.avif)

This Issue Includes:

- Think Piece: As we approach the 250th July 4th celebration, for this special (and lengthier) edition of Think Piece, our partner Brian Montgomery reflects on the history of the housing and housing finance industry, its remarkable evolution and growth over two and a half centuries, and the ways in which it has adapted to meet the nation’s significant challenges, and even, perhaps contributed to the Founders' vision of life, liberty, and the pursuit happiness for ordinary Americans.

- Three Questions: Mike Frueh on the new VA Partial Claim loss mitigation program, the VA Home Loan Affordability Act, and funding fee tradeoffs in the VA Omnibus bill.

- Inside Voices: FHA’s modernization push through recent Mortgagee Letters, a widening gap between FHA and conventional delinquency rates, Bill Pulte’s dual mandate at FHFA and ODNI, and the housing market’s $30 trillion equity cushion.

- Gate House Index: In honor of America's 250th birthday, this month's Gate House Index charts the nation's growth from 2.5 million people to today — population, urbanization, the Homestead Act's 270 million transferred acres, homeownership rates, and the $50+ trillion in residential real estate value now underpinning the American economy.

THINK PIECE

America’s 250th Birthday: A Housing Finance Journey Through the Nation’s History

As America celebrates its 250th birthday, the country is taking stock of how this grand experiment all began, how far it’s come, and just how we’ve gotten to where we are today.

We thought it would be the appropriate time to reflect on the industries that have helped put a roof overhead for millions upon millions of Americans in these first two-and-a-half centuries. More importantly, perhaps, is to appreciate how these endeavors have served as a foundation for society – as our population expanded across the frontier, swelled exponentially with a growing middle class, and supported the nation as it became a world power.

Drawing on John Locke’s principle that government exists to protect life, liberty, and property, our Founders believed that distributing land and property broadly was essential to building a stable, free society. In their view, ordinary citizens had a right to own a piece of the new country, and that broad ownership was vital to a healthy republic.

Indeed, when the Declaration of Independence was adopted in 1776, the idea of property ownership was baked into the country’s DNA. At the time, the American population was about 2.5 million, overwhelmingly rural, with just 5% living in our cities, and most families lived in homes they built for themselves utilizing local materials. It was a farming and frontier society, where financing the acquisition of land and construction of homes relied largely on personal savings, seller credit, private agreements, and community relationships.

Nine years later, the Continental Congress passed the Land Ordinance of 1785, with Thomas Jefferson as its intellectual architect, creating a system for surveying, subdividing, selling, and titling western lands with legal precision before settlers even lived there. It turned land into a commodity and laid the groundwork for a speculative land market that would help define the decades ahead in America. In a famous letter of that year, Jefferson described small landowners as “the most precious part” of a nation.

As the country expanded westward during the nineteenth century, housing development followed. The Northwest Ordinance of 1787 became the template for organizing federal territories. It also banned slavery in the Northwest Territory, which had a critical impact on the way these lands were settled, by smaller farms versus large landholders working the land with enslaved people.

The 19th Century – Transcontinental Transformation

By 1800, America had 5.3 million people. The Louisiana Purchase (1803) added 828,000 square miles and doubled the national territory overnight. The Northwest Territory (Ohio, Indiana, Illinois, Michigan, Wisconsin) opened for organized settlement.

A series of federal land laws made western lands increasingly accessible to private citizens. The Land Act of 1800 allowed for credit purchases and installment payments to the government for the first time but also fed land speculation. The Land Act of 1820 ended credit purchases but reduced the minimum price and parcel size so that ordinary farmers, not just large speculators, could participate.

In the 1820s and 1830s, following the end of federal credit for land purchases, state-chartered banks expanded as sources of loans for farm and land purchases, but many were undercapitalized, unstable, and vulnerable to failure. The typical bank mortgage loan was a short-term, interest-only loan with a balloon payment. By the 1830s, building and loan associations appeared, offering a mutual model of home finance in which members made regular payments toward shares in the association that could be used to retire their mortgage debt.

The Erie Canal and the railroads ended dependence on local building materials; lumber, brick, and standardized components could now move anywhere.

The Preemption Act of 1841 gave squatters who had already occupied and improved public land the opportunity to purchase it at a minimum price before it was offered for public sale. And in the Civil War era, the Homestead Act of 1862 and the Southern Homestead Act of 1866 further encouraged settlement, as railroads and industrialization spurred the growth of new towns and cities.

The federal government also rewarded military service with land. Congress issued transferable bounty land warrants to veterans of the Revolutionary War, the War of 1812, and the Mexican-American War. The warrants were ultimately redeemed for tens of millions of acres, but they did more to fuel speculative land markets than to turn veterans into property owners because most veterans sold them at a discount to brokers and speculators.

