This Issue Includes:

- Think Piece: Michael Marshall on AI’s rapid transformation of mortgage finance, the risks of bias and fraud, and the growing need for a clear federal regulatory framework.

- Three Questions: Keith Becker on rising homeowners’ insurance costs, the tradeoffs of new GSE policy shifts, and the broader implications for affordability, risk, and credit access.

- Inside Voices: A sweeping housing executive order, bipartisan legislation nearing the finish line, expanding HUD responsibilities, insurance policy shifts, and the growing impact of student debt on homeownership.

- Gate House Index: Rising insurance costs, credit loss dynamics, AI adoption trends, and the growing gap between AI investment and real-world implementation in mortgage finance.

THINK PIECE

AI Regulation in Mortgage Finance: Navigating Risk and Fragmentation

Artificial intelligence is rapidly reshaping mortgage finance, offering opportunities in scale and scope that are generational. Innovative lenders and servicers are currently leveraging the technology to augment myriad roles, shedding costly, error-prone manual tasks, deploying exception-based workflows, and performing quality control and compliance checks as they move toward predictive, proactive customer engagement, origination, servicing, and risk analysis.

While many current AI deployments manage discrete tasks, greater gains can come from re-architecting end-to-end processes, ultimately enabling AI systems to orchestrate the entire loan lifecycle.

For those who embrace the moment, the potential to capture value is tangible. For those able and willing to make significant investment -- imbedding AI organically (ironically) into the firm operating model – the returns are more than promising, perhaps exponential.

The eventual (inevitable) AI-mediated mortgage process will ultimately mean AI identifies borrowers, customizes product offerings, performs a first-pass decision, and fulfills origination and closing while humans manage exceptions and critical decisions in a continuous learning environment. In theory, AI improves consumer access, service, and outcomes.

It sounds pretty good, but what are the obstacles in this traditionally staid, heavily regulated, and paper-weighted industry that stand in the way? How do we navigate the new generation of risks all of this advancement introduces?

At the core are elevated concerns around data integrity and unintended bias. Data quality is essential to initial decision-making and reinforcement learning. Ill-constructed AI models learning from historical mortgage data may embed prior inferior underwriting practices, and potentially structural inequities and proxy variables.

The reputational and financial risk of replicating or amplifying bias are real and can be substantial. In 2019, Facebook paid a civil penalty over alleged discriminatory housing ad practices and agreed to overhaul its ad algorithms in 2022 to address Fair Housing Act concerns. In 2024, SafeRent Solutions reached a $2.3 million settlement a in a class-action lawsuit alleging its AI scoring tool disproportionately penalized federal Section 8 voucher users and minority renters. In March of this year, a federal judge allowed the 2023 lawsuit against WorkDay, alleging AI-driven age discrimination in hiring, to move forward as a potential class action.

Meanwhile, generative AI amplifies threats tied to fraud and cybersecurity. Mortgage lenders and settlement agents have reported increases in wire fraud schemes where criminals use AI-generated emails or voice cloning to impersonate trusted parties at closing. In other cases, bad actors have leveraged deepfake technology to pose as borrowers or real estate professionals, undermining identity verification processes. These developments are not hypothetical—they are actively reshaping risk management priorities across the housing finance ecosystem.

As political and regulatory attention has intensified, federal housing and banking regulators—including Federal Housing Finance Agency (FHFA), Office of the Comptroller of the Currency (OCC), and Federal Deposit Insurance Corporation (FDIC)—have issued guidance emphasizing model risk management, third-party oversight, and fair lending compliance. State leaders and federal policymakers alike are raising concerns about consumer protection, fairness, and systemic risk. High-profile statements and legislative pushes—including those from officials like Florida Governor Ron DeSantis—underscore a growing sense that AI must be governed before its risks outpace existing safeguards. However, much of the current guidance is principles-based, signaling that standards are in flux rather than fully defined.

The recent directive from Freddie Mac requiring an enterprise-wide AI governance framework – origination, underwriting, servicing -- and the Presidential Executive Order on AI – which seeks to enforce a national framework -- feel like an inflection point: AI is expected to be embedded in mortgage operations—but, importantly, within a framework of accountability, explainability, and control.

But there is work to be done yet to get past the fragmentation: In 2024 alone, more than 100 AI-related laws were enacted across the United States, reflecting a wide range of approaches. Comprehensive frameworks like the Colorado AI Act (SB 24-205) impose obligations on “high-risk” AI systems to prevent algorithmic discrimination, while laws such as the Texas Responsible AI Governance Act take an intent-based approach to prohibiting harmful uses. Other states, including Utah and California, have focused on transparency, disclosure, and consumer interaction requirements, while sector-specific rules address employment practices, healthcare communications, and even political deepfakes.

