litigation task force to challenge state laws that conflict with national policy and cited a concern with the Colorado law. In the housing finance market, federal standards are intended to provide uniform rules to prevent algorithmic discrimination while ensuring clarity and consistency.

THE GATE HOUSE INDEX

The Gate House Index and analysis is designed to provide insight into the status of FHA’s business at a moment in time and over a period of time, as well as other pertinent data points we’re following.

This month, we look at the a few data points related to large investor purchases of single-family homes as well as the cost of regulations and other home production cost factors that are the target of legislation working through Congress. We also look at recent bank capitalization and market credit characteristics, AI in mortgage lending, and access to mortgage credit by underserved communities discussed in Three Questions.

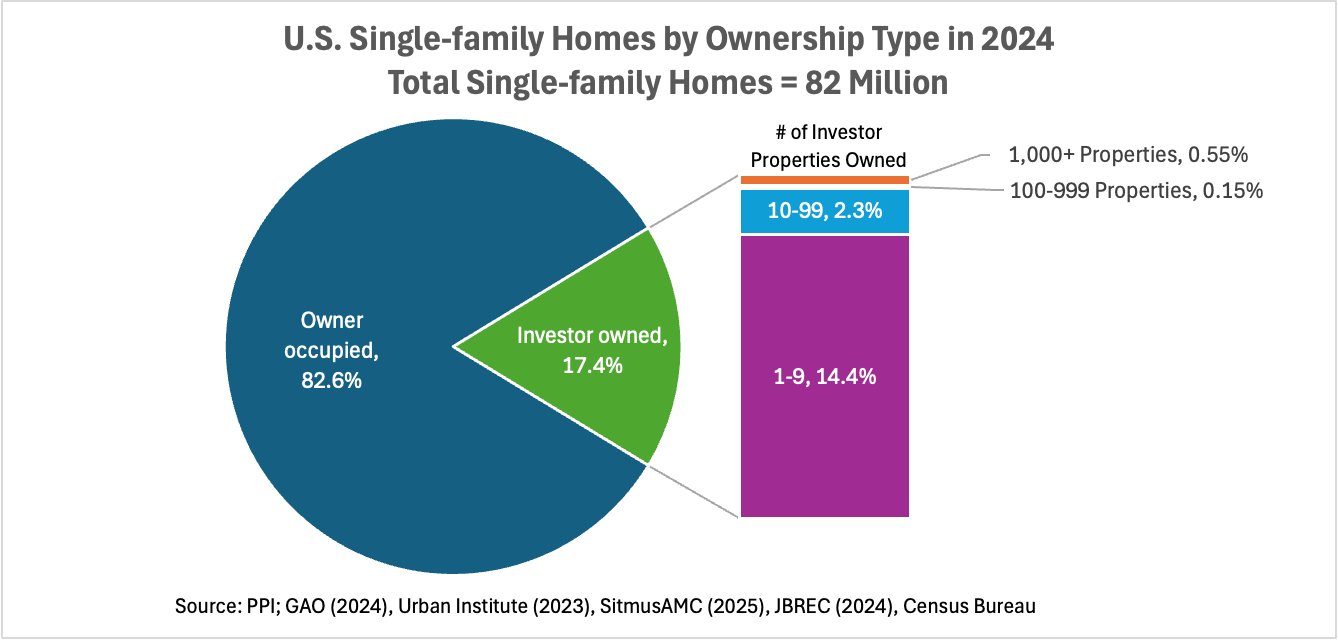

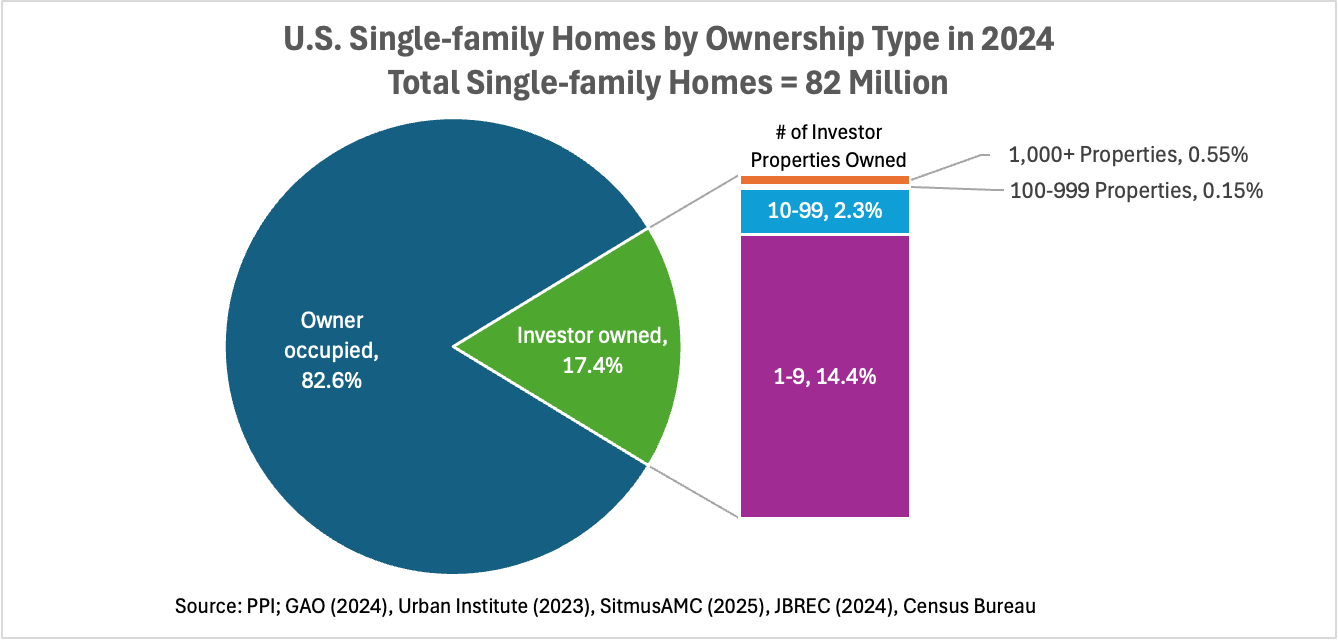

The share of single-family homes owned by investors with 10 or more properties is roughly 3%, the share with over 100 properties is less than 1%.