By 1850, the country stretched to the Pacific: the Oregon Territory, Texas annexation, and the Mexican Cession added the entire western half of the continent. Over the next few decades, mortgage lending gradually became more common, but national banks played only a limited role in real estate lending and financing remained mostly fragmented, localized and often risky. Western farm mortgage companies were a small but notable exception, originating mortgage loans to borrowers in the Midwest and Great Plains and selling those loans to investors in the Northeast and Europe while retaining the servicing. Most mortgages were, again, short-term loans, typically lasting five years, with interest-only payments and a large balloon payment due at maturity. Borrowers frequently had to refinance their loans, which left families vulnerable during economic downturns. The financial crises of the 1890s exposed the risks of speculative land markets, farm distress, and unstable sources of credit.

The 20th Century – Meeting the Modern World

By 1900, America had been utterly transformed: 76 million people, 40% urban, a transcontinental railroad, and, remarkably, a frontier declared closed. Still there was no national mortgage market. Savings and loans were important for urban buyers and life insurers got into the business, as did some mutual savings banks, but a significant portion of mortgage finance was provided by private lenders, seller financing, or wealthy local investors.

Early 20th century housing problems – scarce mortgage credit, overcrowding, substandard conditions, and speculation – were only partly remedied by state and local regulation. The market remained acutely vulnerable when the Great Depression hit. Home lending effectively excluded most of the working class. At the time, mortgage loans typically required a large down payment, often half the purchase price, and presented elevated risk of default to lenders and average American households. Urban real estate boomed in the 1920s, but the boom was highly dependent on credit availability, and stable or rising home values.

The shortcomings of this system for the country’s growing needs became painfully clear during the Great Depression. As banks failed, credit dried up, and home values collapsed, millions of Americans faced foreclosure. By the early 1930s, the nation’s housing finance system was in crisis. In response, the federal government undertook the most significant housing policy transformation in American history.

Congress passed the Federal Home Loan Bank Act of 1932 to stabilize the housing market and support mortgage lending by providing liquidity to local financial institutions, for the first time addressing fragmentation and creating a federal backstop. The Home Owners’ Loan Act of 1933 formally chartered a federal savings and loan system and created the Home Owners’ Loan Corporation (HOLC), which refinanced over 1 million mortgages into longer-term, amortizing loans. But HOLC’s residential security maps (created in 1935-1940) also codified the discriminatory neighborhood risk-rating practices of the era.

The creation of the Federal Housing Administration (FHA) in 1934 fundamentally changed the mortgage market. Building on the long-term, fully amortizing loan structure that HOLC had pioneered in its refinancing program, FHA introduced mortgage insurance and standardized underwriting, transforming the standard mortgage product from a short-term, interest-only balloon loan into a long-term, fixed-rate, fully amortizing, and freely prepayable loan that American families could realistically repay over time. Over the following decades, the 30-year fixed-rate mortgage became the American standard.¹ Unlike balloon and adjustable-rate mortgages, the fully amortizing fixed-rate mortgage provides predictable monthly payments and protection from interest-rate fluctuations, an innovation that, together with other federal policies, made homeownership attainable and sustainable for the middle class and helped millions of families build wealth and financial security. Not all American families benefited equally, however. For more than three decades, FHA’s underwriting included racially discriminatory appraisal practices that restricted credit in Black and other minority neighborhoods until the reforms of the 1960s.

In 1938, the Federal National Mortgage Association (Fannie Mae) was created to provide liquidity to mortgage lenders and reduce regional variations in credit availability by establishing a national secondary mortgage market for FHA loans.

The Servicemen’s Readjustment Act of 1944 (the GI Bill) added the VA home loan guaranty, which allowed millions of returning veterans to purchase homes with little or no down payment. Together, FHA and VA financing powered the postwar homeownership surge. The national homeownership rate rose from about 44 percent in 1940 to more than 60 percent by 1960.

In 1965, the creation of the Department of Housing and Urban Development (HUD) elevated housing policy to a Cabinet-level priority, with FHA, which was folded under it, continuing to serve as a cornerstone of the federal government’s housing and homeownership mission. The Government National Mortgage Association (Ginnie Mae) was established on September 1, 1968, under the Housing and Urban Development Act of 1968, which restructured the original Fannie Mae by dividing it into two separate entities: Ginnie Mae, a wholly owned government corporation, and a rechartered Fannie Mae operating as a shareholder-owned company.

Ginnie Mae supports liquidity for government-insured and -guaranteed mortgages, providing a full faith and credit guaranty on securities backed by FHA, VA, USDA, and other government loans. In 1970, Ginnie Mae guaranteed the first mortgage-backed security (MBS), which let lenders pool and sell mortgage loans in the secondary market. The structure attracted global investment capital and replenished lender funds to expand the availability of mortgage credit nationwide. A key benefit of mortgage securitization was that it separated mortgage credit risk from interest-rate and prepayment risk; lenders and investors could retain, transfer, or manage those exposures according to their preferences, risk tolerance and expertise. Freddie Mac followed in 1970 and brought competition to the secondary market and additional liquidity to primary market lenders.