The Presidential EO promises to sue states whose regulatory regimes are out of sync with a national AI framework. A well-designed federal framework could, in theory, strike a balance—mitigating risks such as bias and fraud while avoiding overly prescriptive rules that stifle innovation. It could also provide much-needed consistency across markets, particularly in sectors like mortgage finance that depend on national scale and standardized processes.

While these efforts demonstrate meaningful progress, they also highlight the growing challenge. Mortgage lenders and servicers operating nationally must navigate a patchwork of inconsistent—and sometimes conflicting—state requirements. In some cases, widely used underwriting tools supported by the GSEs may be subject to state-level standards that were not designed with these systems in mind, creating compliance ambiguity or even impractical expectations. For management teams, this translates into a costly and complex compliance burden, with heightened legal and operational risk.

As AI continues to evolve and advance—and as both risks and opportunities expand—compliance becomes increasingly urgent and lends itself toward a cohesive federal standard that provides the clarity and balance that the current patchwork of state laws cannot.

Look for more on what makes into a final bill in our supplemental addition of FHA+.

THREE QUESTIONS

by Keith Becker

Keith is President/CEO and Founding Partner of Gate House Strategies, LLC, a Washington, DC-based advisory firm serving the financial services, mortgage, community development, and public housing sectors. Before founding Gate House, he served as Deputy Assistant Secretary and Chief Risk Officer at FHA, where he oversaw risk governance for the agency's $1.3 trillion mortgage insurance portfolio. He previously spent 26 years at Freddie Mac, concluding as Vice President and Chief Credit Officer in their Single Family division. Keith holds degrees in Economics and Business from the University of Pittsburgh and completed an advanced risk management program at the Wharton School.

Question: FHFA announced on March 18 that Fannie Mae and Freddie Mac will update property insurance requirements to allow actual cash value (ACV) coverage for roofs on single family (1–4 unit) homes. How should this change be viewed in the context of rising insurance costs, and should the Federal Housing Administration (FHA) consider a similar approach?

BECKER: The FHFA announcement reflects mounting pressure from sharply rising homeowners insurance costs—up roughly 70% since 2019—which, alongside higher property taxes, is straining housing affordability. By allowing Fannie Mae and Freddie Mac to accept actual cash value (ACV) coverage for roofs on 1–4 unit homes, FHFA is signaling a willingness to introduce flexibility that can reduce insurance premiums and help borrowers qualify for or sustain homeownership, particularly in high-cost insurance markets.

Viewed in this context, the change is a pragmatic response to affordability challenges. Lower premiums can modestly reduce monthly housing costs, potentially improving loan eligibility and borrower resilience at the margin. For some households, especially in disaster-prone or high-premium regions, this flexibility could be the difference between qualifying for a mortgage or not.

However, changing the replacement cost value (RCV) coverage requirement to an ACV requirement comes with meaningful tradeoffs. Because ACV accounts for depreciation, payouts after a loss may fall short of the full cost to replace a roof. This creates added financial exposure for homeowners—particularly those with older roofs—who may need to cover significant out-of-pocket costs after damage. In turn, this could elevate risks of deferred maintenance, property deterioration, or even default in severe cases.

For FHA, the decision is more complex. FHA borrowers typically have fewer financial reserves and are more vulnerable to unexpected expenses. Allowing ACV coverage in this segment could amplify financial stress following a loss event, potentially conflicting with FHA’s mission to support sustainable homeownership among higher-risk borrowers.

In sum, FHFA’s move can be seen as a targeted affordability measure with clear benefits but notable risks. Whether FHA should adopt a similar approach depends on balancing premium relief against borrower protection. FHA may be more cautious or consider a more limited or conditional version of the policy, given the vulnerability of its borrower base.

Question: Do you see any likelihood that some kind of a federal backstop or guaranty for homeowners’ insurance ever becomes reality?

BECKER: Well, that’s a topic that’s been discussed back and forth for a very long time. Of course, it’s good to have thoughtful conversations about ideas to reduce the cost of insurance. The U.S government already acts as a backstop for terrorism insurance and flood insurance, so precedent exists for government intervention. And it is possible the government could play a role here but I think only in background, not as the primary insurer.

However, before shifting catastrophic risk to the federal government, I do think it’s feasible for the industry to consider non-governmental alternative structures that better socialize at least the catastrophic risk, if not risk beyond a basic policy limit, across a group of reinsurers. That would be like the credit risk transfer activities of the GSEs. The federal government should not always be viewed as the backstop for catastrophic risk as it creates a moral hazard. And the capital markets are more efficient at establishing and managing a structure like this.

Question: What are the pros or cons of only permitting GSEs to recover unpaid principal balance (UPB) at default, not the associated legal fees, foreclosure costs or accrued interest?