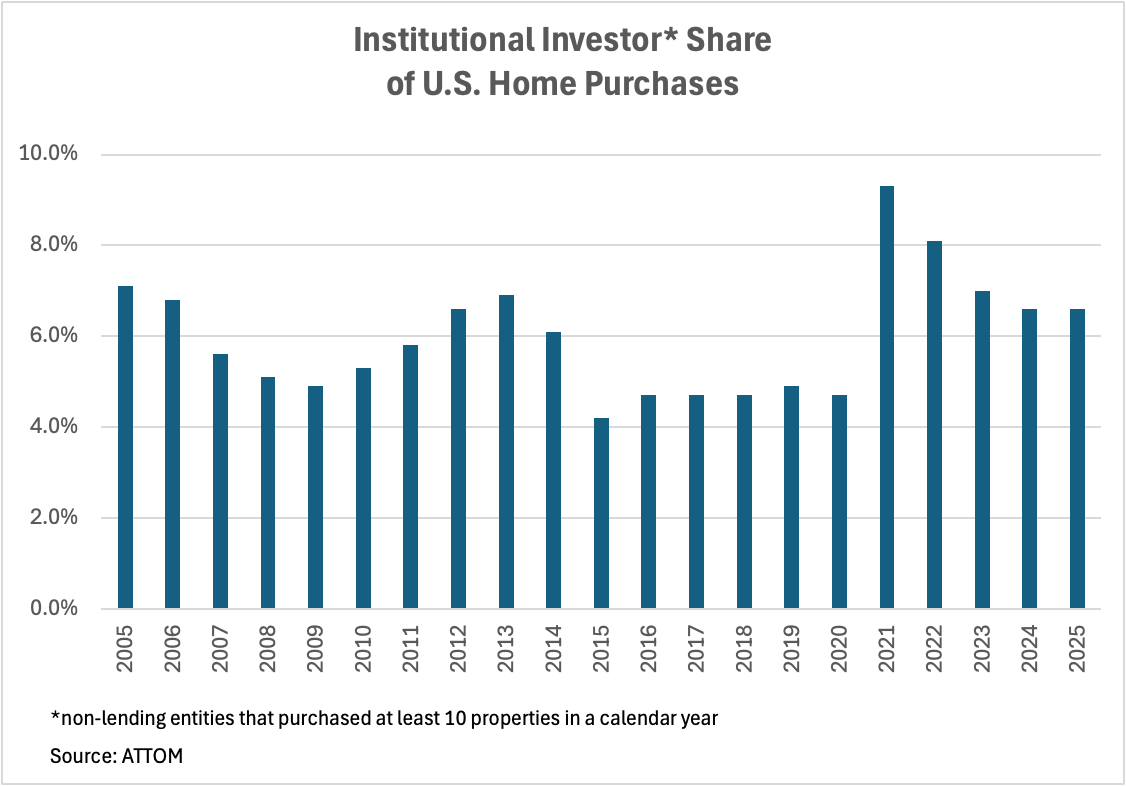

The share of institutional investor purchases peaked in 2021 when debt financing costs were extremely low, rents and home prices were rising rapidly, producing strong expected levered returns. After Fed tightening, borrowing costs went up, cap rates expanded, yields compressed, and total homes listed for sale have fallen with the existing homeowner lock-in effect.

