This Issue Includes:

- Think Piece: In 2023, Congress excluded federally backed housing loans from NEPA—yet HUD and USDA still require it. Paul Compton explains what the law says, why agencies haven’t acted, and what that delay costs the industry.

- Three Questions: FHFA and FHA approved VantageScore 4.0 alongside legacy FICO models—a major shift in mortgage underwriting. Keith Becker breaks down what changed, who benefits, and the operational and risk management challenges ahead.

- Inside Voices: The 21st Century ROAD to Housing Act clears the House 396–13; HUD releases a construction best practices report; manufactured housing gets a potential chassis overhaul; appraisal modernization accelerates; and VA expands benefits and launches a new partial claim program.

- Gate House Index: A look at HUD multifamily NEPA review timelines, the $17 billion in federal housing finance still running through them despite a statutory exemption, and a comparison of VantageScore 4.0 vs. Classic FICO score distributions.

THINK PIECE

NEPA Reform: Congress Ordered the Hostages be Freed in 2023 – Loosening the Shackles on Multifamily Housing

Paul is a founding partner of Compton Jones Dresher, where he advises clients in real estate, financial services, and banking. His practice focuses on affordable and multi-family housing—including tax credit and opportunity zone work—and on the regulatory, M&A, and growth activities of financial institutions. Over 30+ years he's handled hundreds of transactions in Alabama and nationwide, and his prior service as a senior federal official informs his perspective on regulation.

In June 2023, buried inside the debt-ceiling legislation known as the Fiscal Responsibility Act of 2023 (the “FRA”), Congress made the most consequential amendments to the National Environmental Policy Act (“NEPA”) since its enactment in 1970. For the commercial mortgage industry — which has watched projects stall, costs balloon, and timelines stretch to absurdity under decades of regulatory accretion — this should have mattered immediately. Three years later, the implementing regulations at the agencies that matter most to multifamily and affordable housing finance remain largely unreformed. One diagnosis is that the Stockholm Syndrome is in effect: Federal agencies and the industry have been captive to onerous NEPA rules for so long that they apparently cannot envision operating without them, even when Congress has ordered the change.

Background

It is important to begin from the perspective that NEPA provides no substantive environmental protections. It does not prohibit anything. Instead, the Supreme Court stated, “As a purely procedural statute, NEPA does not mandate particular results, but simply prescribes the necessary process for an agency's environmental review of a project.” Seven County Infrastructure Coalition v. Eagle County, 605 U.S. 168 (2025). Thus, NEPA is wholly bureaucratic in nature. It simply requires filings, notices, waiting periods and possibly studies (environmental impact statements; though these almost never happen with housing developments). Complicating things further, sometimes administration of these steps is delegated by federal agencies to state and local government but with oversight, i.e., second-guessing, by the agency. Substantive environmental protections, such as requirements relating to Phase I environmental studies, wetlands delineations, endangered species and archeological resources, are applicable without regard to NEPA. Currently, regulations apply NEPA to almost all multifamily housing with any type of Federal involvement, whether new construction, rehabilitation or even refinancing.

What Congress Did

The FRA did something multifamily housing professionals have long sought. It redefined “major Federal action” — the threshold trigger for NEPA applicability — to require “substantial Federal control and responsibility,” expressly replacing the prior, effectively boundless standard. Most importantly for commercial lenders and their borrowers, the FRA enacted an express statutory exclusion from the definition of “major Federal action” for “loans, loan guarantees, or other forms of financial assistance where a federal agency does not exercise sufficient control and responsibility over the subsequent use of such financial assistance.” Congress placed this exclusion directly in the NEPA statute itself at 42 U.S.C. § 4336e(10)(B). Thus, U.S. Department of Housing and Urban Development (“HUD”) HOME Program Loans, Federal Housing Administration (“FHA”) insured (the functional equivalent of a loan guarantee) new construction or rehabilitation loans under National Housing Act Sections 221(d)(4) and 223(f) respectively, and U.S. Department of Agriculture (“USDA”) loans and loan guaranties are clearly within the ambit of the statutory exclusion.

