This Issue Includes:

- Think Piece: Brian Montgomery on President Trump’s housing executive orders and their key implications for HUD and FHA, including appraisal modernization, servicing reform, digitization, and housing supply.

- Three Questions: Michael Marshall on Fannie Mae’s new crypto asset policy, how it aligns with the GENIUS Act, and what the future of digital assets means for mortgage lending.

- Inside Voices: The Economic Report of the President on housing supply, Ginnie Mae’s TPP delinquency fix, VantageScore acceptance, new construction energy code rollback, and the Fed Chair transition.

- Gate House Index: Homeownership affordability relative to median income, cryptocurrency ownership rates and household demographics, geographic distribution of crypto wealth across U.S. households, and Bitcoin volatility trends.

THINK PIECE

President Trump Executive Orders on Housing: Key Implications for HUD and FHA

The recent housing-focused executive orders issued by Donald Trump provide an important directional signal for federal housing policy, particularly around expanding mortgage access and reducing barriers to construction. Collectively, the orders establish a broad framework for housing priorities across federal agencies, including the U.S. Department of Housing and Urban Development (HUD) and the Federal Housing Administration (FHA).

As a threshold matter, these executive orders do not—and cannot—directly alter statutory requirements governing HUD, FHA, VA, or USDA loan programs without formal rulemaking or congressional action. However, there remains substantial administrative flexibility. Agencies can act more immediately in areas such as underwriting policies, appraisal practices, servicing frameworks, and technology adoption. These represent the most realistic near-term levers for HUD and FHA. At the same time, much of the executive orders’ emphasis on bank regulatory relief reflects a broader policy objective of encouraging greater bank participation in the mortgage market—an important addendum given the current dominance of nonbank lenders in FHA and other government lending channels.

Under the first executive order, focused on promoting access to mortgage credit, several implications for FHA emerge. Potential changes to Qualified Mortgage (QM) and Ability-to-Repay (ATR) standards led by the Consumer Financial Protection Bureau could indirectly reshape FHA’s credit box. FHA has long operated with its own QM framework but shifts in broader market definitions may trigger some recalibration of debt-to-income thresholds and other compensating factors to maintain alignment and competitiveness, even though such changes are not statutorily required.

Appraisal modernization is another key area of focus. FHA has historically lagged the GSEs in adopting appraisal flexibilities, and policy direction encouraging the use of automated valuation models and hybrid appraisals could accelerate HUD’s efforts to expand pilots and reduce property-related delays. While FHA’s statutory and regulatory emphasis on property condition, safety, and habitability will continue to limit full substitution of traditional appraisals, there may be opportunities to leverage more technology in the process.

Servicing reform also presents a meaningful opportunity. FHA’s loss mitigation framework remains more prescriptive and operationally complex than those used by the GSEs or the VA, relying on a structured waterfall that requires servicers to evaluate borrowers through a sequential set of options. Although recent updates have streamlined certain elements, the framework continues to involve detailed decision trees and multiple program pathways, creating a higher degree of operational burden relative to more flexible or outcome-oriented approaches in other channels.

In parallel, the executive order’s emphasis on digitization could push FHA and Ginnie Mae to accelerate adoption of eClosings and eNotes—areas where government programs have historically trailed the conventional market. For lenders operating on thin margins, particularly independent mortgage banks, these efficiencies could be significant. Ginnie Mae has been creating momentum in the digital space with rapid growth in its Digital Collateral program—now exceeding $100 billion in eNote-backed securities—and recent policy changes allowing eNotes to be included in its Pools Issued for Immediate Transfer (PIIT) program, expanding execution flexibility and supporting broader adoption across issuers.

The second executive order, centered on removing barriers to building homes, may ultimately have the most meaningful impact on FHA through supply-side effects. FHA serves as a primary access point for first-time and lower-income borrowers, making it highly sensitive to the availability of entry-level housing. Efforts to reduce zoning constraints, streamline permitting, and lower construction costs could expand FHA- eligible inventory and ease price pressures. Additionally, renewed attention to manufactured housing—particularly if accompanied by financing support from the Federal Housing Finance Agency—may prompt HUD to revisit its Title I manufactured housing program and better position FHA within that segment.