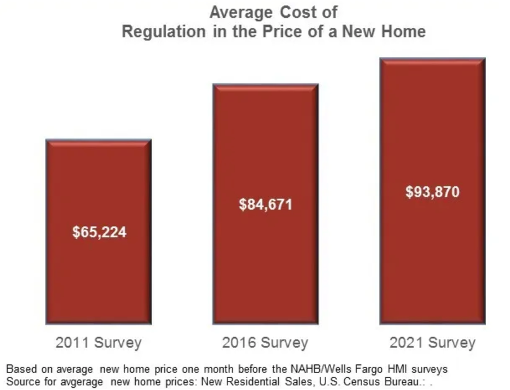

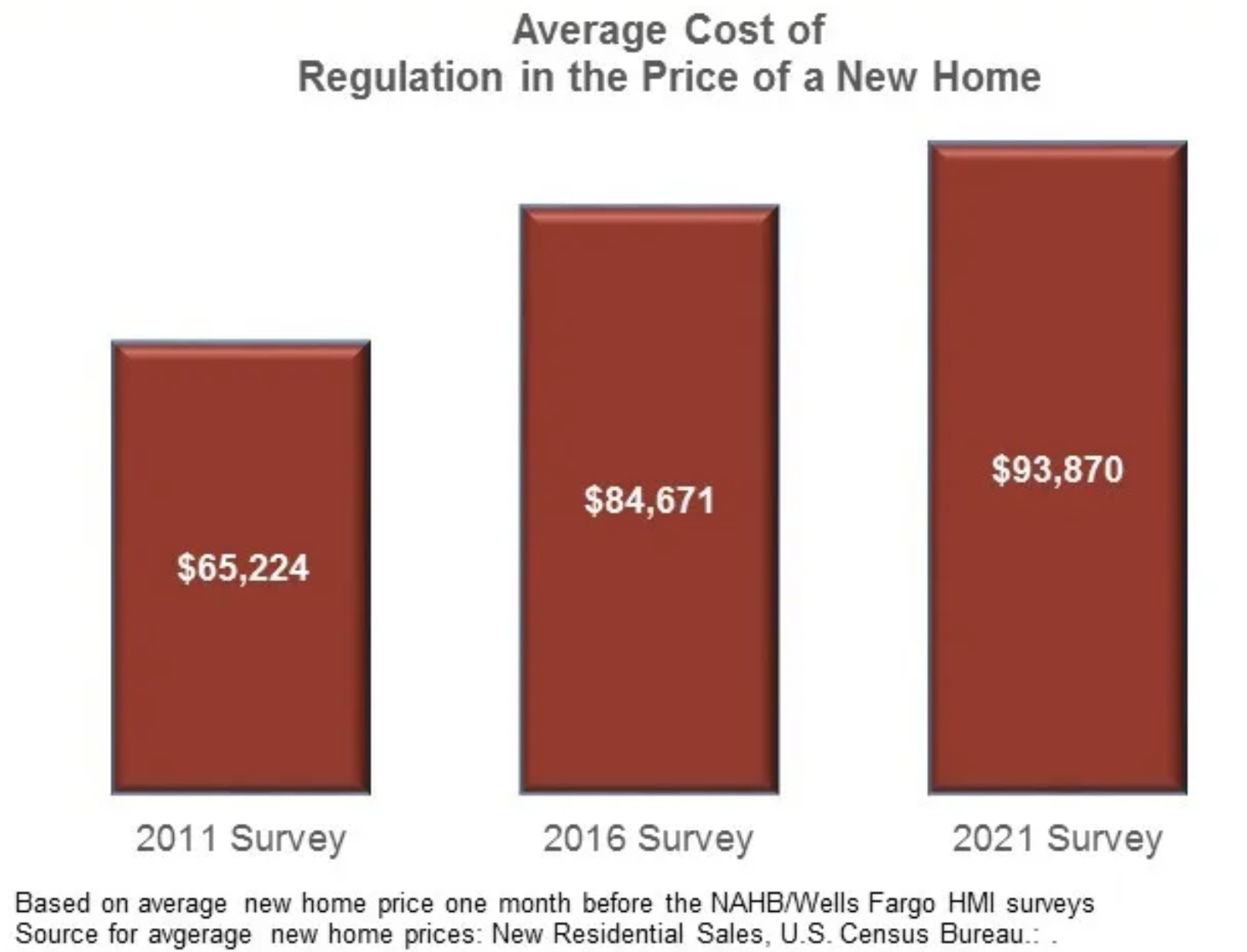

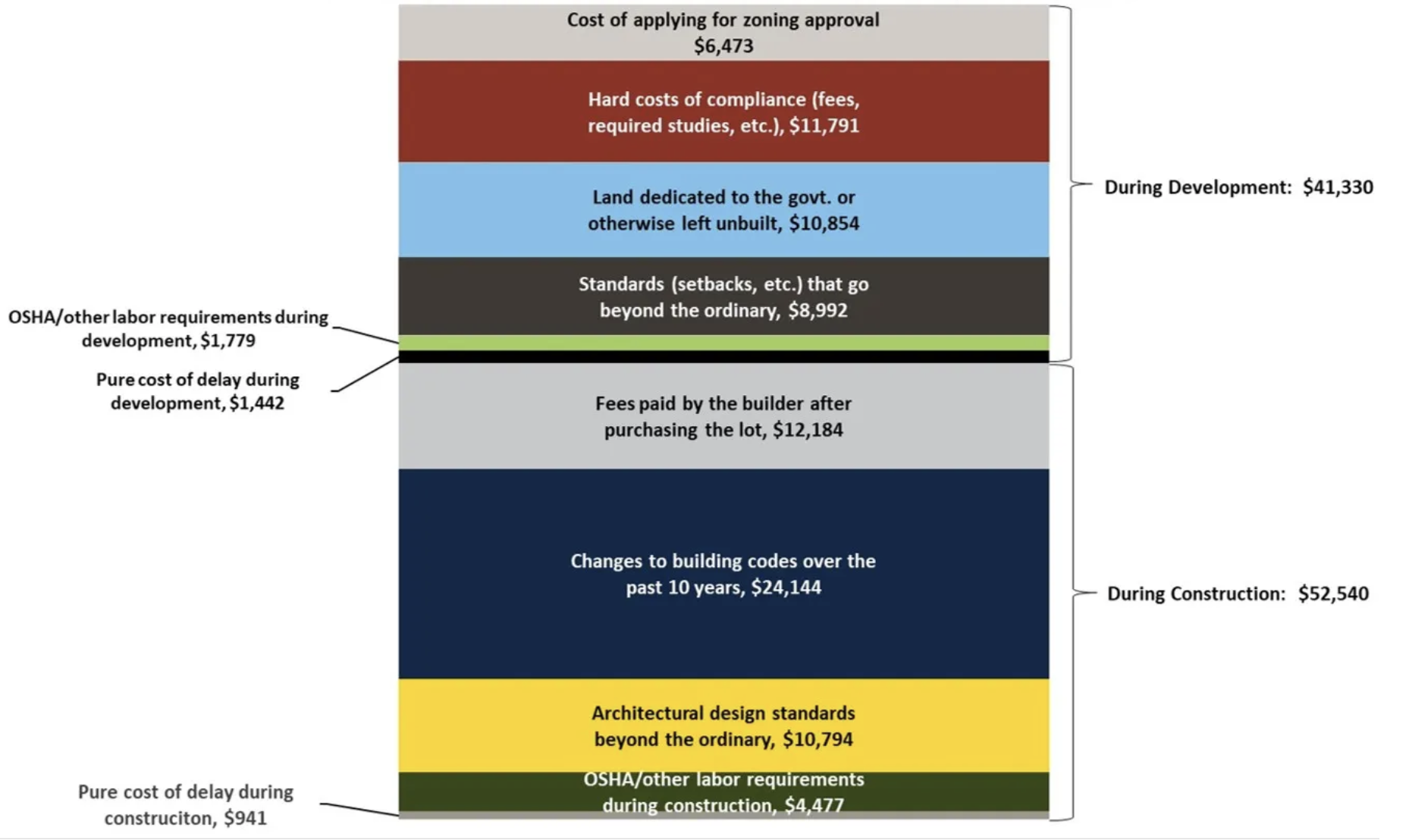

Meanwhile, one major target of the bipartisan housing legislation working through Congress is the cost of regulations in the price of a home, which is related to the cost of producing those homes. The NAHB estimates that cost to be nearly $94,000 per home, or 24% of the average new home price in 2021.