The significance cannot be overstated. If an action is not a “major Federal action,” NEPA simply does not apply. No threat of an environmental impact statement. No need to obtain a “finding of no significant impact”. No publication of notice. No second guessing of local jurisdictions acting under delegated authority. No choice-limiting activity doctrine tying developers’ hands while environmental review crawls forward. The months-long regulatory environmental process (even the U.S. Supreme Court has recognized that NEPA is purely procedural) goes away. Instead, lenders and borrowers must comply with the substantive environmental laws and use typical commercial diligence approaches to confirm that, as they are typically doing already.

What Agencies Have Done Since — Not Much

The Council on Environmental Quality (“CEQ”) — which was found to lack lawful authority to promulgate NEPA regulations by the Court of Appeals for the District of Columbia Circuit in Marin Audubon Society v. FAA (D.C. Cir. 2024) — did withdraw its implementing regulations in February 2025. That withdrawal, while legally necessary and moderately helpful, simply removes a framework that was already invalid. It does not itself reform the agency-specific regulations that were modeled on the now-invalid CEQ rules.

HUD is the regulatory home for FHA-insured multifamily lending with both formal regulations and provisions of the sub-regulatory “Multifamily Accelerated Processing guide” (the “MAP Guide”). The regulations at 24 C.F.R. Parts 50 and 58 remain essentially unreformed. Those rules — premised on now-withdrawn CEQ regulations and mandates that the federal courts have held CEQ did not have the authority to issue (and CEQ has traditionally resisted HUD efforts from time to time to scale back NEPA applicability) — continue to govern HUD’s environmental review process. The choice-limiting activity doctrine, which can prevent a prospective borrower from purchasing property with its own private funds while federal environmental review proceeds, continues to appear in the regulations and the MAP Guide despite HUD’s cited authority for it being the now-withdrawn CEQ regulations. HUD has issued no rulemaking notice, no interim final rule, and no formal guidance addressing the FRA exclusions. And the mortgage industry seems to have placed the issue low on its priority list.

At USDA’s Rural Development division, the situation is different in form but maybe worse in substance. USDA published final NEPA regulations in April 2026 that acknowledge FRA’s changes in general terms but fail to take the steps the statute commands. Rather than expressly excluding USDA’s direct loans (Section 515) and guarantees for rural rental housing (Section 538), which are, unambiguously, “loans” or “loan guarantees” under the FRA’s financing exclusion — the regulations preserve a case-by-case determination framework that invites continued regulatory creep. They introduce a new concept called a “finding of applicability and no extraordinary circumstance” (FANEC) that appears designed to reconstitute the prior “finding of no significant impact” (“FONSI”) process under a different name — precisely the kind of bureaucratic restraints that the FRA was meant to eliminate.

The Loan Exclusion Means What It Says

A question has circulated in regulatory circles about whether the FRA’s loan exclusion is qualified by the “sufficient control and responsibility” language that follows in the statute. The answer, under straightforward principles of statutory construction, is simply “no.”

The financing exclusion lists three items in series: loans, loan guarantees, and “other forms of financial assistance where a federal agency does not exercise sufficient control and responsibility.” Under the principle of the “last-antecedent canon,” recognized by the Supreme Court most recently in Lockhart v. United States (2016), a limiting clause modifies only the immediately preceding term — not the entire series. In other words, the “sufficient control” qualifier modifies “other forms of financial assistance” and does not reach back to qualify loans or loan guarantees.

This reading is also compelled by the “surplusage canon” a legal principle of interpretation that states courts should give effect to every word and provision in a statute. That is, if the “sufficient control” test applied to loans and loan guarantees, their separate enumeration would be meaningless redundancy — any loan lacking sufficient federal control would already fall outside the general “substantial Federal control” threshold. Reading the exclusion as categorical for loans and loan guarantees gives independent effect to every word Congress chose.

Time for Mortgage Industry Focus and Agencies to Act

The FRA’s loan exclusion, and its redefined threshold for major Federal action, are law. They have been law since June 3, 2023. The delay in adopting regulations to implement the FRA or half measures in implementation is the habit created by decades of multifamily housing being in the NEPA dungeon.