Despite these opportunities, several constraints remain. Insurance affordability continues to be a growing challenge for FHA borrowers, yet it sits largely outside HUD’s direct control. Resource limitations within HUD may also slow the pace of implementation, even where policy direction is clear. And while appraisal modernization and AI-driven tools hold promise, safety-and-soundness considerations will necessitate a measured and deliberate approach.

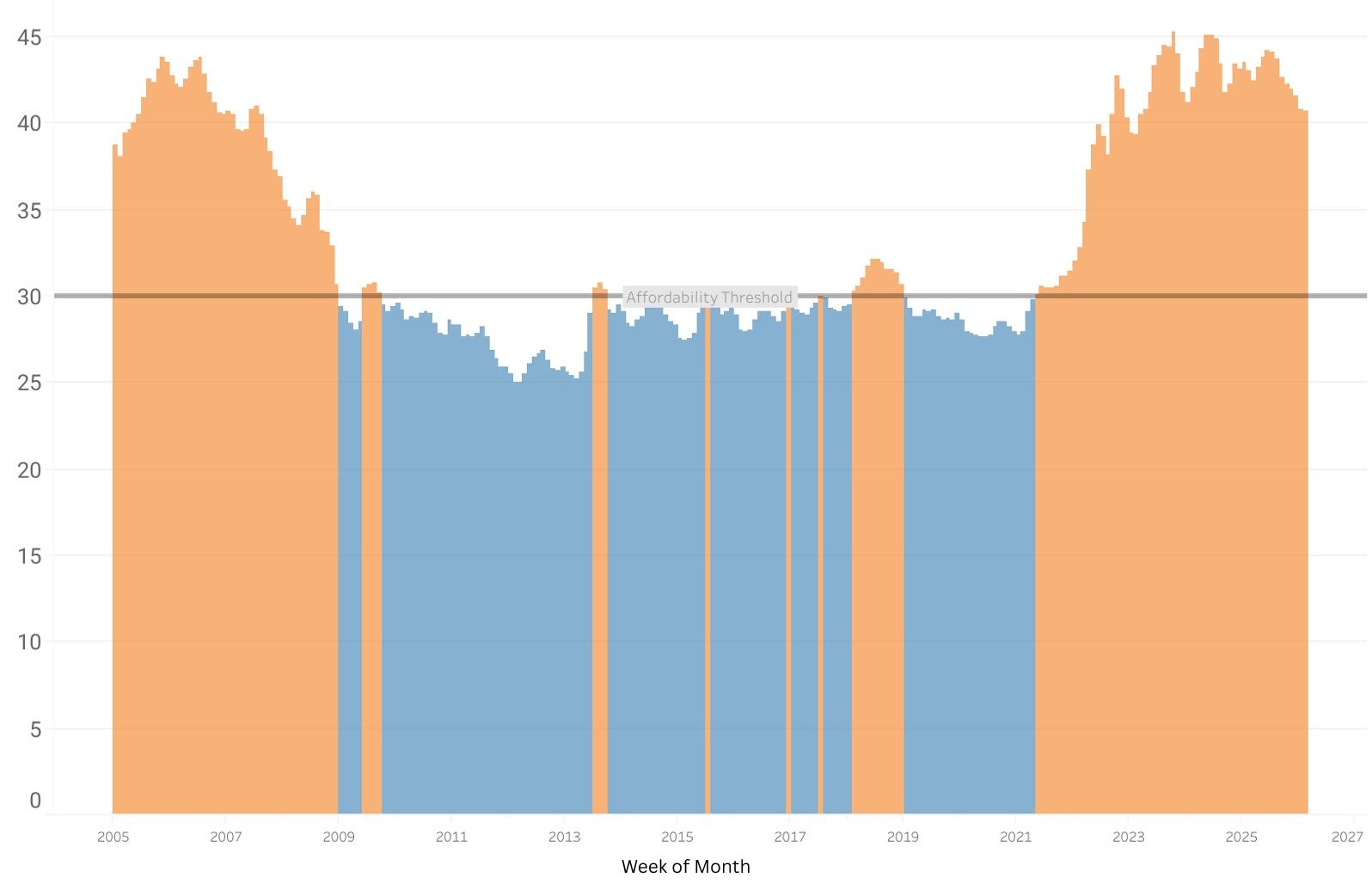

Homeownership Cost share of Median Household Income United States

One notable and constructive theme across the executive orders is the emphasis on prudent, risk-based and fair supervision and enforcement. For HUD, this raises an important question: whether that philosophy will extend to the application of the False Claims Act in the FHA context. Over the past decade, concerns about disproportionate enforcement risk have contributed to lender overlays and, at times, reduced participation in FHA lending—especially among depository institutions who largely exited FHA. A more balanced, transparent, and consistently applied enforcement framework—aligned with the tone of the executive orders—could encourage broader lender engagement while maintaining program integrity.

In the near term, the impact of these executive orders on FHA is likely to be modest but meaningful, particularly in areas such as appraisals, servicing, and digitization. Over the medium term, their influence will depend on whether HUD pursues rulemaking and policy updates consistent with the administration’s direction. The most significant upside lies in supply-side reforms that increase the availability of affordable housing. While substantial work remains, the policy direction—and the expectations for federal housing agencies—are increasingly clear.

Brian Montgomery is the Chairman and Founder of Gate House Strategies and a former two-time Commissioner of the Federal Housing Administration. He also served as Deputy Secretary of the U.S. Department of Housing and Urban Development and is a recognized expert in housing finance policy and FHA programs.

THREE QUESTIONS

with Michael J. Marshall

Marshall, a Founding Partner of Gate House Strategies, shares thoughts on the recent reports that the U.S. has entered a “buyers’ market” in residential real estate. Prior to Gate House, Marshall served in leadership roles at HUD, including Acting Assistant Secretary for Policy Development and Research (PD&R), Chief of Staff to the Deputy Secretary, and Senior Advisor at FHA.