Together these institutions, each with a distinct mission, created the housing finance infrastructure that remains the foundation of the modern mortgage ecosystem.

The post-World War II housing boom, suburban development, interstate highway expansion, and growth of the American middle class were all supported by expanding access to mortgage credit. Homeownership became a symbol of the American Dream and one of the most important sources of wealth creation for American families.

Like the nation itself, housing finance has faced significant challenges. Persistent housing discrimination, which had been perpetrated through government programs including FHA, led to the Fair Housing Act of 1968. Passed in the week following Martin Luther King Jr’s assassination, it prohibited discrimination in the sale, rental, or financing of housing.

High inflation and mortgage rates in the 1970s and early 1980s contributed to the Savings and Loan Crisis of the 1980s, which demonstrated the risks associated with funding long-term mortgages with short-term deposits and led to FIRREA and other regulatory reforms. The financial crisis of 2008 exposed weaknesses in collateral and borrower underwriting as well as securitization and risk management discipline, leading to HERA, GSE conservatorship, the Dodd-Frank Act, and other substantial regulatory reforms, but left the underlying housing finance framework in place. More recently, the housing finance system demonstrated remarkable resilience during the COVID-19 pandemic through coordinated forbearance programs, servicing reforms, and operational flexibility.

Looking Ahead – Building the Next Chapter of the American Housing Story

As America enters its next 250 years, innovation in housing and housing finance is accelerating. The next 250 years will look different, starting with construction. 3D printing, modular manufacturing, and offsite assembly all promise homes built faster and at lower cost, and AI may compound those gains: generative design can produce and test floor plans in hours, robotics could ease the industry’s chronic shortage of skilled labor, and better supply-chain forecasting can reduce the material delays and cost overruns that have burdened builders for decades. None of this has reached scale, but even modest progress would matter in reducing the current and long-lasting shortage in housing supply.

Housing finance is changing as well. Shared-equity programs, co-living arrangements, and technology-enabled down payment assistance are giving buyers options that did not exist a decade ago, and digital platforms and eClosings have already removed meaningful time and cost from the process. AI is now reaching the operational core of the business — underwriting, document review, fraud detection, compliance — and as those routine tasks are automated, loan officers are becoming advisers more than processors. Human oversight is not optional: fair lending and consumer protection must be designed into these systems from the outset, not audited in afterward. If the technology delivers, it will reduce the two stubborn costs of homeownership, building the home and financing it.

Throughout America’s 250-year housing history, the meaning of home has extended far beyond bricks and mortar. Homeownership has long represented the opportunity to create a true sense of home, a place where families are raised and traditions are passed from one generation to the next. More than a financial asset, a home provides stability and belonging, the foundation on which many Americans build their lives. As Ronald Reagan said, “Home ownership is an essential part…of the American dream. It strengthens the family. It’s fundamental to our way of life.”

The next chapter of the American housing story is already being written. The story of American housing and housing finance is ultimately the story of America itself. If the first 250 years were defined by expanding opportunities for homeownership in pursuit of the Founders’ ideal, the next 250 years may be defined by the challenge of making housing and housing finance more accessible, liquid, customizable, and technologically advanced for future generations of Americans.

Brian Montgomery is Chairman and Co-Founder of Gate House Strategies and former Deputy Secretary of the U.S. Department of Housing & Urban Development (HUD).

¹ The U.S. is nearly unique among industrialized nations in having the 30-year, fixed-rate, freely prepayable mortgage, a structure that shifts interest-rate risk from households to investors, as the standard product used to finance homeownership. Adjustable-rate mortgages or short-term fixed-rate rollover mortgages predominate in other industrialized nations except Denmark, where long-term fixed-rate, prepayable mortgages are funded in its covered-bond market. Also, Danish borrowers avoid the “lock-in” effect that U.S. borrowers face when rates rise, because they can purchase the specific bonds funding their mortgage at a discount to retire their debt.

THREE QUESTIONS

by Mike Frueh, Senior Advisor with Gate House Strategies and former VA Acting Under Secretary for Veterans Affairs

QUESTION 1: What is the VA Partial Claim program, and how does it change loss mitigation for Veterans?

Frueh: The Department of Veterans Affairs has officially launched its new VA Partial Claim program following publication of the final rule on June 1, with the program going live June 15. Servicers have been given a 180-day implementation window to fully integrate operational and system changes, but many had already been preparing in advance due to the scale of the policy shift.

At its core, the program modernizes how the VA supports veterans experiencing mortgage hardship. It introduces a structured loss mitigation option that allows delinquent payments to be advanced by the servicer (and reimbursed by VA), and placed into a subordinate, interest-free obligation. The balance of this subordinate debt only becomes due in full when the home is sold, the loan is refinanced, or the loan reaches maturity.