Over the past 10 years there have been about 25,000 FONSI’s under HUD’s regulations and fewer than 10 instances where Environmental Impact Statements were deemed necessary. Thus, even for the deals that are consummated, 99.6% of all HUD completed financings (FHA and HOME) have been delayed for months, exacerbating the shortage and increasing the cost of housing in the United States. Congress did its job in reforming NEPA. It is time for the agencies and industry to do theirs.

For commercial mortgage professionals financing multifamily housing and affordable housing developments with Federal loan programs, the practical stakes are concrete: Deals that die from delay during environmental review, sites that are lost when purchase contracts expire, and projects that never pencil because of NEPA-related carrying costs. The FRA clearly sets housing developments supported by Federally backed loans free from NEPA.

THREE QUESTIONS

with Keith Becker

Keith Becker is a founding partner of Gate House Strategies, with more than 37 years in the mortgage industry, Becker recently served as Chief Risk Officer for the Federal Housing Administration (FHA).

The recent shift toward credit score competition in the mortgage market represents one of the most consequential housing finance policy changes in years. As the Federal Housing Finance Agency (FHFA) and Federal Housing Administration (FHA) move forward with the adoption of VantageScore alongside newer FICO models, policymakers, lenders, investors, and consumer advocates are focused on several important questions.

QUESTION: What did FHFA and FHA announce regarding VantageScore?

Becker: In April, FHFA, in coordination with the U.S. Department of Housing and Urban Development (HUD) and FHA, announced the approval of Vantage Score and FICO 10T (in addition to the existing Classic FICO score) for use within the government-backed mortgage system. The move advances the long-debated implementation of the Credit Score Competition Act and ends the exclusive reliance on legacy FICO scoring models that have dominated mortgage underwriting for decades. Director Pulte also announced that that the GSEs will permit the use of FICO 10T following the release and evaluation of historical credit-score data.

Compared to Classic FICO, VantageScore 4.0 incorporates trended credit data and may also consider certain forms of alternative payment data, including rent, utility, and telecommunications payment histories, to evaluate borrower creditworthiness. Proponents argue that this approach could expand access to mortgage credit for consumers with limited traditional credit histories while improving predictive accuracy.

QUESTION: What are the implications for consumers, lenders and FHA?

Becker: For consumers, the most immediate implication is the potential expansion of mortgage credit access. Applicants with limited credit histories or nontraditional financial profiles that did not have usable FICO scores may become “scorable” and therefore potentially eligible for mortgage financing, consistent with housing goals of expanding access to mortgage credit to underserved borrowers.

The transition creates both strategic opportunities and operational complexity for lenders. Increased competition among credit scoring providers may contribute to lower credit reporting and scoring costs over time, although the magnitude of those savings remains uncertain.

Current VantageScore pricing is very competitive compared to classic FICO and repriced FICO 10T:

And an additional credit score option enables a “lesser of” calculation that could reduce LLPAs. Over time, competition among lenders could result in cost savings for mortgage borrowers.

The ability to evaluate a broader range of borrowers could support market expansion and improved borrower segmentation. At the same time, lenders will need to manage significant implementation challenges, including:

- Updating underwriting and loan origination systems

- Revising credit policy overlays and score cutoffs

- Aligning compliance and fair lending monitoring

- Coordinating secondary market execution and investor requirements

- Training operational and risk management teams on model differences

For FHA and the GSEs, we must first note how third-party credit score models are used. FHA uses both the borrower's overall credit score and the underlying credit tradelines to evaluate risk where the credit score establishes a baseline eligibility filter and serves as a primary risk indicator when combined with debt-to income ratios while the GSEs rely on the analysis of the underlying tradelines and trending of the data over time in lieu of the actual score. In manual underwriting, FHA and the GSEs use third-party credit scores to establish thresholds for product eligibility and compensating factors. Credit scores are also used to set GSE loan level price adjustments (LLPAs). Credit scores and the credit score model will also be included in disclosures to MBS investors.