Cost of Regulation in the Price of an Average New Home in 2021 (Total = $93,870)

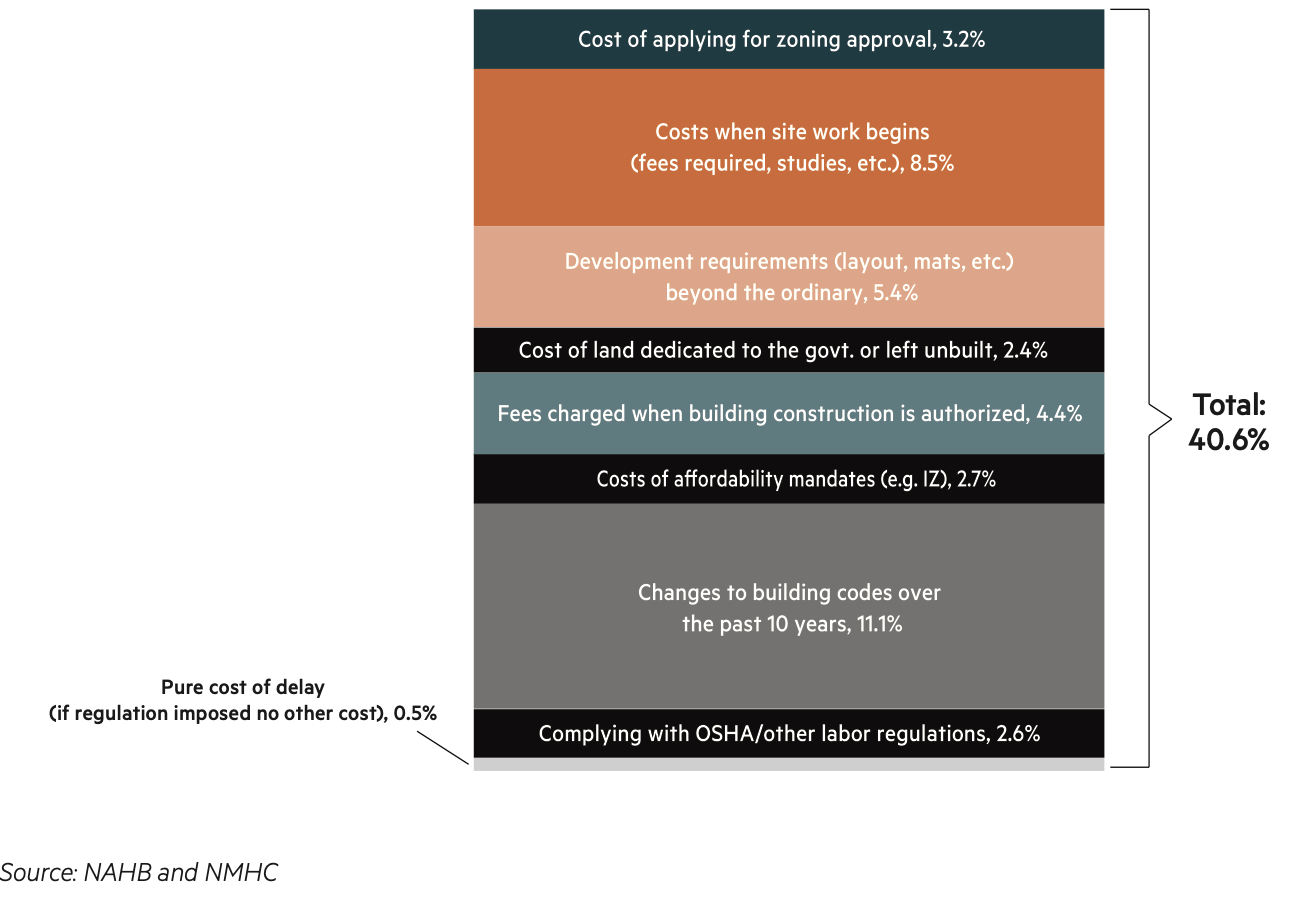

Average Cost of Regulation as a % of Total Multifamily Development Cost in 2022

Rodney Hood discusses the credit invisible and the promise of AI for access to mortgage lending in “Three Questions” above.

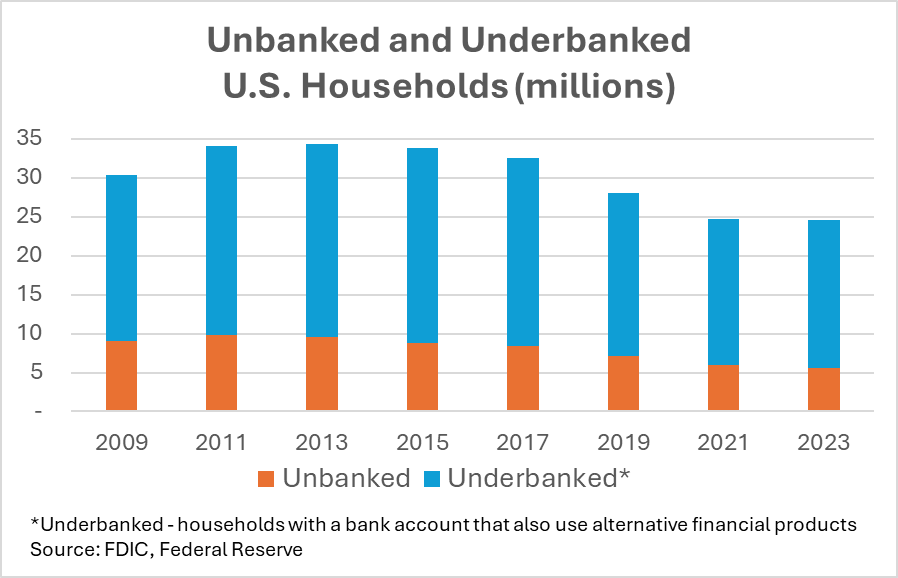

The share of American adults that are unbanked, the share that don't have a credit file, and the share with a credit file that is too thin to generate a credit score:

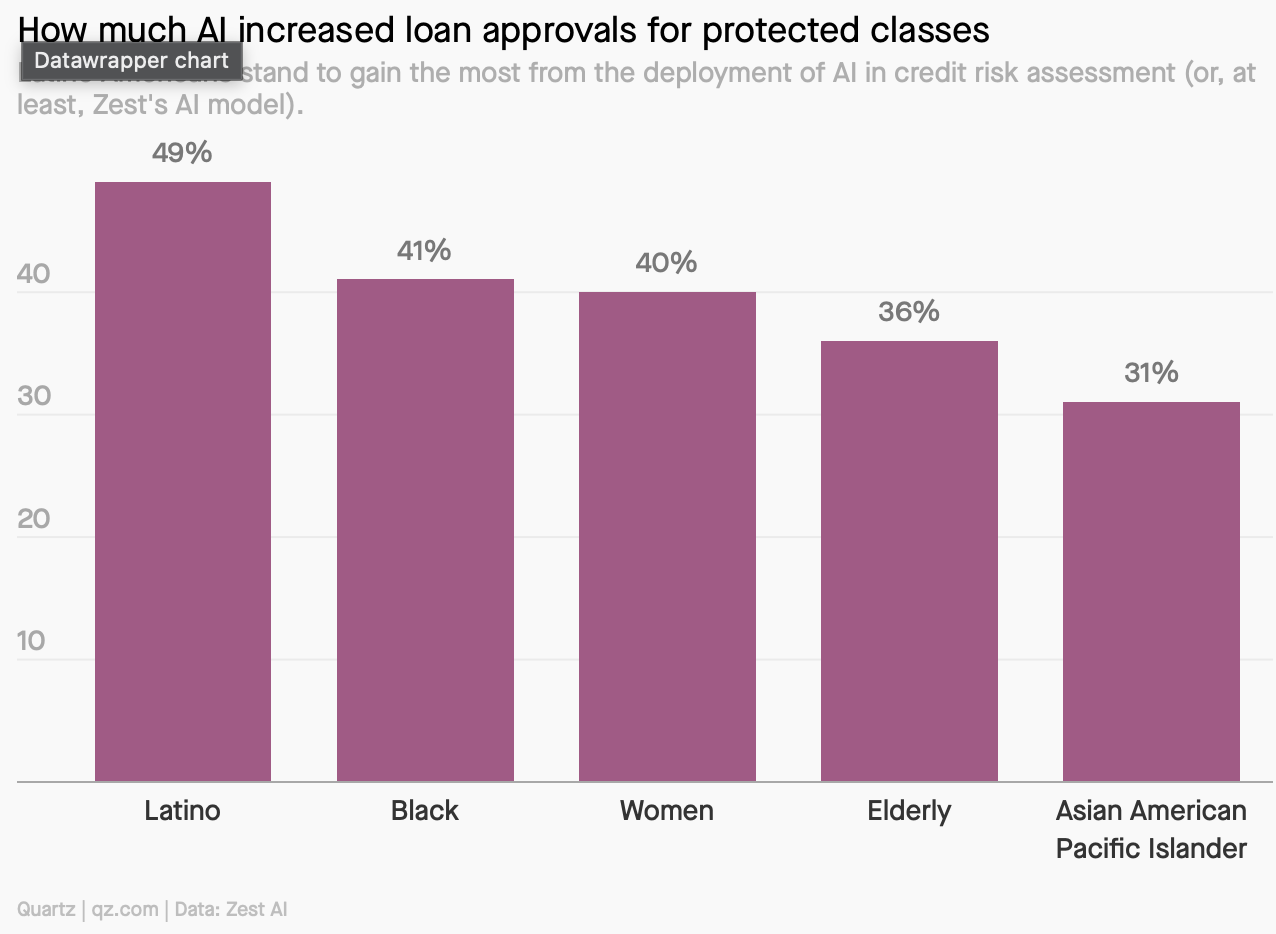

AI models have been shown to increase access to credit -- https://qz.com/ai-bank-loan-approval-zest-ai-freddic-mac-1851379970