Fannie Mae recently announced that verified cryptocurrency holdings can now factor into mortgage underwriting—a first for the housing finance system. We sat down with Marshall, Partner at Gate House Strategies and former Acting Assistant Secretary at HUD, to explore what this policy shift actually means for borrowers, how it connects to the broader federal effort to bring digital assets into the regulated mainstream under the GENIUS Act, and what the future of crypto in mortgage lending could look like over the next several years.

Question: Fannie Mae recently announced that crypto can be used for mortgage applications, which is a big step—how would this work?

Marshall: Fannie Mae recently clarified that certain cryptocurrency holdings may now be considered in the mortgage underwriting process, but importantly, this does not mean borrowers can make a down payment in crypto or close with crypto assets. The down payment and closing funds must still be provided in U.S. dollars. What is new is that eligible, verified crypto assets can: (1) be pledged as collateral for a separate loan used to fund a down payment and closing costs and (2) be counted as part of a borrower’s reserves or overall financial profile without requiring full liquidation into cash.

This policy shift was directed by Federal Housing Finance Agency (FHFA) and is being operationalized with the help of fintech and digital asset infrastructure firms. By all accounts, both Better Mortgage, an AI-native mortgage originator, and Coinbase, a cryptocurrency exchange, have partnered with Fannie Mae to provide the infrastructure and guardrails needed to launch a crypto-backed mortgage product. Better Mortgage will originate and service the loans. Coinbase will hold and administer the pledged digital assets.

In the proposed structure, the borrower receives two loans at closing: a standard conforming first mortgage secured by the home and a separate second-lien down payment loan supported by the pledged crypto collateral. The structure allows the borrower to use digital assets to help finance a home purchase without requiring liquidation or triggering immediate capital gains on the pledged assets.

This change could particularly benefit a growing segment of “crypto-rich, cash-poor” applicants— often younger borrowers who have accumulated wealth in digital assets but lack traditional liquid savings. By recognizing digital assets within a controlled underwriting and collateral framework, Fannie Mae is signaling a broader evolution in how wealth is defined in mortgage lending, while still maintaining core safety and soundness standards for reserves, repayment capacity, and cash-to- close.

Question: The GENIUS Act was signed into law in July 2025, an important crypto- related milestone. How does the Fannie Mae policy fit with federal goals in the crypto market?