For the GSE’s, the operational rollout is underway. While there has been commentary suggesting FHA availability could occur “within a couple of months,” the overall scope of change management likely points to a longer time frame than shorter. There are several significant workstreams required before VantageScore 4.0 can be fully operationalized alongside, or in place of, legacy FICO Classic models, including:

- Calibration and validation of VantageScore 4.0 relative to existing FICO-based underwriting frameworks

- Updates to technology platforms, including Catalyst and lender underwriting portals, to process and validate credit reports using VantageScore

- Enhancements to the FHA TOTAL Mortgage Scorecard to recognize and appropriately assess risk across multiple approved score models, including the anticipated future introduction of FICO 10T

- Revisions to the FHA Handbook and related policy guidance to formally permit use of the alternative scoring models

- As part of this process, FHA will likely need to determine whether to allow immediate use across the full range of existing policy parameters (e.g., LTVs, minimum credit scores, DTIs, etc.) or initially apply more conservative overlays while monitoring performance and unintended risk impacts

- Development and communication of delivery and implementation instructions for lenders and vendors

- Consideration of a phased rollout approach with select lenders, similar to the GSE implementation strategy currently being used

Given FHA’s overall credit risk profile and the importance of maintaining consistency across underwriting and servicing operations, it would not be surprising for the agency to take a measured and deliberate approach to implementation.

The transition period may be particularly complex because lenders could be operating with multiple approved scoring models simultaneously.

QUESTION: What are the critical risks that should be considered?

Becker: Several important risk considerations warrant close attention:

- Model risk is central to the transition. Lenders, the GSEs, and FHA will need to determine how VantageScore outcomes compare with existing FICO-based underwriting thresholds and recalibrate eligibility standards, pricing, and risk tolerances accordingly.

- Adverse selection risk has also been widely discussed. Market participants are evaluating whether borrowers, brokers, or lenders could attempt to optimize applications around whichever scoring model produces the most favorable result, both in loan decisions and pricing. How effectively FHFA, FHA, and the GSEs manage these dynamics will be critical to maintaining underwriting consistency and portfolio quality.

- Operational and execution risks are also substantial. Running multiple scoring models in parallel could create inconsistencies across underwriting, servicing, securitization, and quality control processes, particularly during the implementation phase.

- Fair lending and consumer impact considerations will receive significant scrutiny as well. Changes in scoring methodologies and data inputs could affect approval rates, pricing outcomes, and borrower segmentation across demographic groups. Regulators and lenders will likely need enhanced monitoring to ensure compliance with fair lending standards and to assess disparate impact concerns.

- Secondary market acceptance and performance validation remain important unresolved considerations. Investors will closely monitor how loans underwritten using different scoring models perform over time, including potential implications for mortgage-backed securities pricing, representations and warranties, servicing outcomes, and overall credit performance consistency. Ultimately, the pace and success of implementation will likely depend on how quickly market participants gain confidence in the comparability, transparency, and predictive reliability of the new scoring framework.

The transition to credit score competition has the potential to expand access to mortgage credit, modernize underwriting, and introduce meaningful innovation into the housing finance system. At the same time, the success of implementation will depend on careful management of the risks to ensure the new framework strengthens both market access and long-term housing finance stability.

INSIDE VOICES

Landmark Housing Legislation:

On May 20, the bipartisan 21st Century ROAD to Housing Act cleared the House by an overwhelming 396–13 vote, advancing one of the most significant federal housing packages in decades and setting up final negotiations with the Senate. The legislation combines a broad range of supply-focused reforms, including manufactured housing expansion, permitting and regulatory streamlining, community development initiatives, and restrictions on large institutional investors' purchases of single-family homes. Notably, the House removed the Senate’s controversial seven-year build-to-rent divestiture requirement, reflecting concerns that the provision could discourage new housing production. With strong bipartisan support in both chambers, housing stakeholders are increasingly optimistic that congressional leaders—including Senate Banking Committee leaders Tim Scott and Elizabeth Warren—can reach a final compromise later this summer.

HUD Best Practices:

HUD Secretary Scott Turner recently released HUD’s Best Practices for Home Construction report aimed at reducing regulatory barriers, accelerating permitting and construction timelines, and lowering housing development costs. The guidance encourages state and local governments to streamline approvals, unlock additional land for development, and reduce regulatory burdens that contribute to higher home prices and limited housing supply. The report reflects the Administration’s agenda to increase housing production and reduce housing development barriers. Expect HUD to continue to play a proactive role in these issues.