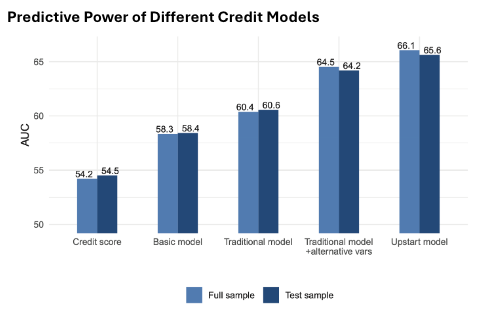

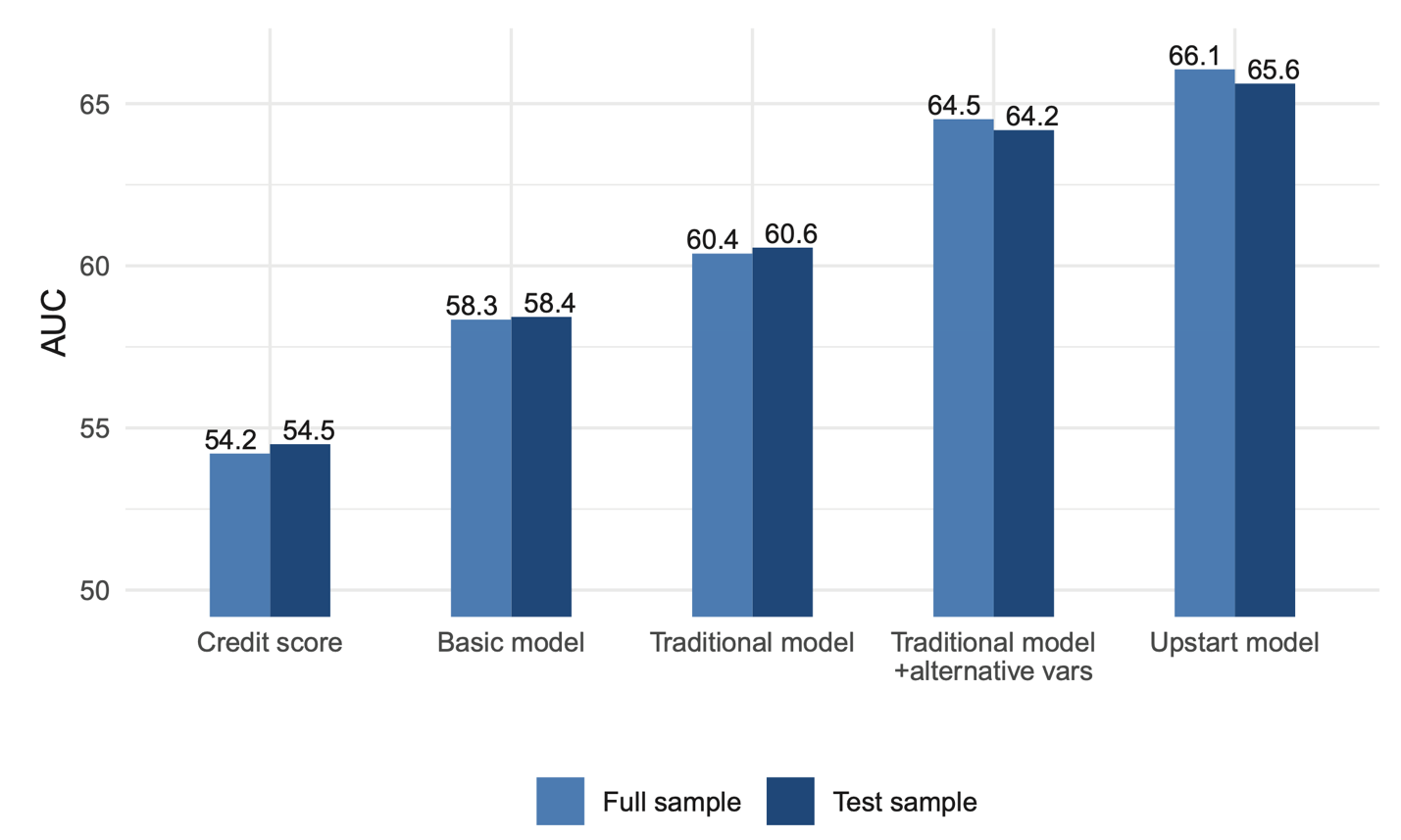

An NBER study of unsecured personal loans originated in 2019-20 found that underwriting models incorporating non-traditional data were more predictive of performance than traditional underwriting models and expanded access to credit, including for "invisible primes." https://www.nber.org/papers/w29840

According to the study: "[A]lternative data used by [the Fintech] Upstart exhibits substantially more predictive power with respect to likelihood of default; [enables] broader access to credit, particularly for borrowers with low credit scores; [and] delivers quantifiable benefits to both borrowers and lenders." This figure plots the area under the curve (AUC) for the funded Upstart sample using credit worthiness measures estimated using different models.

Predictive power of different models

Credit unions and banks are using lending technology from Zest AI to increase loan approvals by 25% while holding risk constant. “[T]he Zest AI model categorized a significant number of applicants as low risk when the standard model categorized them as high risk, ... [and] categorized borrowers as high risk when the standard model would categorize them as low risk."1

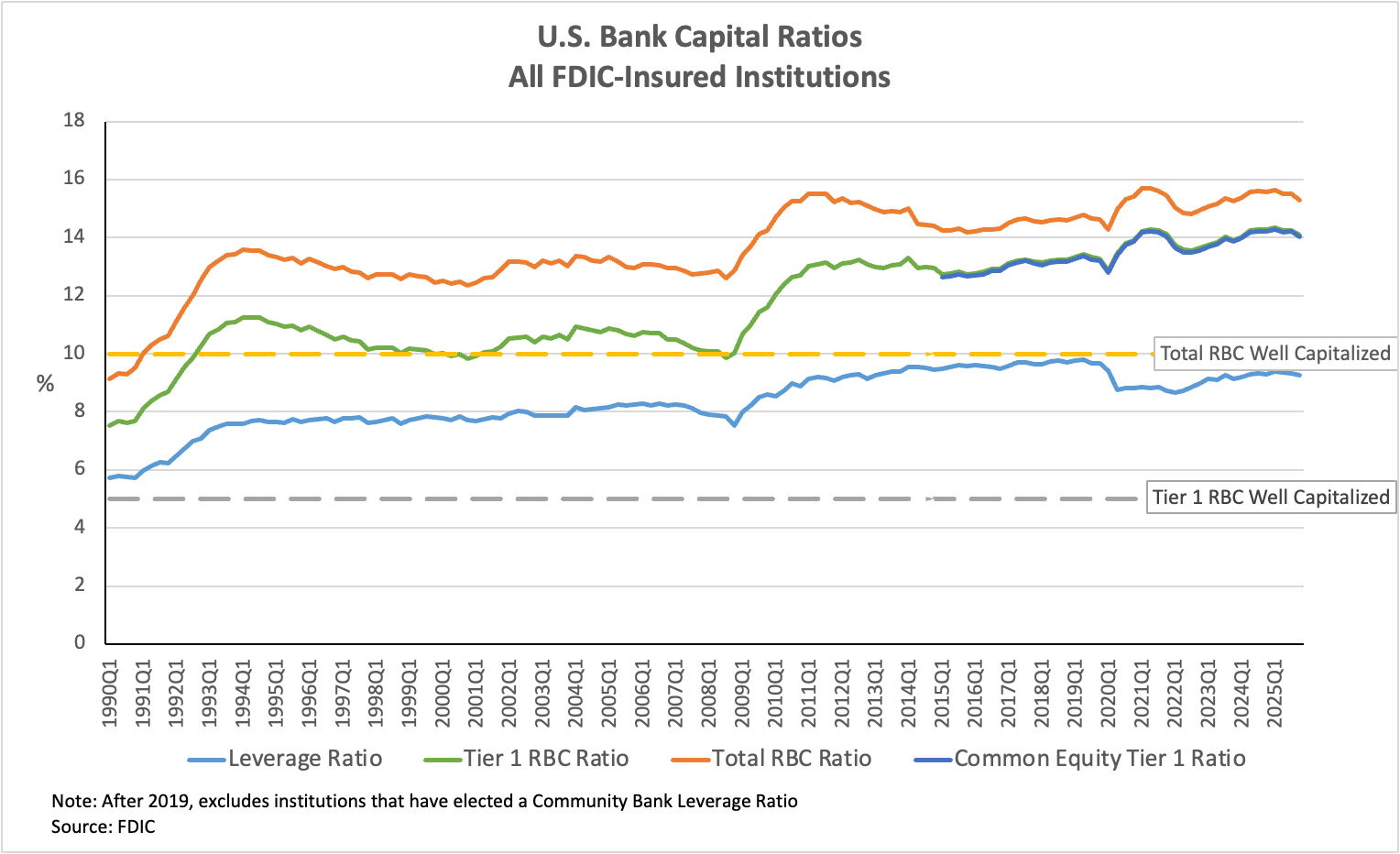

Meanwhile, Rodney Hood mentioned the health of US banks, who currently exceed capital requirements.