In practice, the program was designed to align with successful loss mitigation strategies in use by the GSEs and FHA, working in tandem with a now codified waterfall of loss mitigation options. The changes allow Veterans to access the same type of home-retention options available to conventional borrowers. In the current rate environment, adding the partial claim allows Veteran borrowers to retain their existing first mortgage, and its interest rate, rather than relying solely on loan modifications to current market rates.

The VA Partial Claim program represents a significant evolution in Veteran loss mitigation policy; it represents a shift from short-term relief tools to a more durable, structured pathway that prioritizes home retention while maintaining program sustainability.

QUESTION 2: What is the VA Home Loan Affordability Act all about?

Frueh: Following enactment of the VA Home Loan Program Reform Act of 2025, policymakers have continued pushing reforms to further increase scalability of VA lending, reduce friction in servicing, remove regulatory barriers, and improve outcomes for veterans. Recently, House Republicans introduced the VA Home Loan Affordability Act (H.R. 8532), which would help accelerate closing timelines, reduce or remove regulatory burdens, expand digital processing capabilities across VA lending channels, and align select VA practices more closely with other federal housing programs. The bill is sponsored by Representative Derrick Van Orden (R-WI) and includes several original co-sponsors, including Reps. Mike Bost, Juan Ciscomani, Tom Barrett, and Jen Kiggans.

At its core, the legislation seeks to make the VA mortgage process faster and less administratively burdensome for Veterans, lenders, and servicers, to help Veterans better compete with conventional borrowers. A key objective is to accelerate closing timelines by reducing documentation requirements and improving the speed of loan processing through more standardized and automated workflows.

Another major focus is appraisal modernization and flexibility. The bill aims to increase the number of certified appraisers, reduce unnecessary appraisal hurdles and improve consistency in property valuation requirements, particularly in situations where reliable data or prior valuations already exist (particularly with VA Interest Rate Reduction Refinance Loans). In addition, the bill works to align VA Minimum Property Requirements more closely with the GSEs and other federal housing programs. These efforts are intended to reduce inconsistencies across federal mortgage programs that can create confusion, delay underwriting decisions, and/or increase compliance complexity for lenders operating across multiple agencies.

The legislation also prioritizes technology modernization and system interoperability. It encourages more efficient VA–lender digital interfaces, better data exchange standards, and expanded use of automated underwriting and verification tools. These changes are designed to reduce manual processing steps, lower operational costs, and improve overall system responsiveness for both lenders and veterans.

Overall, the VA Home Loan Affordability Act represents a targeted effort to modernize the VA lending ecosystem—focused on reducing friction, improving speed, and enhancing the borrower experience while maintaining the unique protections of the VA loan guaranty and aligning more closely with broader federal housing frameworks. The bill is currently under review by the House Committee on Veterans’ Affairs.

QUESTION 3: The VA Omnibus bill has significant financial implications and tradeoffs—what is being proposed?

Frueh: The VA Omnibus package, Take Care of America’s Veterans Act (S. 4744/H.R. 9237), under consideration reflects an effort to consolidate broad, bipartisan measures that modernize and expand Veteran benefits and care programs. While mostly focused on care and benefits outside the mortgage finance world, it does contain a section that impacts the mortgage industry. The Sharri Briley and Eric Edmundson Veterans Benefits Expansion Act (H.R. 6047) has been rolled into the omnibus, which expands eligibility for National Guard and Reserve members, as well as modifies and extends certain funding fees to pay for the section.

This highlights the perennial tension in federal lawmaking or rulemaking: any new or expanded expenditures generally must be offset with corresponding savings or revenue increases under statutory pay-as-you-go requirements. As a result, the bill is structured around a series of complex “Pay-For” mechanisms that have generated active debate among policymakers and Veteran advocacy groups.

There are significant other “Pay-Fors” in the omnibus bill, but the funding fee Pay-Fors will impact Veteran borrowers the most. The VA home loan program originated with the landmark Servicemen’s Readjustment Act of 1944, commonly known as the GI Bill. VA did not charge a funding fee until 1966, when it created a one-time charge of 0.5%. This fee varied from 0.0% to 1.0% until the 1990s, when the tiered system in use today was created, with fees dependent on type of loan, number of uses of the program, and downpayment amount. Congress codified a funding fee waiver for certain Veterans in receipt of disability compensation in 1982.

The Sharri Briley and Eric Edmundson Veterans Benefits Act relies on fee-based and structural changes within the VA home loan ecosystem, including a funding fee increase from 0.5% to 1.42% for refinance loans, 0.5% to 1.0% for loan assumptions, and an overall extension of the current baseline funding fee rate schedule for an additional 28 months.

Funding fees were created to ensure that expanded VA housing and benefits programs remain budget-neutral over the long term; however, they have been used over the years to pay for unrelated benefits and care. Increasing funding fees introduces tradeoffs that can directly affect borrower behavior, affordability, access, and loan utilization patterns—particularly in refinance-sensitive environments or for borrowers hoping to assume a VA loan.