A Transformative Manufactured Housing Reform:

The 21st Century ROAD to Housing Act includes several provisions designed to expand manufactured housing as a lower-cost homeownership option, including a proposal to relax HUD’s longstanding “permanent chassis” requirement by allowing certain manufactured homes to be built without a permanent chassis. Supporters argue this change could reduce costs, improve design flexibility, and expand placement opportunities while helping modern factory-built housing compete more directly with site-built homes. From a policy perspective, the chassis provision may be one of the bill’s most consequential supply-side reforms. If coupled with progress on zoning, appraisal, and financing challenges, the change could help position factory-built housing as a more scalable solution to the nation’s affordability and housing supply challenges.

Appraisal Modernization Accelerates:

Loan Program Reform Act in 2025, House Republicans recently introduced the VA Home Loan Appraisal modernization is gaining momentum following the Administration’s recent housing affordability Executive Orders, with policymakers increasingly focused on removing unnecessary costs and delays from the mortgage process. At MBA’s Secondary and Capital Markets Conference, industry participants called for greater alignment among FHA, VA, and GSE appraisal policies, including broader use of desktop appraisals, data standardization, hybrid valuation approaches, and other modernization tools already being deployed by the GSEs. FHA officials also highlighted the growing role of automated valuation models (AVMs) as a means to improve efficiency, lower borrower costs, and expand access to credit while maintaining appropriate risk controls. More recently, on May 29 FHA issued a Request for Information (RFI) seeking feedback on ways to streamline its Minimum Property Requirements (MPRs). Together, these developments signal likely changes ahead.

VA Actions:

Following enactment of the VA Home Affordability Act (H.R. 8532) to further modernize the VA housing benefit by reducing regulatory barriers, accelerating closing timelines, lowering closing costs, streamlining digital processing, and aligning select VA practices more closely with other federal housing programs. The bill now awaits committee markup and potential floor consideration in the House, with Senate introduction expected to follow if bipartisan agreement holds. The House passed the Sharri Briley and Eric Edmundson Veterans Benefits Expansion Act, which expands eligibility to more National Guard and Reservists, increases some funding fees, and extends the funding fee schedule through September 2036. Finally, the VA Partial Claim program final rules were published June 1, codifying the new loss mitigation option - the program goes live June 15, but servicers have 180 days to fully implement.

Reconsideration of Value:

The 21st Century ROAD to Housing Act proposes reforms to the Reconsideration of Value (ROV) process. The policy would establish consistent requirements for lenders that respond to consumer requests of a reconsideration of value, or a second appraisal. The changes also aim to align UDSA, FHA, VA, and FHFA (GSE) practices more closely to ensure a more uniform and predictable valuation appeals process nationwide. While any changes may have compliance implications, consistent policy across the regulatory landscape should bring efficiencies.

THE GATE HOUSE INDEX

The Gate House Index and analysis is designed to provide insight into the status of FHA’s business at a moment in time and over a period of time, as well as other pertinent data points we’re following.

This month, we look at the a few data points related to the discussions above, including Paul Compton addressing how FRA changed the definition of "major federal action" that determines when NEPA applies to HUD-related loans and loan guarantees, and Keith Becker’s thoughts on the adoption of Vantage Score usage.