BECKER: Limiting GSE recoveries to only the UPB at default, while excluding legal fees, foreclosure costs, and accrued interest, would significantly alter the mortgage servicing and risk landscape. This approach would reduce borrower financial burdens during foreclosure but could increase overall system costs and reduce credit availability. The outcome would likely be an increase in the guaranty fees (or MIPs for FHA) to offset the increased cost Fannie and Freddie would have to bear. They could also tighten their respective credit boxes to reduce the likelihood of loan default. That would reduce consumer access to credit. And for borrowers, knowing their liability is capped at the UPB creates the possibility of increasing strategic default risk. These would all be major disruptors to the efficient operations of the U.S. mortgage market.

INSIDE VOICES

What we’re hearing around Washington and the industry

Executive Order: President Donald Trump’s March 2026 executive order on housing takes a broad aim at affordability by cutting federal regulatory barriers—particularly for community banks—revamping Consumer Financial Protection Bureau disclosure rules, recalibrating supervision standards, and accelerating permitting to boost housing supply. The directive also directs agencies to expand access to mortgage credit, modernize appraisals, and encourage state and local zoning reforms, underscoring a supply-side strategy to lower costs. Many of the ultimate impacts will hinge on agency implementation and local adoption. “The order is far-reaching, with the potential for significant impacts in the months and years ahead,” said Brian Montgomery, Co-Founder and Chair of Gate House Strategies.

Housing: Two bipartisan housing packages have cleared major hurdles in Congress. The Housing for the 21st Century Act passed in the House overwhelmingly by a vote of 390-9 and the 21st Century ROAD to Housing Act passed in the Senate by an 89–10 margin. We now move to the messy endgame typical of big-ticket housing legislation. The bill must be reconciled across chambers, where differences over provisions like limits on institutional investors, regulatory scope, and the absence of new spending are slowing final passage despite broad support. The delay isn’t about momentum, rather it’s about alignment: leadership is threading the needle between conservative concerns over federal overreach and progressive pushes for stronger affordability tools, while also navigating legislative bandwidth and competing priorities. Next steps center on House reconsideration of the Senate-amended package or a conference process to agree on a final bill to deliver to the President’s desk in the coming months.

HUD Impacts: For HUD, the expected housing law will be less about new funding and more about a quiet but meaningful expansion of the HUD operational footprint. It will lean heavily on the Department to administer new grant programs, recalibrate existing tools like HOME and CDBG, and take the lead on manufactured and modular housing standards, which effectively positions HUD as the central driver of federal housing supply policy. An expected challenge will be to manage capacity and execution risk: HUD is being handed broader authority such as more waivers, more flexibility, and more program design, but without a commensurate increase in resources, while also being asked to coordinate with local governments that retain zoning control.

FHFA Insurance Directive: The March 18 directive to Fannie Mae and Freddie Mac effectively reversed course on a contentious insurance standard—allowing actual cash value (ACV) coverage for roofs in lieu of full replacement cost value (RCV). The shift is attempts to address the surge in property insurance costs and availability constraints that had begun sidelining borrowers and stalling transactions. If implemented the premium itself may decrease, but the potential out-of-pocket expense for homeowners in the event of a total roof loss will be significantly higher than under a traditional RCV policy. It’s not clear how many homeowners will adopt this approach and whether lenders/servicers will permit it or require homeowners to maintain RCV.

Student Loan Debt: Now exceeding $1.7 trillion nationwide—continues to weigh on mortgage affordability, with the average borrower carrying roughly $30,000–$40,000 in balances. Monthly payments can add $200–$400+ to debt-to-income ratios, often pushing borrowers above qualifying thresholds or reducing purchasing power by tens of thousands of dollars. The result: fewer first-time buyers able to enter the market, median age of 1st time homebuyers rising to 40, and a measurable drag on homeownership rates among younger house.

THE GATE HOUSE INDEX

The Gate House Index and analysis is designed to provide insight into the status of FHA’s business at a moment in time and over a period of time, as well as other pertinent data points we’re following.

This month, we look at the a few data points related to homeowner’s insurance and the use of AI in the mortgage industry.