The complexity of these offsets has led to healthy but difficult policy debate. Some stakeholders argue against creating new benefits solely by shifting costs onto Veterans using other programs (like the VA home loan program). Others emphasize the importance of maintaining fiscal discipline while ensuring new benefits are fully funded rather than adding pressure to discretionary spending.

Given these fiscal realities, it’s fair to say that there will be a lot more discussion about the provisions within the omnibus bill. The final bill, if enacted, will likely differ from the current in many ways, but funding fees will still exist; changes to the current tiered system are always in the works, so lenders will have to be prepared to modify systems and account for changes in borrower behavior when they do change.

INSIDE VOICES

Road to Housing Drumroll:

Never a dull moment in Washington. After months of negotiations, Congress overwhelmingly approved the bipartisan 21st Century ROAD to Housing Act, with the Senate voting 85-5 on June 22 and the House following 358-32 on June 23, sending the legislation to President Trump’s desk. A White House signing ceremony was scheduled for June 24, but President Trump unexpectedly postponed action, saying he would not sign the bill until Congress advances the unrelated SAVE America Act. The procedural twist may ultimately have little practical effect: unless the President vetoes the legislation, it will automatically become law after the Constitution’s ten-day review period (excluding Sundays), provided Congress remains in session. For now, Washington is watching whether this becomes another chapter in the bill’s unusual legislative journey—or simply a brief pause before enactment.

FHA is on a Roll:

FHA’s recent flurry of Mortgagee Letters reflects the ongoing effort to modernize the program by eliminating legacy requirements, reducing lender friction, and sharpening risk management where it matters most. The agency’s decision to expand flexibility within the Limited 203(k) program and eliminate the outdated HUD-92900-B disclosure reflects a broader push to simplify the borrower experience and remove administrative steps that no longer add meaningful consumer protection. At the same time, FHA tightened aspects of its loss mitigation framework, signaling that the agency remains focused on protecting the Mutual Mortgage Insurance Fund and ensuring that payment assistance is directed toward sustainable outcomes. FHA also pared back certain lender approval and quality control requirements, a move that should lower compliance costs. The updates to appraisal field review requirements further underscore a shift toward more targeted, risk-based oversight rather than one-size-fits-all compliance mandates. Taken together, these actions suggest an FHA that is increasingly comfortable reducing regulatory burden in low risk but high impact policy.

FHA Credit Divergence:

MBA’s first-quarter data reinforces a growing divergence between government and conventional credit performance. Conventional delinquencies remain exceptionally stable at 2.75%, declining from the prior quarter and increasing just 5 basis points from a year ago, while FHA delinquencies climbed to 11.88% - more than four times the conventional rate and 126 basis points above year-ago levels. FHA serious delinquencies increased 212 basis points over the past year, highlighting the greater financial pressures facing many FHA borrowers. At the same time, the data should be viewed in the context of FHA’s recent loss mitigation changes: MBA notes that the expiration of pandemic-era relief options and the implementation of required Trial Payment Plans temporarily keep many borrowers classified as delinquent until permanent workout solutions are completed.

Pulte’s Dual Mandate:

Bill Pulte’s nomination to serve as the Acting Director of National Intelligence, while continuing to lead FHFA through the transition period, has become one of Washington’s more intriguing personnel developments. To simultaneously oversee the GSEs while taking a Cabinet Level national security role, raises questions about how long Pulte will remain engaged in day-to-day FHFA matters. For now, markets appear to be taking a wait-and-see approach, with no immediate policy changes signaled at the GSEs. Stay tuned.

Housing’s Equity Cushion:

U.S. homeowners continue to hold more than $30 trillion in home equity, near record levels despite affordability pressures and higher mortgage rates. Years of home price appreciation and disciplined post-crisis underwriting have created a substantial buffer for household balance sheets and the broader housing market. While slower appreciation and pockets of price correction may limit future equity gains—particularly for recent buyers with smaller down payments—today’s equity position remains one of the housing market’s most important sources of resilience and stability.

THE GATE HOUSE INDEX

The Gate House Index and analysis is designed to provide insight into the status of FHA’s business at a moment in time and over a period of time, as well as other pertinent data points we’re following.

This month, in honor of America’s 250th birthday, we examine several data points that we believe capture or reflect the nation’s remarkable growth and transformation over the past two-and-a half centuries, and the role that the housing and housing finance industries have played.