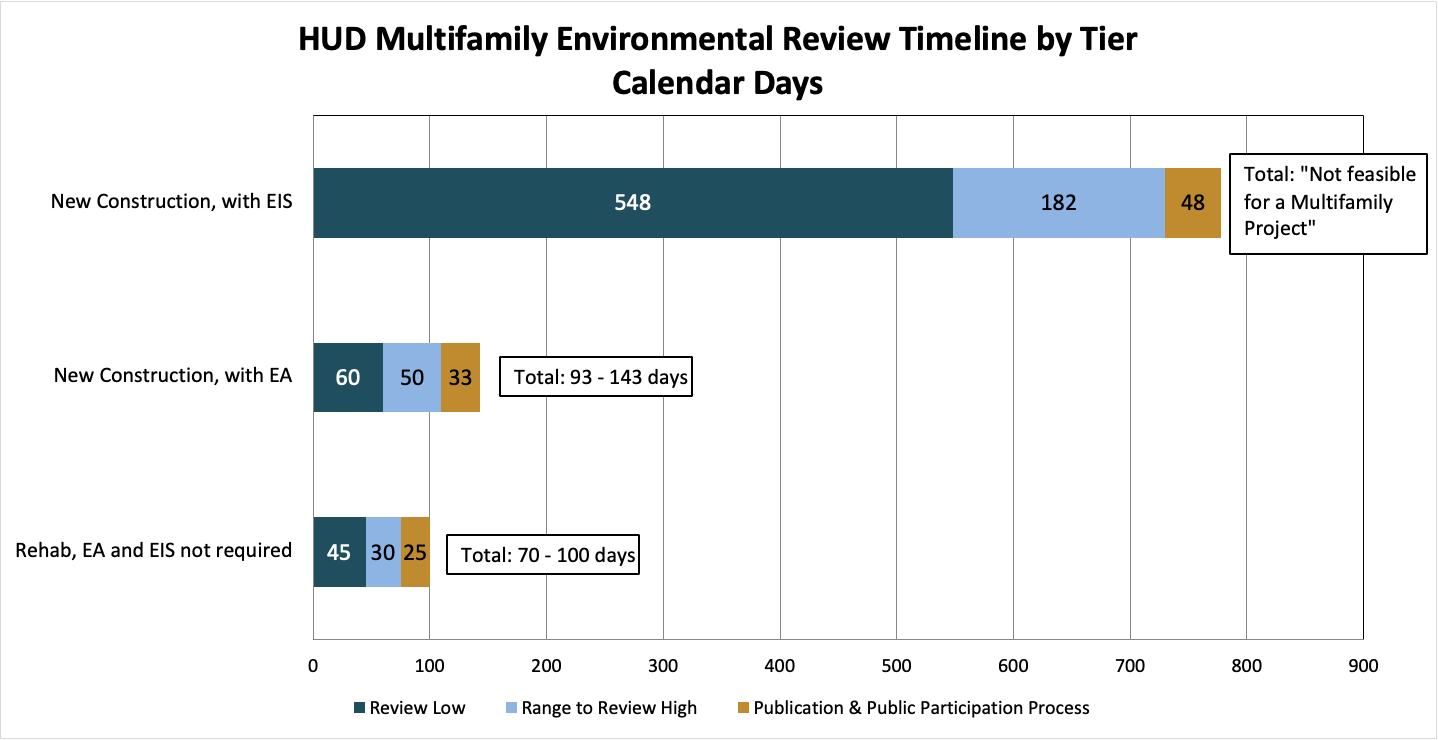

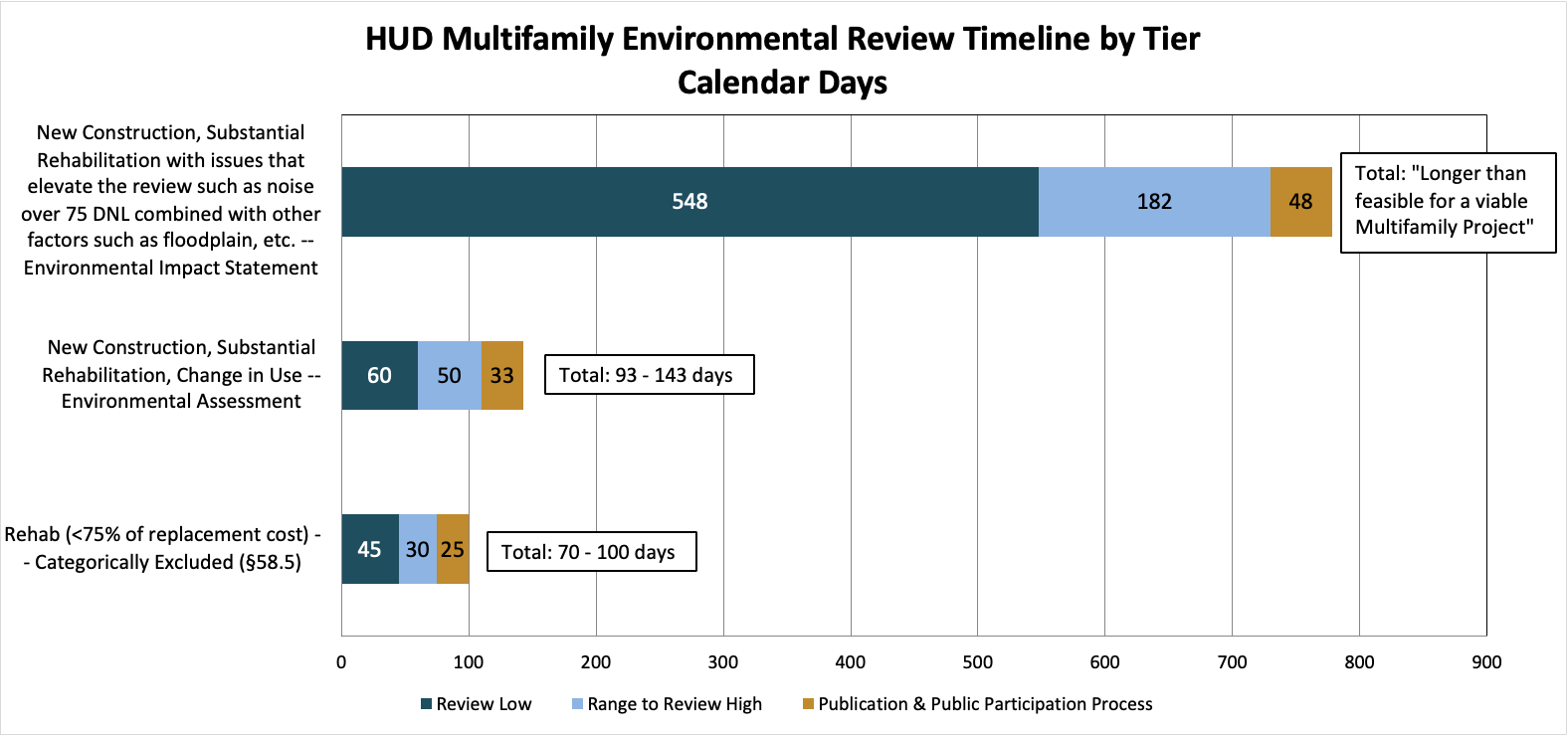

Based on the review timeframes published by the Texas Department of Housing and Community Affairs (TDHCA), every tier of HUD multifamily environmental review lasts months and projects that would require an Environmental Impact Statement take longer than is feasible for a viable multifamily project.

The chart above shows the timeline for completion of different levels of environmental review for HUD multifamily projects:

- The short timeline is for projects that don't require an EA (environmental assessment) or EIS (Environmental Impact Statement), but are still subject to review under other federal environmental laws.

- The medium timeline applies to projects that require an EA — e.g., new construction, substantial rehabilitation, or changes in use.

- The long timeline is for projects requiring an EIS — projects with 2,500 or more housing units and when an EA shows significant environmental impacts.

In other words, all HUD multifamily projects could move to the short timeline and many projects that HUD doesn't do today could become viable.