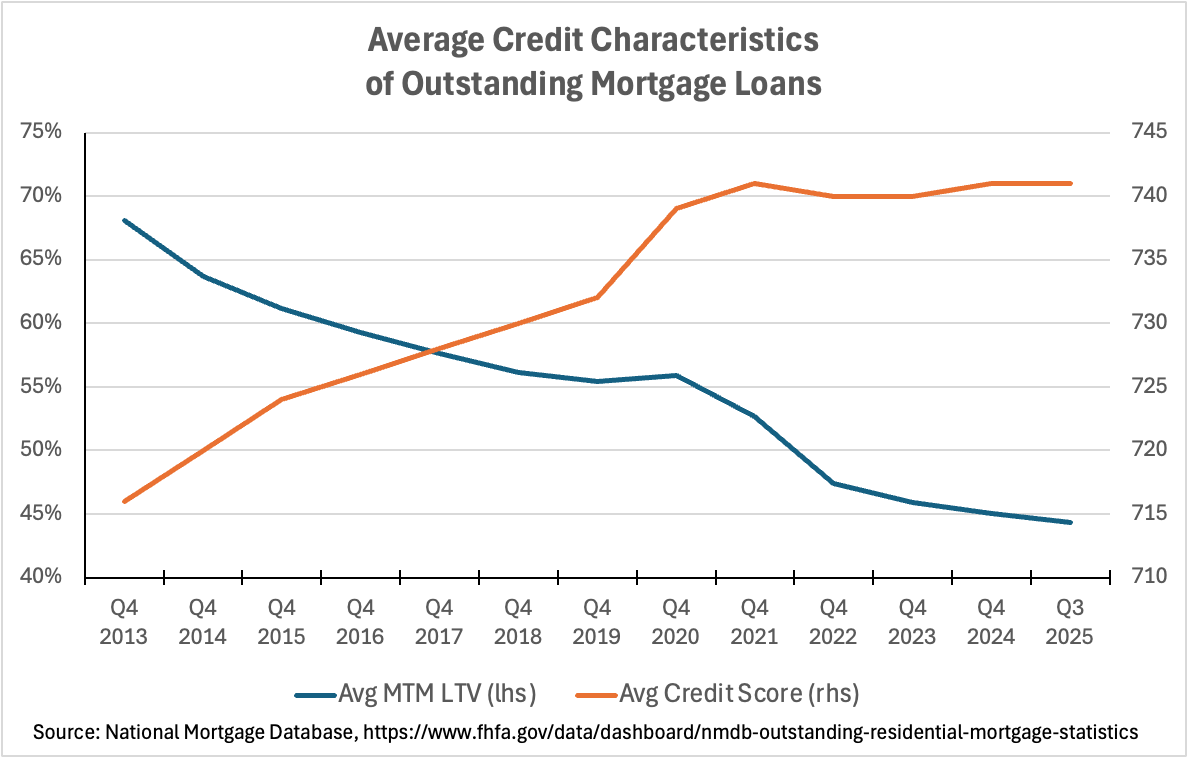

Morever, for all mortgage loans outstanding in the NMDB, the average mark-to-market LTV has trended down for more than a decade to a record low and the average credit score has trended up to a near record high in Q3 2025, the most recent period reported.