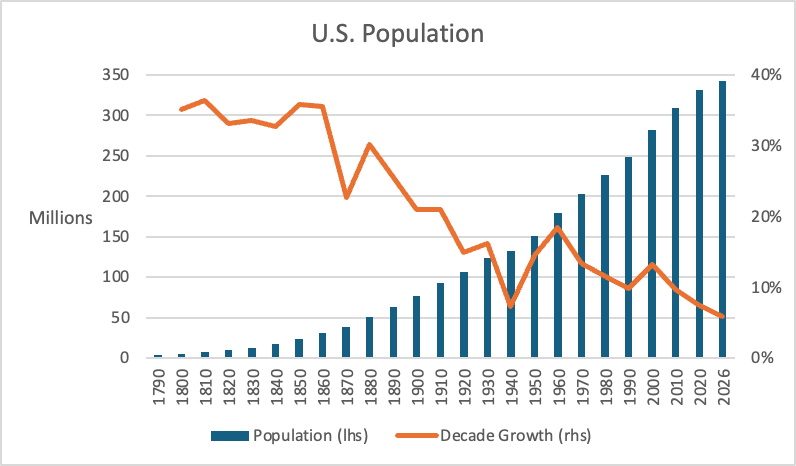

In this first chart, we see the US population growth since the beginning, with a moderating pace in the 21st century:

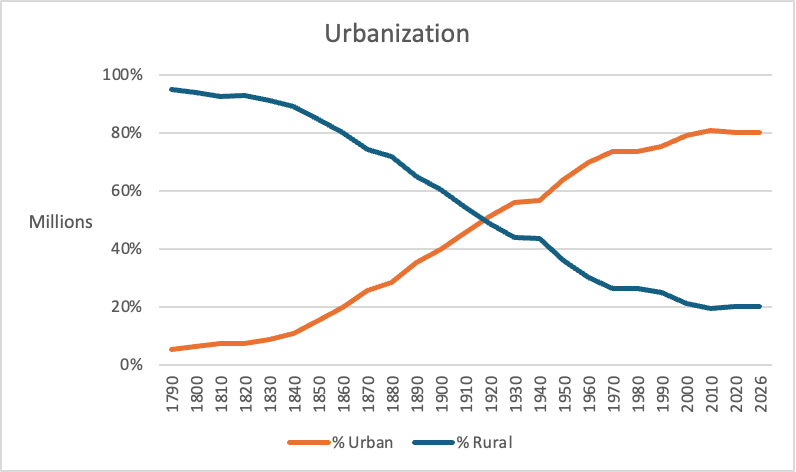

While the U.S. began as a nearly 100% rural society, most of the U.S. population has lived in urban areas since the early 20th century. Urban share has leveled off in recent decades, meaning growth now happens within metros where land use and zoning can be a constraint...

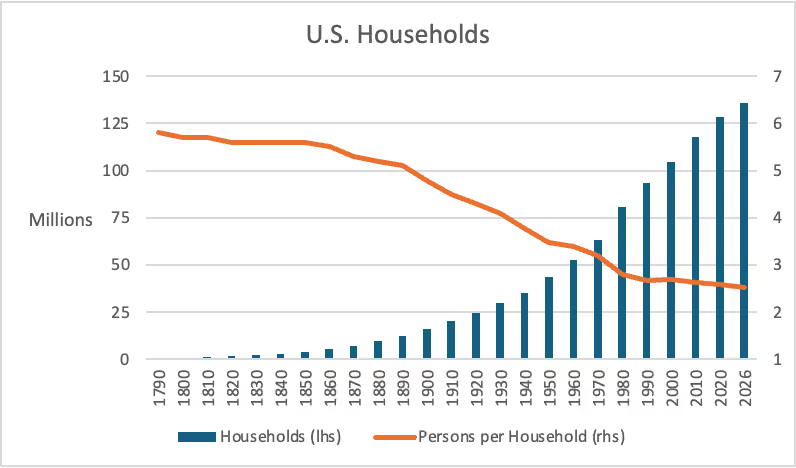

The number of U.S. households has grown faster than the U.S. population overall. Housing demand per capita has nearly doubled since 1900...

Nominal home prices have risen faster than inflation since the middle of the 20th century. After rising modestly for a century, real home prices have broken out of their century-long range, rising and falling dramatically since 2000...

.avif)

.avif)