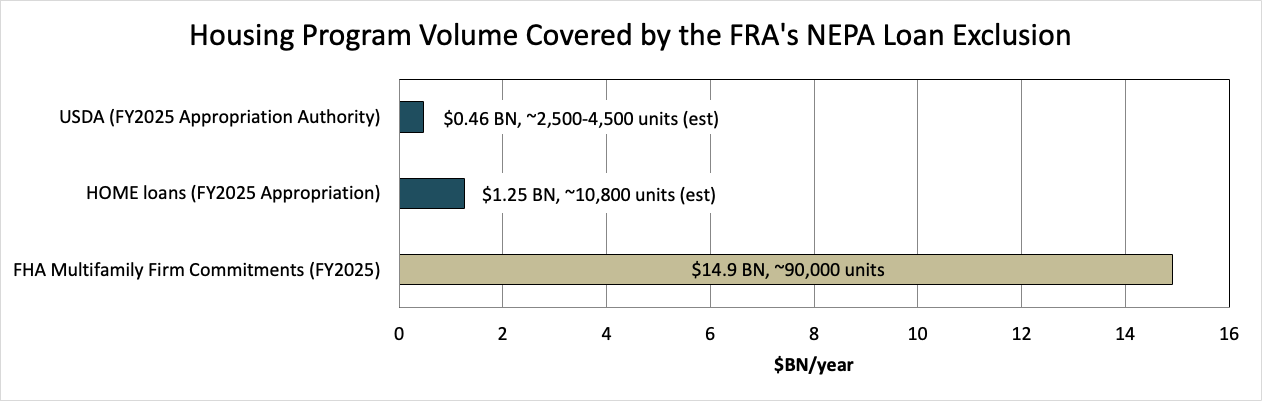

Moreover, in FY 2025, the FRA's loan exclusion covered roughly $17 BN of federal housing finance and over 100,000 housing units. The agencies have not yet implemented the statutory carve-out, so these deals still ran through NEPA.

HOME (FY2025, $1.25B appropriation), https://www.congress.gov/crs-product/R40118;

FY2023 units in HOME National Production Reports scaled to FY2025, https://www.federalregister.gov/documents/2025/01/06/2024-29824/home-investment-partnerships-program-program-updates-and-streamlining

USDA (FY2025 authority, Sec. 515 $60M + Sec. 538 $400M) FY2026 Budget Summary, Table RD-2 - https://www.usda.gov/sites/default/files/documents/2026-usda-budget-summary.pdf; unit count estimated

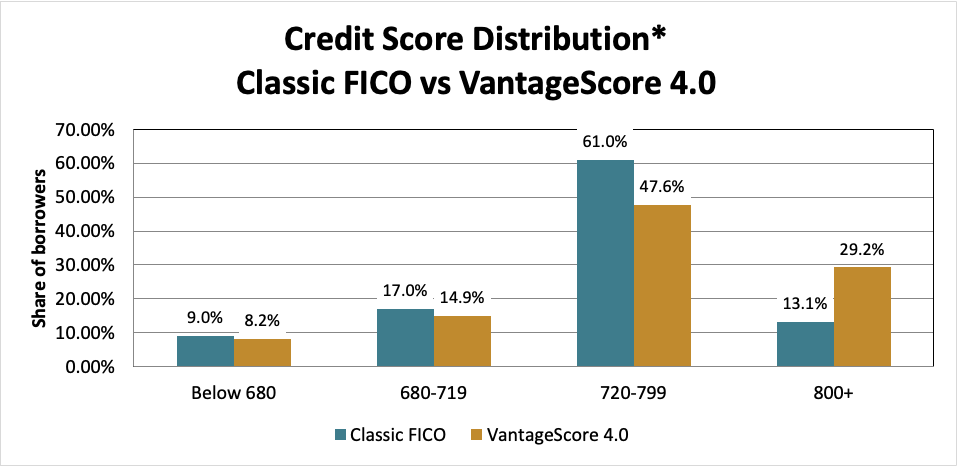

For a decade of Fannie Mae loan acquisitions analyzed by the Urban Institute in late 2024, the share of borrowers with VantageScore 4.0 ≥ 800 exceeded the share with Classic FICO ≥ 800. The share difference in the 800+ range was mostly offset by more borrowers with Classic FICO than VantageScore 4.0 scores in the 720-799 range.

Source: Urban Institute, https://www.urban.org/sites/default/files/2024-12/Classic_FICO_versus_VantageScore_4.0.pdf

Classic FICO has been the exclusive credit scoring model used by FHA and the GSEs for many years. The recently approved VantageScore 4.0 and FICO 10T scoring models include features that could expand the number of scorable consumers and could improve predictive performance relative to Classic FICO.

This Month In History

On June 27, 1934, President Franklin D. Roosevelt signed the National Housing Act of 1934 into law, creating the Federal Housing Administration (FHA) and its mutual mortgage insurance program. By introducing federal mortgage insurance, the Act enabled lenders to offer long-term, fully amortizing loans, ushering in the modern American mortgage. FHA began by insuring 20-year, fully amortizing loans with a maximum LTV ratio of 80%.

FHA+ is published monthly by Gate House Strategies, a Washington, DC area-based advisory firm focused within the financial services, mortgage lending and servicing, community development, and public housing sectors. Contact us at FHAplus@gatehousedc.com