Marshall: The relationship between the GENIUS Act and Fannie Mae’s recent policy on crypto assets reflects a broader federal effort to bring digital assets into the regulated financial mainstream. At a high level, the GENIUS Act aims to establish clearer rules for digital asset markets—particularly around transparency, custody, and the role of regulated intermediaries—while encouraging responsible innovation.

Fannie Mae’s move aligns with those goals by cautiously integrating crypto into traditional mortgage underwriting without disrupting core consumer protections. By allowing verified crypto holdings to count as reserves—but still requiring that down payments be made in cash—the policy mirrors the federal approach of recognition without full substitution. It acknowledges crypto as a legitimate store of wealth, while maintaining the stability and liquidity standards that underpin the housing finance system.

This approach also reinforces the role of regulated custodians, exchanges, and other verifiable financial intermediaries, which is central to the GENIUS Act’s framework. Crypto assets must be documented, traceable, and held in compliant accounts to be considered—paralleling federal priorities around anti-money laundering, investor protection, and market integrity.

More broadly, the policy supports financial inclusion in a way that is consistent with broader federal efforts to integrate crypto within regulated financial markets. It opens the door for “crypto-native” borrowers—often younger households—to access mortgage credit without forcing liquidation of digital assets, while still operating within a prudential, regulated framework overseen by the FHFA.

Question: What should we expect in the crypto future in mortgage lending over the next few years?

Marshall: Over the next few years, crypto’s role in mortgage lending is likely to expand gradually and deliberately as regulators and the GSEs test its integration into a highly risk-sensitive system. Fannie Mae’s recent policy is best viewed as an initial step, not an endpoint. It signals openness to innovation, while maintaining a cautious posture around credit risk, volatility, liquidity, and consumer protection.

The direction is being set by FHFA, which has encouraged both GSEs to explore how digital assets can be incorporated into housing finance. As a result, it is reasonable to expect that Freddie Mac will introduce a comparable framework within the next year, which should help validate the asset class and accelerate broader adoption across the conventional mortgage market.

The opportunity set is significant. As GSE engagement deepens, we could see expanded use of crypto as verified reserves; integration of digital asset data into automated underwriting systems; and the development of standardized valuation and documentation protocols. There is also potential for faster, more transparent asset verification through blockchain-based infrastructure, reducing friction in the origination process.

Beyond underwriting, longer-term opportunities could include tokenized representations of mortgage assets, improved secondary market liquidity, and new channels for investor participation. For borrowers, particularly younger and “crypto-native” households, this evolution may broaden access to credit without requiring full liquidation of digital wealth.

That said, progress will remain measured. The GSEs are likely to proceed in phases— piloting, refining, and scaling—ensuring that innovation aligns with safety and soundness as crypto becomes a more defined part of the mortgage ecosystem.

INSIDE VOICES

Housing Headlines:

The recently issued Economic Report of the President 2026 highlights the nation’s housing supply shortfall, which continues to drive home prices and monthly payments higher. The report underscores DTI as an affordability constraint as elevated rates and home prices have pushed typical payments beyond what many borrowers can sustain. It also signals a decisive shift toward deregulation and cost reduction, targeting zoning, permitting, and building requirements as major contributors to housing costs. For FHA, the emphasis is increasingly on supporting multifamily production and lowering financing costs. Taken together, the message is clear: meaningful affordability relief will require more housing supply and lower per-unit costs—not just lower rates or expanded credit access.

FHA Calculus:

Ginnie Mae announced on April 24 that it will temporarily exclude FHA loans in Trial Payment Plans (TPPs) from issuer delinquency calculations, acknowledging that recent policy changes have artificially elevated reported delinquency rates. Following FHA’s 2025 update to its loss mitigation waterfall—which now requires borrowers to complete a TPP before accessing permanent solutions like partial claims—servicers have seen a surge in loans classified as delinquent while in trial status. This shift reflects a process change, not performance deterioration, as more borrowers are funneled through TPPs upfront. The move is intended to provide temporary operational relief to issuers until TPP volumes normalize under the new framework.