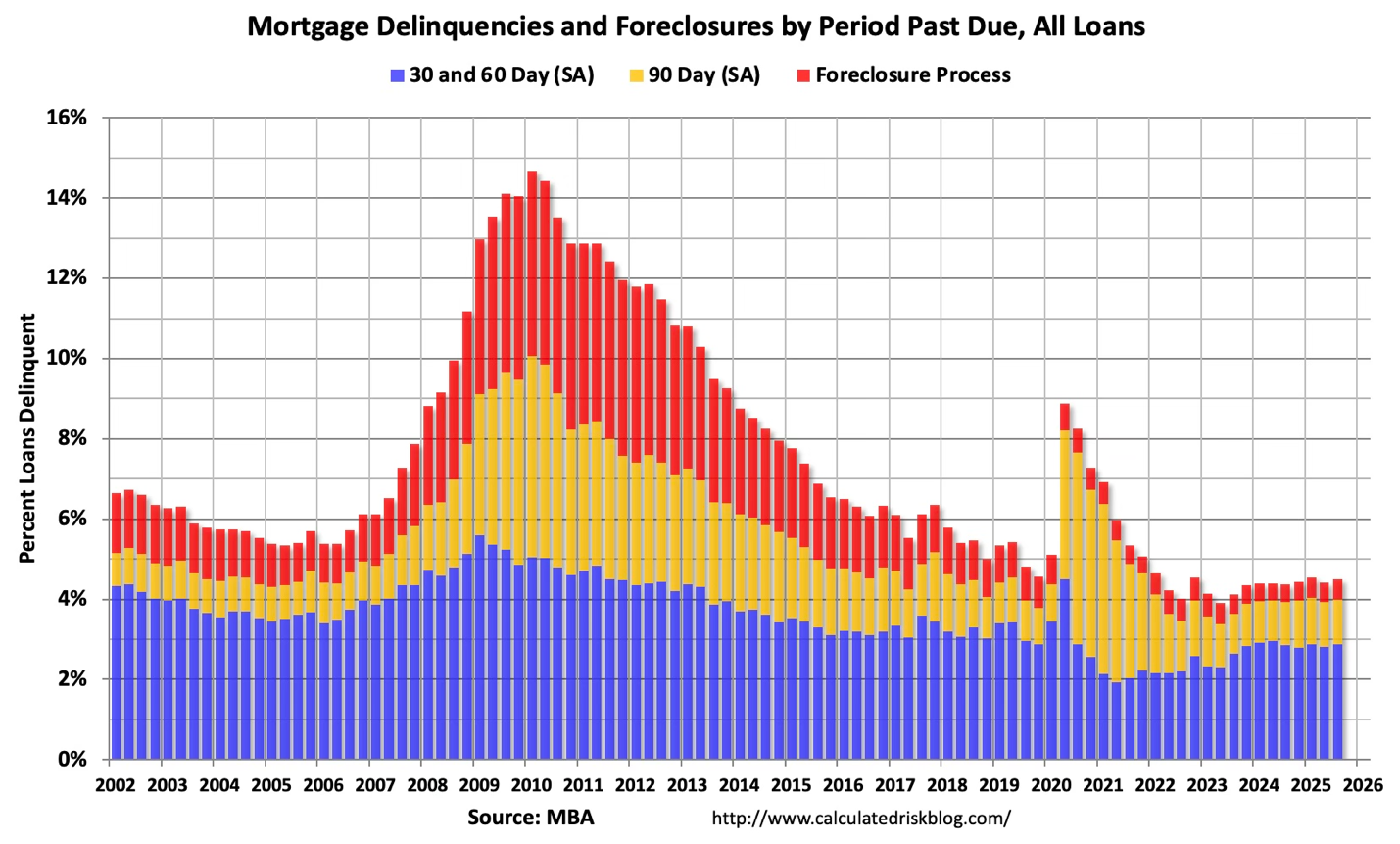

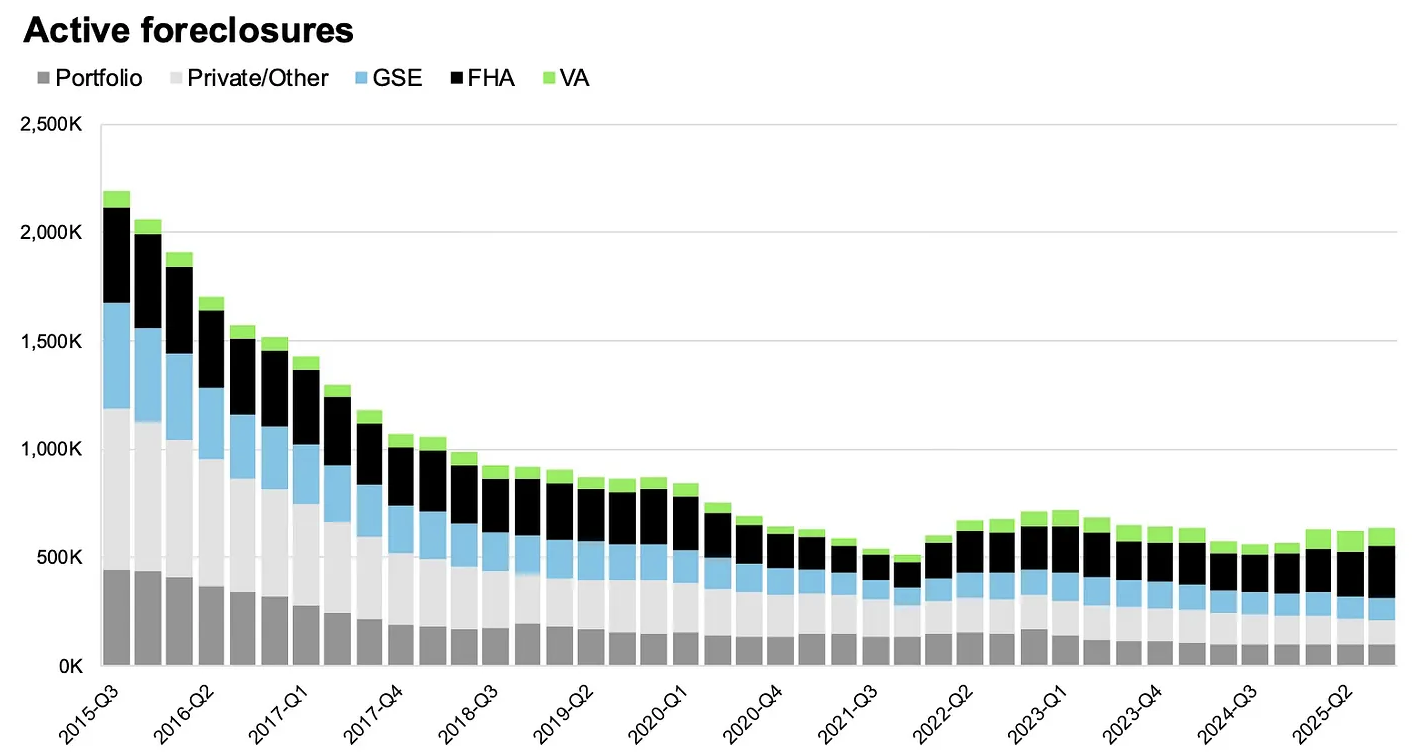

And mortgage delinquencies and active foreclosures remain low; below pre-pandemic levels:

Below is a very brief comparison of the ROAD to Housing Act that passed the Senate in October and the 21st Century Housing Act that passed the House in February.

This Month In History

On March 13, 2008, Bear Stearns notified the Federal Reserve that it faced an immediate liquidity shortfall, driven by a collapse in repo funding and mounting losses tied to mortgage-backed securities, and would be unable to meet its financial obligations the following day. The FRBNY authorized a $12.9 billion emergency loan to JPMorgan Chase, which advanced the funds to Bear. On March 16, Bear agreed to be acquired by JPMorgan for $2 per share (later increased to $10), down from a 52-week high of approximately $133, marking the first major institutional failure of the 2008 financial crisis.

FHA+ is published monthly by Gate House Strategies, a Washington, DC area-based advisory firm focused within the financial services, mortgage lending and servicing, community development, and public housing sectors. Contact us at FHAplus@gatehousedc.com