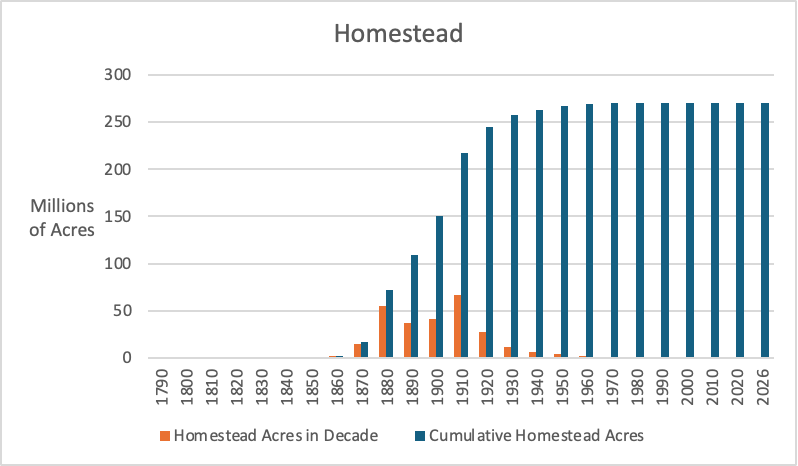

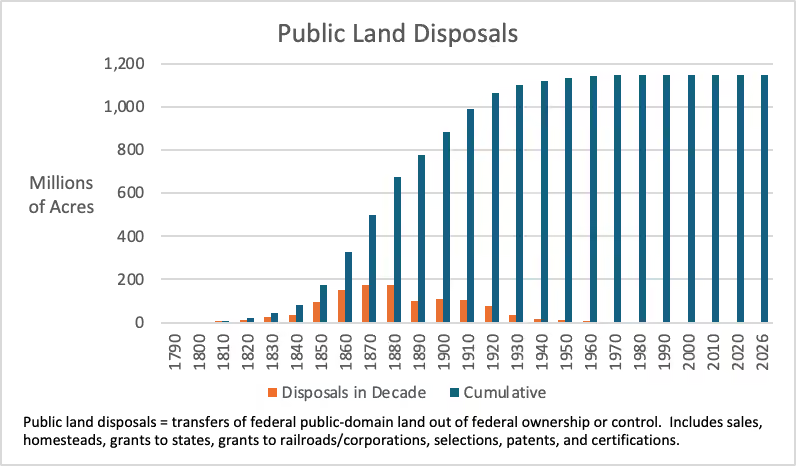

The federal government has transferred nearly 1.3 billion acres of public domain, about 70% of all land it ever acquired, to settlers, states, railroads, veterans, and other entities. Large-scale disposal in the lower 48 ended by the mid-20th century, and FLPMA (1976) formally adopted a policy of federal retention. Nearly all transfers since 1970 reflect Alaska statehood and Native claims conveyances…

The federal government has transferred 270 million acres to about 1.6 million families via the Homestead Acts, land paid for with sweat equity, but <1 million acres since 1970...

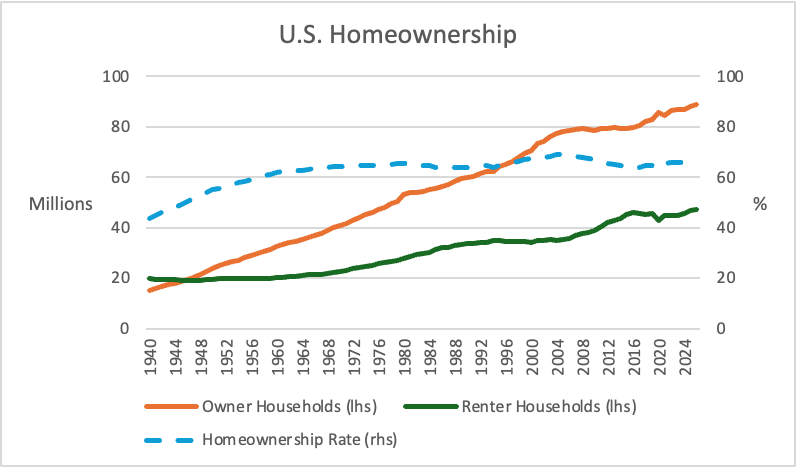

The number of homeowner households has grown faster than renter households since 1940. The homeownership rate increased between 1940 and 1960, with small but meaningful changes within a tight range between 1960 and today...

¹ Acres patented under final homestead entries, per GLO records (~270 million acres, ~1.6 million patents). BLM Public Land Statistics, Table 1-2, reports 287.5 million acres under the broader category "granted or sold to homesteaders," which also includes entries commuted to cash purchase before the residency requirement was completed.

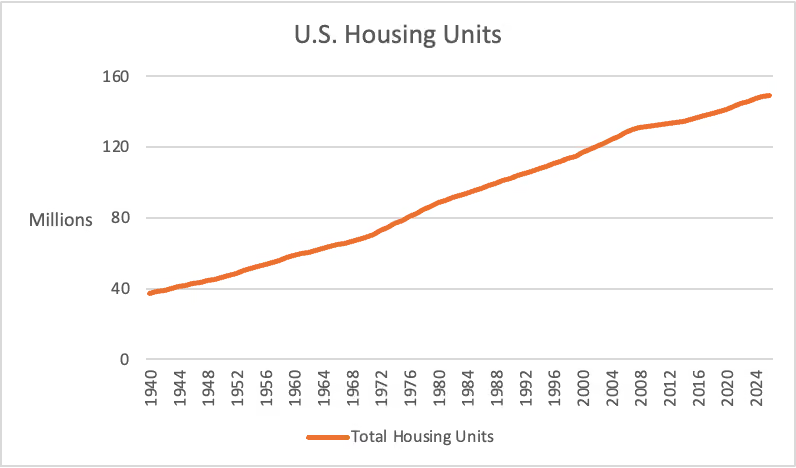

The number of housing units has grown and consistently exceeded the number of U.S. households, partly due to vacancies and some households with 2nd homes and investment properties...