Vantage Score Splash:

At a recent joint press conference, FHFA and HUD announced the acceptance of VantageScore as a credit scoring model, noting that Freddie Mac had acquired roughly $10 million in pilot loan volume. Director Pulte emphasized the potential for rental payment history to expand access to credit, while also pointing to expected cost reductions from increased competition among credit scoring models. For such a significant change, the devil is in the details, and the industry is now closely parsing best execution, risk, and operational implications. FHA in particular will likely require meaningful lead time to fully implement the changes, suggesting a more gradual rollout than the GSEs.

New Construction Relief:

HUD Secretary Scott Turner recently announced a rollback of prior energy-related housing policies, eliminating the requirement that FHA- and USDA-financed new construction meet the 2021 International Energy Conservation Code, which HUD estimated added roughly $20,000–$31,000 per home. The move reflects a broader shift away from energy mandates toward affordability and supply, lowering upfront costs and expanding the pool of homes that can qualify for financing while reinforcing deregulation as a central housing policy lever.

Federal Reserve:

The DOJ dropped its investigation into Fed Chair Jerome Powell related to the Fed’s renovation project, removing a key obstacle to Kevin Warsh’s potential confirmation. Powell’s term as Chair expires May 15, 2026. While the composition of the Federal Open Market Committee will continue to shape rate decisions, a leadership change at the top could be meaningful for monetary policy direction in the foreseeable future. To the surprise of many, Powell announced his intention to retain his seat on the Board of Governors through 2028 - thus remaining influential in Fed decisions.

THE GATE HOUSE INDEX

The Gate House Index and analysis is designed to provide insight into the status of FHA’s business at a moment in time and over a period of time, as well as other pertinent data points we’re following.

This month’s Index is tied to the Three Questions theme on cryptocurrency in mortgage lending. The data explore homeownership costs as a share of median household income, the prevalence of crypto asset ownership across U.S. households, the demographic profile of crypto investors—with younger adults and men more likely to participate—the geographic concentration of crypto wealth per capita, and Bitcoin’s volatility relative to other asset classes. Together, these data points provide context for understanding who holds crypto wealth, where it is concentrated, and what its characteristics mean for housing finance.

1. Homeownership cost of the median-priced U.S. home remains above 30% of median household income.

2. The 2022 Survey of Consumer Finances data indicate that about 4.3% of U.S. households owned cryptocurrency, and the top quartile of owners held more than $10,000 in crypto assets.

3. Younger adults and men are more likely to have invested in crypto assets.

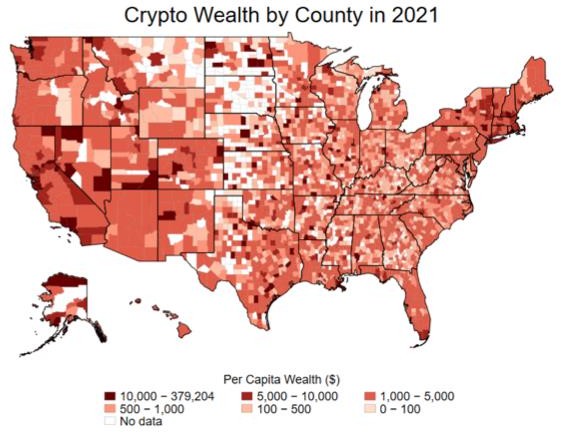

4. FDIC reported data that shows that households across the nation hold crypto assets, and certain areas have significant crypto wealth per capita as of December 2021.

5. Bitcoin Volatility remains high relative to other asset classes, but declined between 2017 and 2024.

This Month In History

In May 1862, Abraham Lincoln signed the Homestead Act of 1862 into law to promote westward expansion, support small farmers, and strengthen the Union during the Civil War. The Act granted 160 acres of public federal land to eligible settlers, with most of the available land located in the Great Plains (including Kansas and Nebraska), the Mountain West (including Colorado and Montana), and western regions (including Oregon and California). To qualify, settlers had to be adults (or heads of household) who had not borne arms against the United States, and then improve the land and live on it for five years. Many former Confederates became eligible after the Civil War through pardons or restored rights. About 30–40% of claimants ultimately met these requirements and received title.

FHA+ is published monthly by Gate House Strategies, a Washington, DC area-based advisory firm focused within the financial services, mortgage lending and servicing, community development, and public housing sectors. Contact us at FHAplus@gatehousedc.com