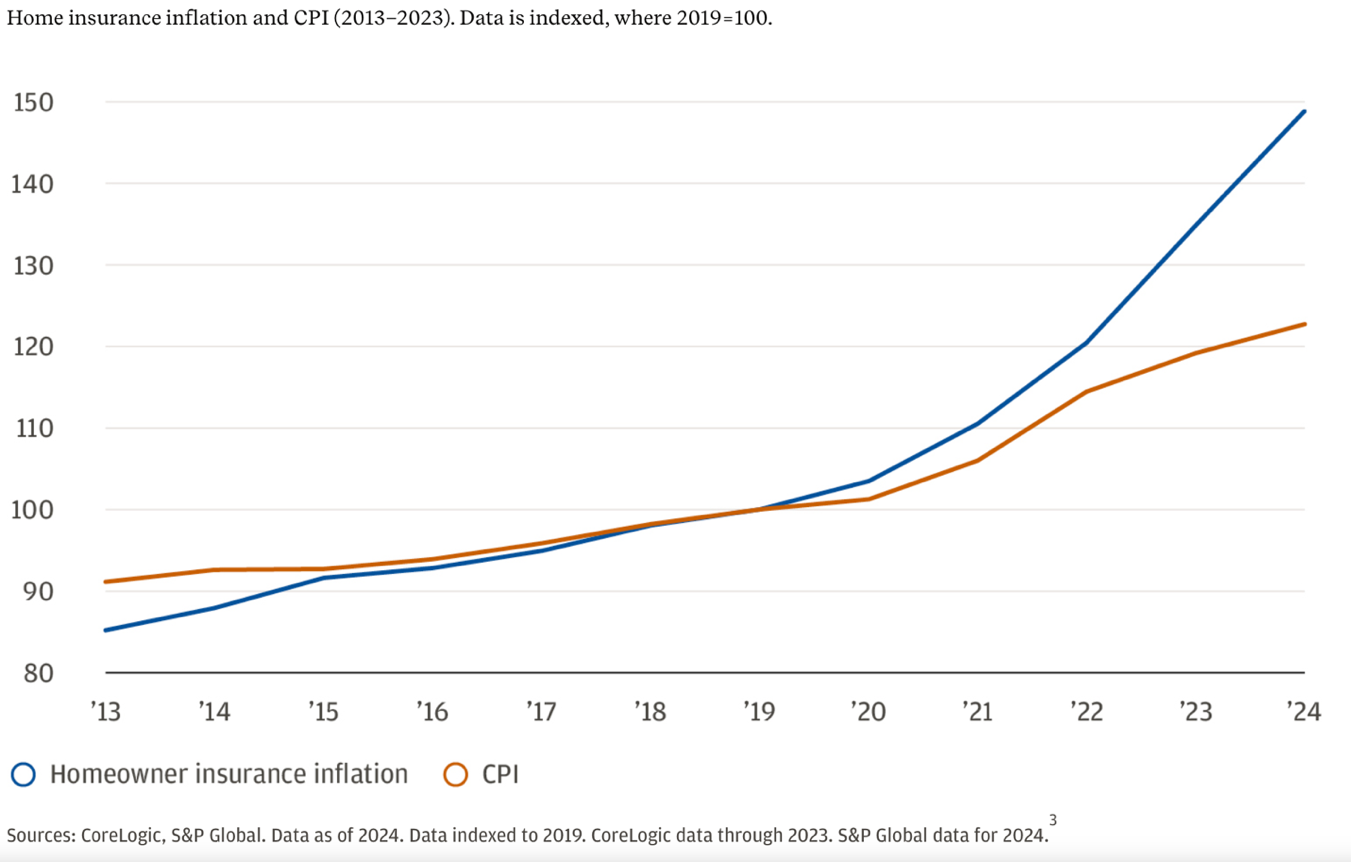

Homeowners' insurance premiums continue to rise faster than inflation:

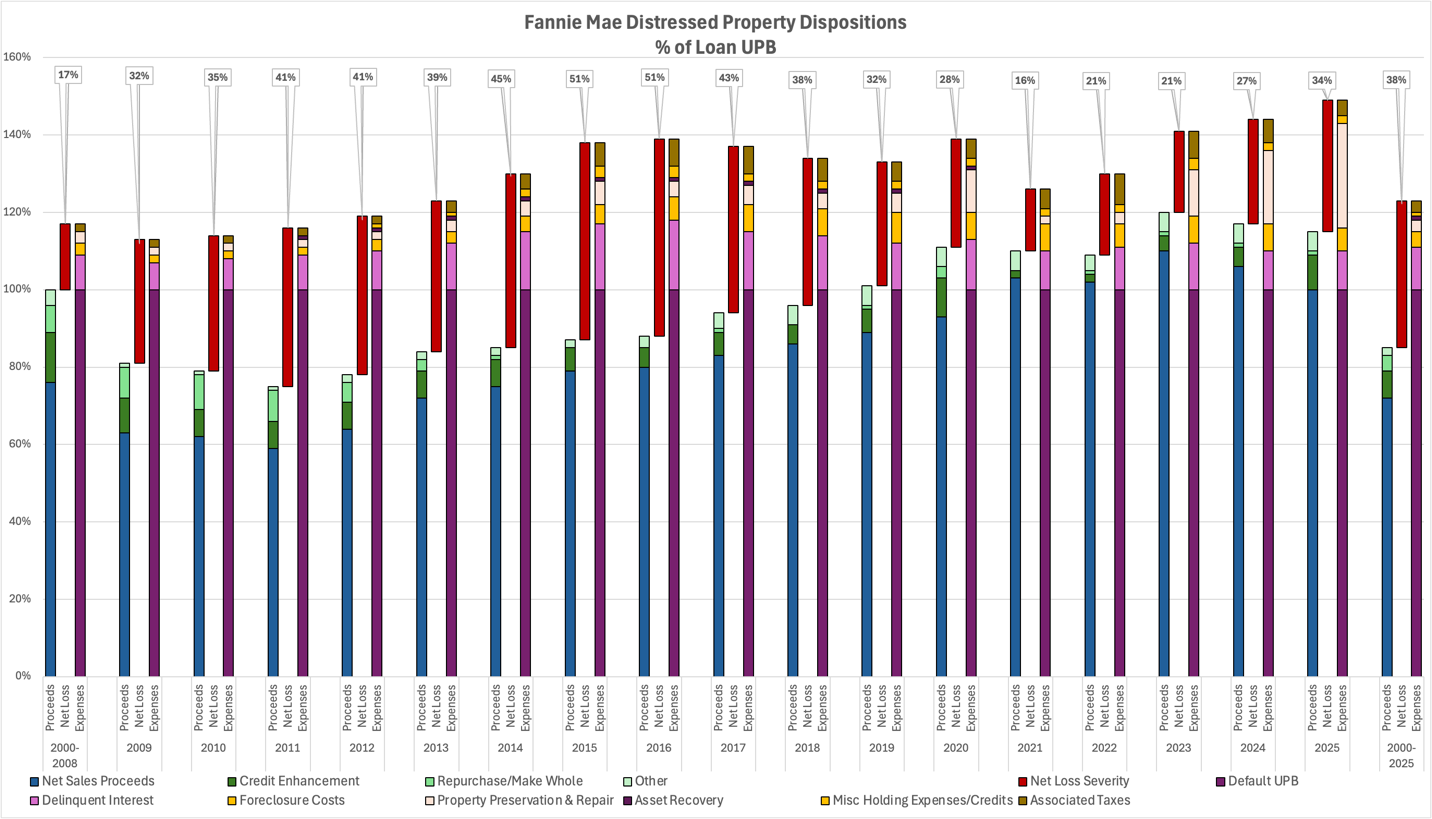

The following chart outline the components of loss for Fannie Mae on distressed property dispositions:

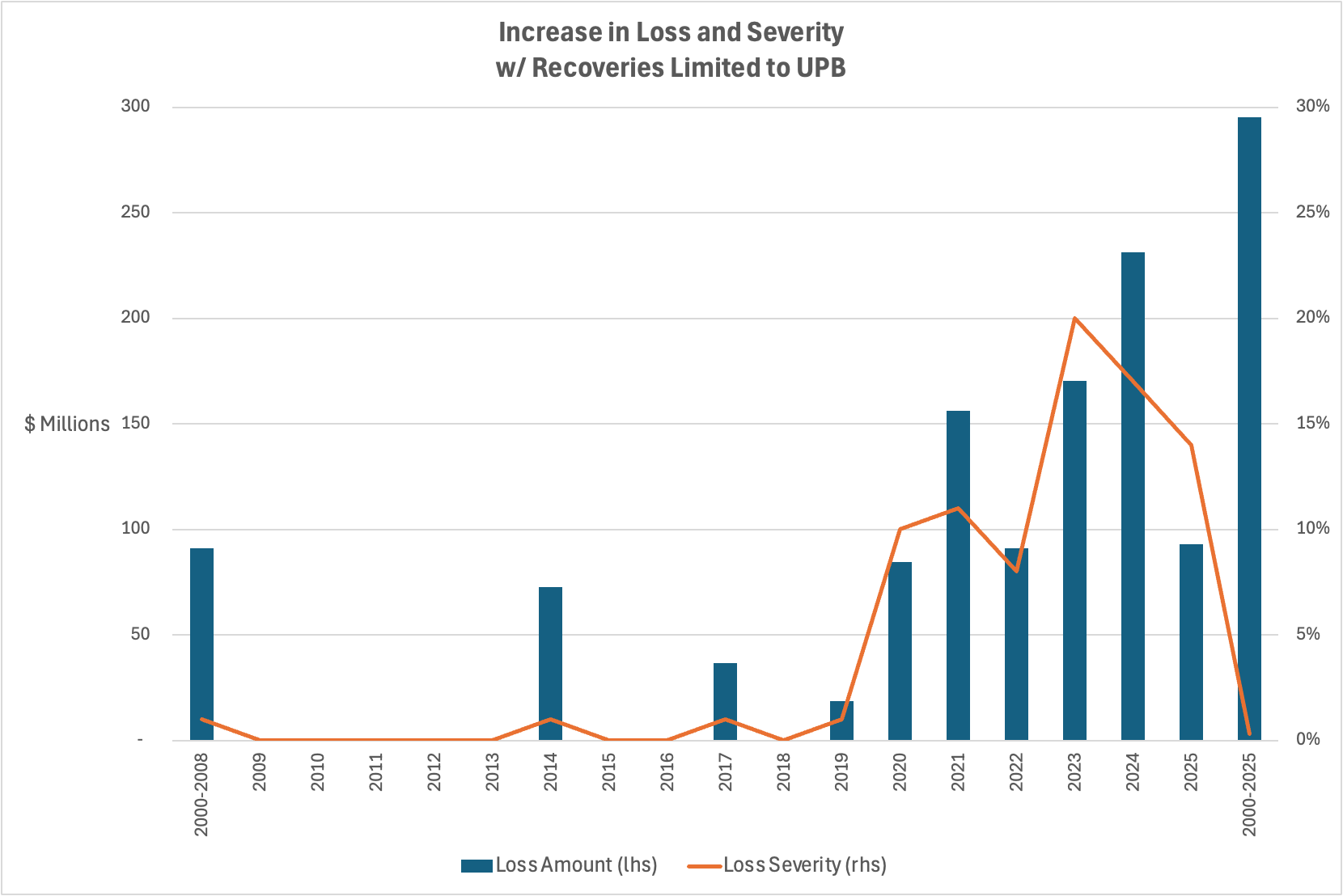

Fannie Mae credit losses would have been ~$100's of millions higher in recent years if recoveries at loan default were limited to loan UPB:

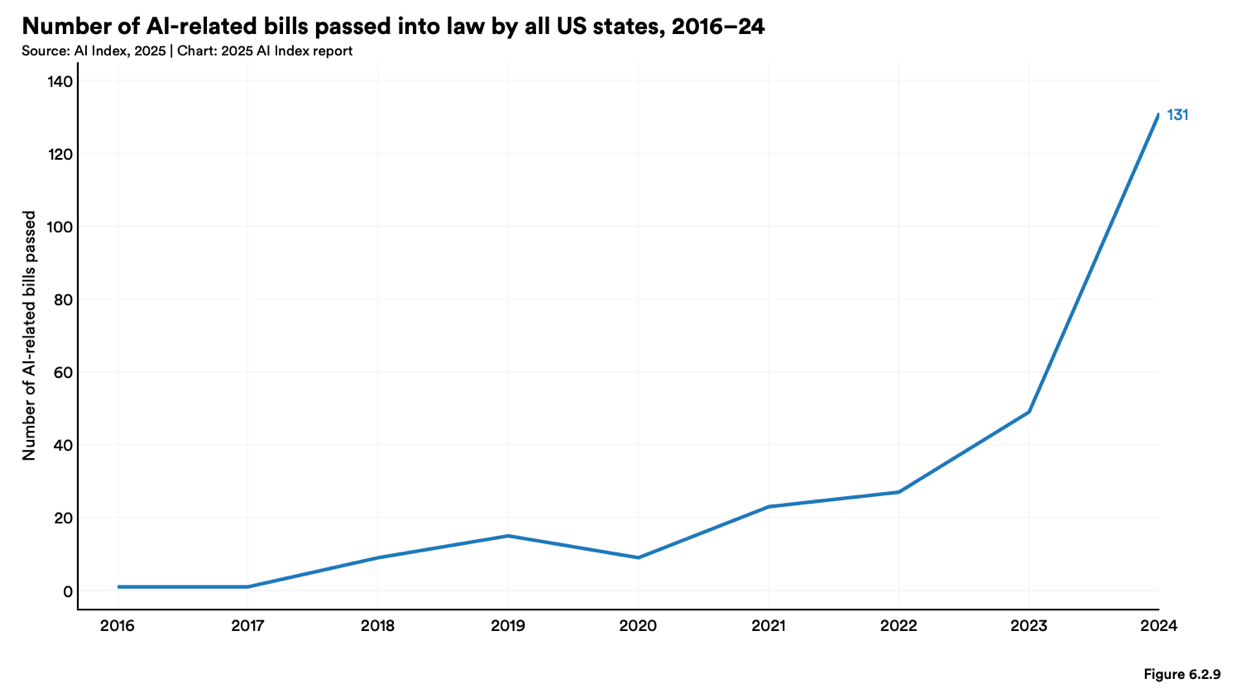

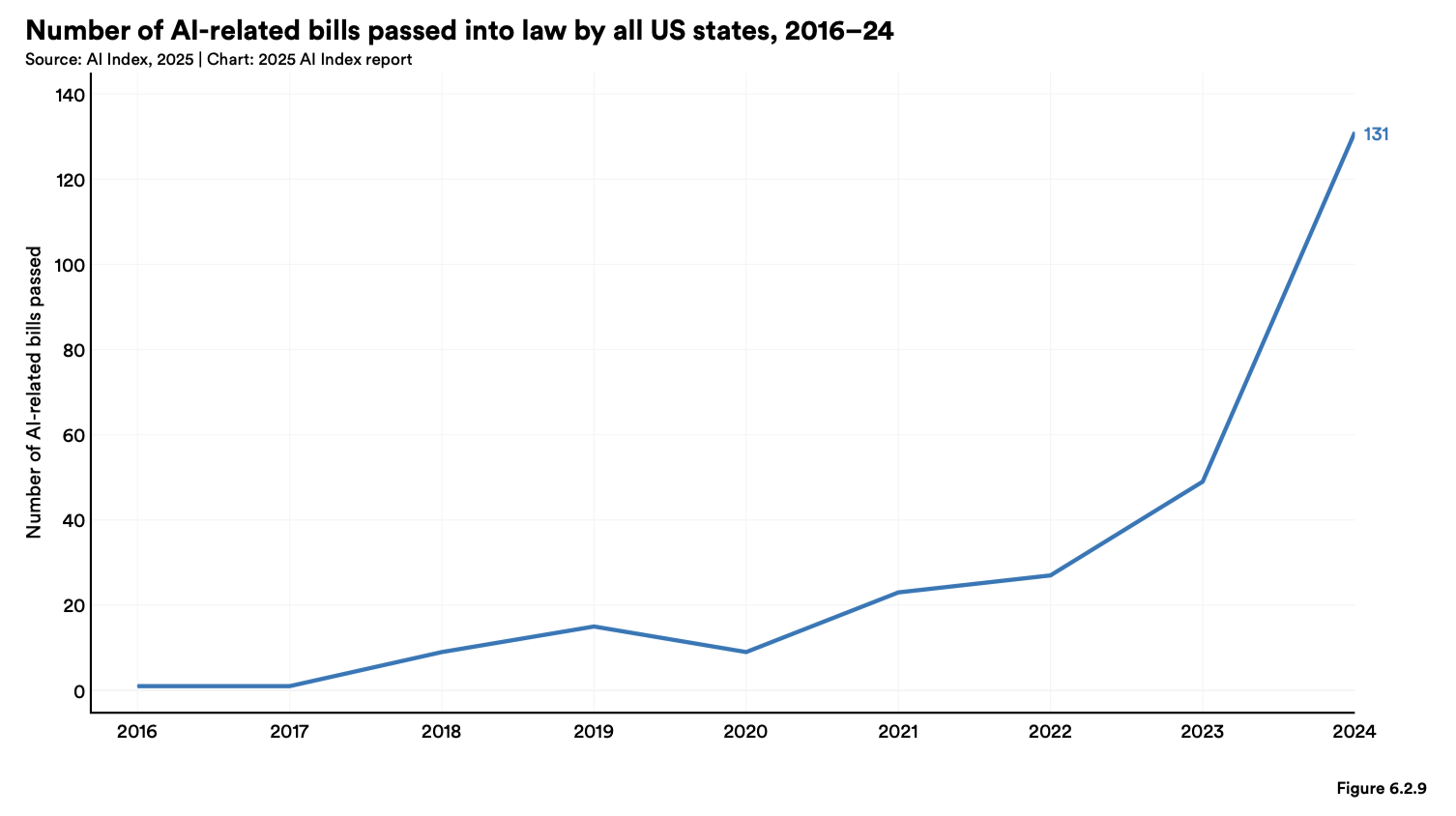

The number of AI regulations has accelerated in the early 2020's.

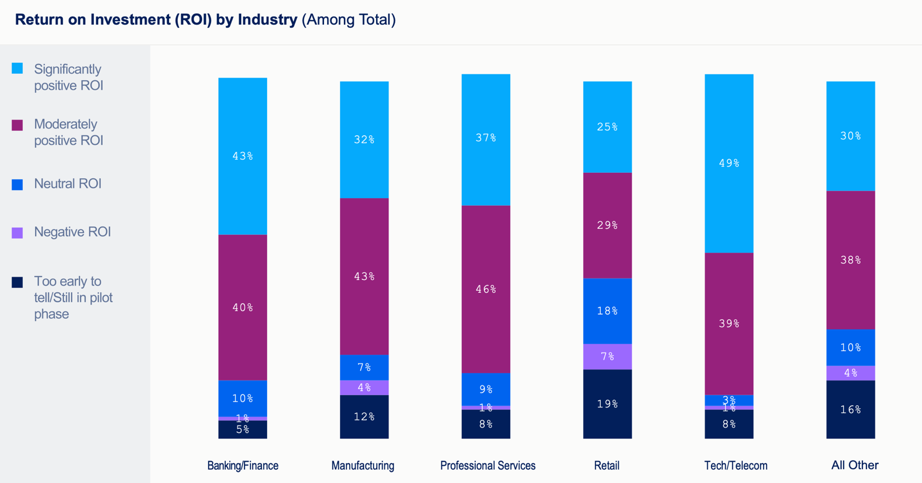

Tech/Telecom and Banking/Finance are the industries with the highest share of firms reporting positive ROI from investment in Gen AI in a 2025 Wharton/GBK Collective study:

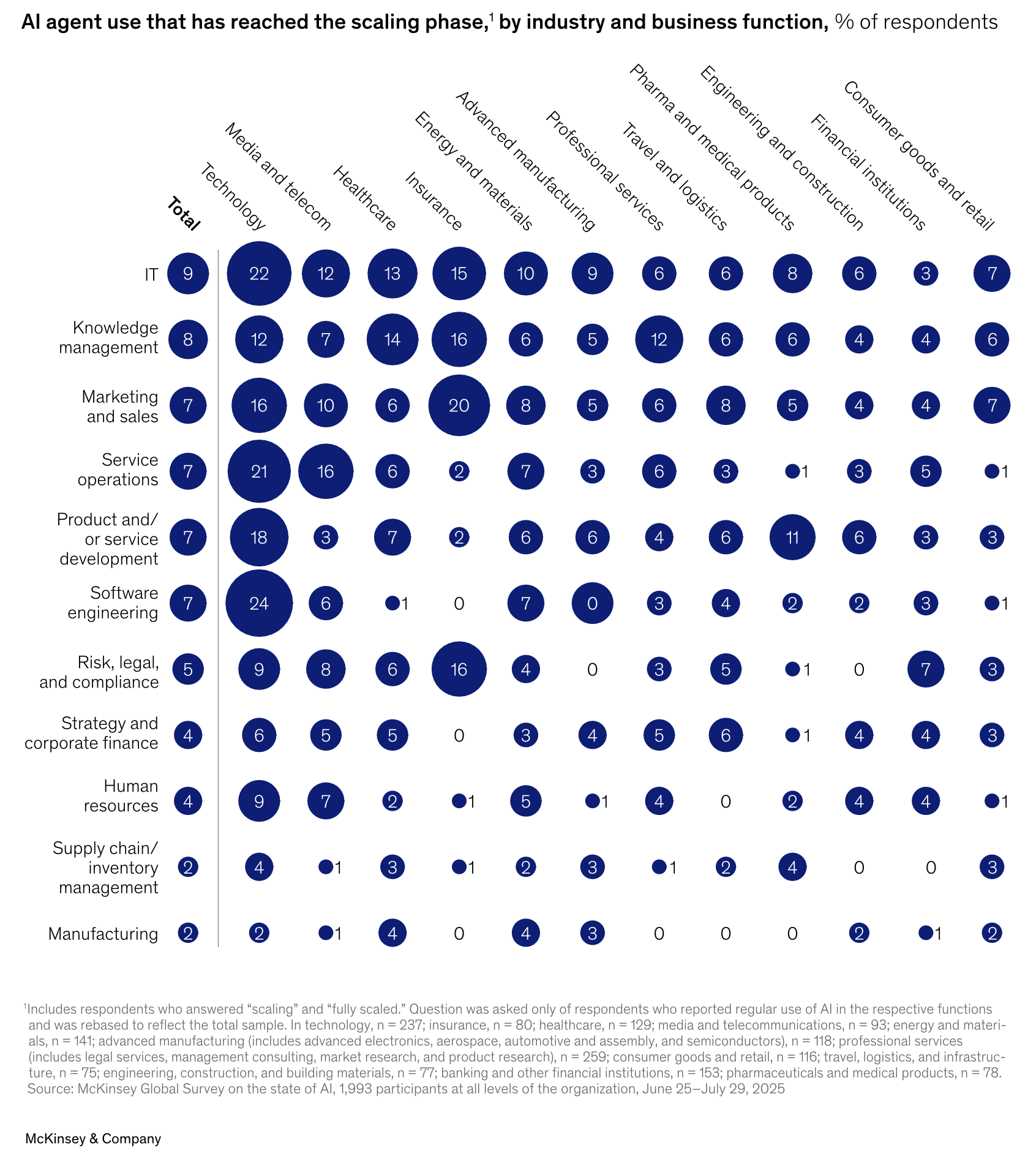

88% of respondents to a mid-2025 McKinsey survey reported use of AI in at least 1 business function, but no more than 10% reported use of AI Agents beyond a pilot phase for any business function. And among respondents at firms reaching the scaling stage, financial institutions lag most other industries across all business functions with the exception of risk, legal, and compliance.

https://www.mckinsey.com/capabilities/quantumblack/our-insights/the-state-of-ai

This Month In History

On April 11, 1968, the Housing and Urban Development Act of 1968 was signed into law, significantly expanding federal support for housing and access to mortgage credit. The Act strengthened FHA's role in the market, particularly through subsidies for low- and moderate-income borrowers (Section 235) and support for rental housing development (Section 236). It also created Ginnie Mae and enabled it to guarantee MBS backed by FHA and VA loans, launching what would become the dominant form of mortgage finance and increasing the liquidity of mortgage loans by opening the market to global investors.

FHA+ is published monthly by Gate House Strategies, a Washington, DC area-based advisory firm focused within the financial services, mortgage lending and servicing, community development, and public housing sectors. Contact us at FHAplus@gatehousedc.com