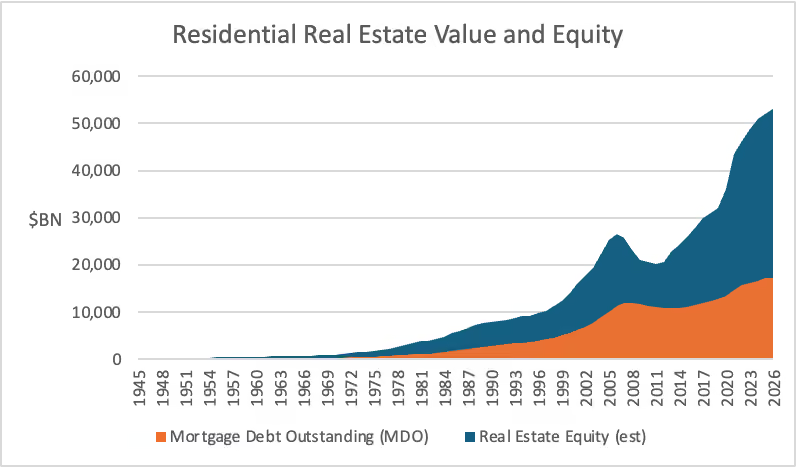

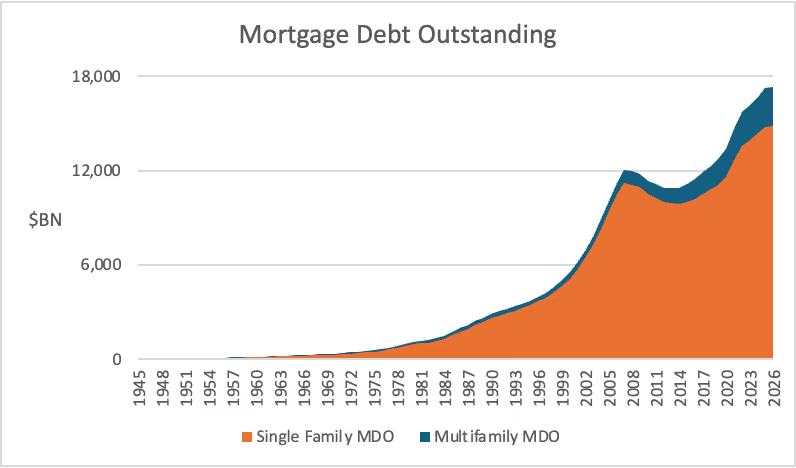

The total value of residential real estate is above $50 TN, and mortgage debt outstanding, held by all sectors, is more than $17 TN. The equity share of home value, about 67%, is the highest since the early 1960s and total equity, roughly $35 TN, is at record levels and up more than 250% since the Great Recession…

Single family mortgage loans represent about 85% of total residential MDO. The multifamily share has grown steadily since 2010, tracking the rental construction boom...

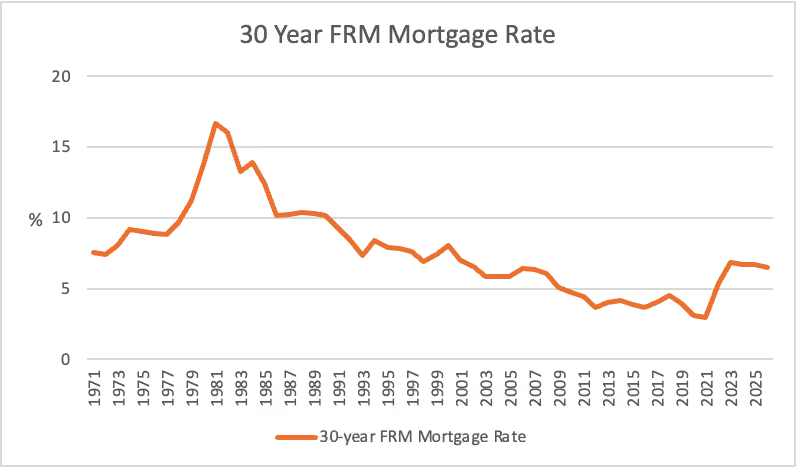

Mortgage interest rates declined steadily between the early 1980s and 2021, with periods of high and low refinance volumes. Rates rose sharply after the pandemic era, but not to the levels of the later decades of the 20th century...

This Month In History

On July 4, 1776, the Continental Congress formally adopted the Declaration of Independence in Philadelphia, severing the 13 American colonies' political ties to Great Britain. Drafted largely by Thomas Jefferson, the document asserted that all people have natural rights to life, liberty, and the pursuit of happiness.

FHA+ is published monthly by Gate House Strategies, a Washington, DC area-based advisory firm focused within the financial services, mortgage lending and servicing, community development, and public housing sectors. Contact us at FHAplus@gatehousedc.com